Why Wont Regions Let Me Overdraft

Okay, so picture this: you're at that ridiculously trendy café that only serves coffee in repurposed jam jars, and you're about to impress your date with your sophisticated taste in artisanal pastries. You reach for your wallet, feeling like a high-roller, ready to drop some serious coin on almond croissants. Then… disaster strikes. Your card gets declined. Declines HARD. You stare blankly at the barista, beads of sweat forming on your forehead. "Insufficient funds," they chirp, with the breezy indifference of someone who clearly doesn't know the existential dread you're experiencing. You think, "But... but I thought I had, like, five dollars in there!"

That, my friends, is the moment you realize you're about to face the wrath of… wait for it… your bank's overdraft policies. And you start to wonder, why on Earth won't they just let you borrow that tiny bit of cash? It's not like you're asking for a bailout to buy a small island (though, wouldn't that be nice?).

The Mythical Land of Overdraft Protection (or Lack Thereof)

Let's be real. We've all been there. The temptation to spend just a little bit more than we have is strong, especially when faced with those aforementioned almond croissants. Banks used to be much more lenient with overdrafts. They'd happily let you slide into the red, then slap you with a fee that could fund a small nation's infrastructure projects. I swear, back in the day, you could overdraft a penny and end up owing more than the GDP of Liechtenstein.

Must Read

But things are different now. Regulations have tightened, and banks are, dare I say it, slightly less predatory. (Don't get me wrong, they're still profit-driven machines, but hey, baby steps!). So, why the change of heart? Well, it boils down to a few key reasons:

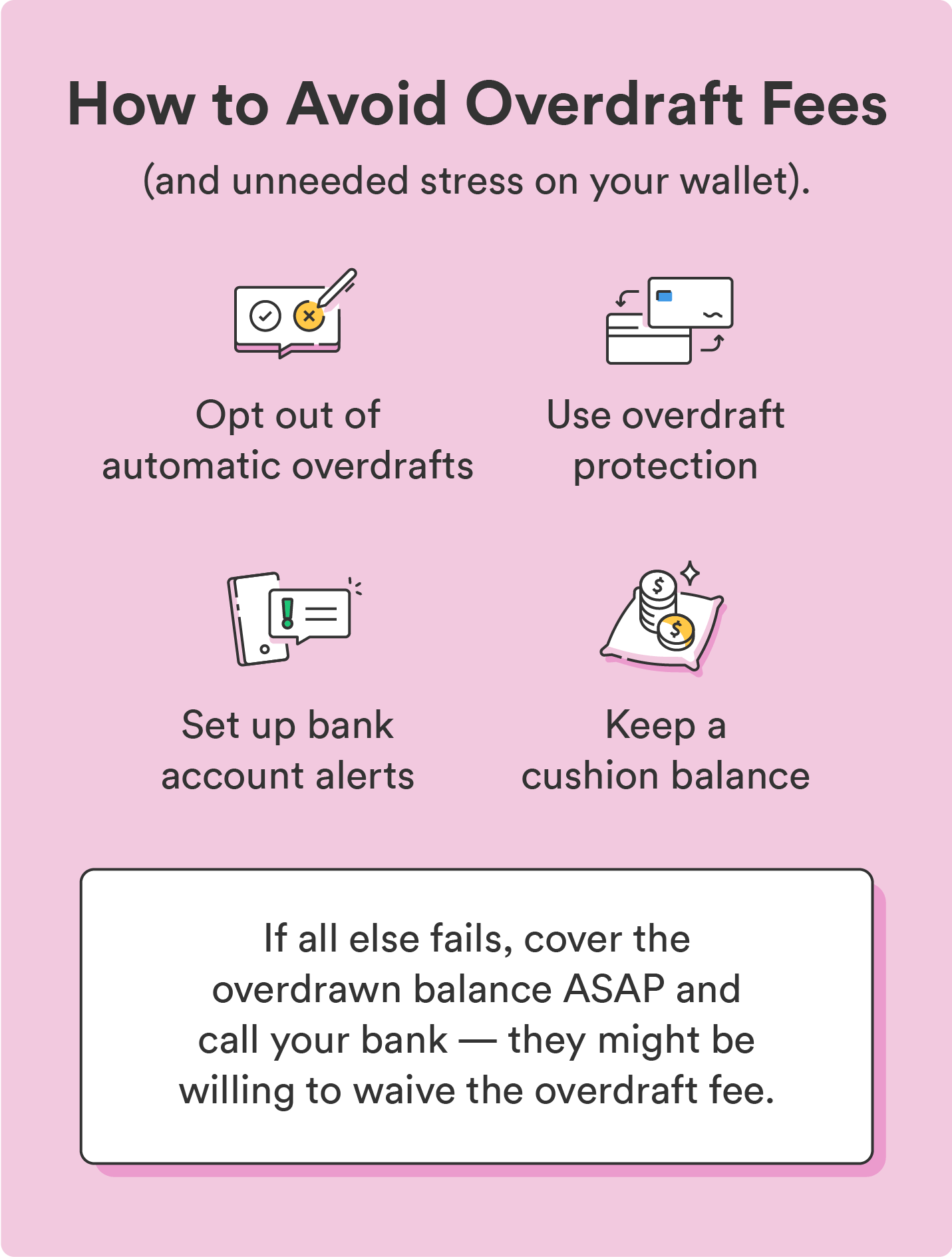

1. Regulations, Regulations, Regulations: The government, in its infinite wisdom (sometimes debatable, I know), stepped in and said, "Enough is enough!" They put in place rules that require banks to get your explicit permission before enrolling you in overdraft coverage for ATM withdrawals and one-time debit card transactions. That's why you probably had to sign something at some point saying you wanted overdraft "protection." And if you didn't sign, or you actively declined, then congratulations! You're overdraft-free (at least, in terms of them letting you go into the negative and charging you for it).

2. The Risk Factor (aka, They Don't Trust You… Yet): Banks are in the business of lending money, but they only want to lend it to people they think will pay it back. Overdrafting is essentially a tiny, instant loan. If you're a new customer, or you have a history of… let's just say "creative" financial management (like repeatedly bouncing checks or having collections agencies call you on a first-name basis), they might be hesitant to extend that credit. They're thinking, "If they can't manage their current balance, what makes us think they'll pay back the overdraft fee, let alone the actual amount they spent?"

3. The Alternatives: Banks aren't completely heartless (debatable, I know, I know!). They often offer alternatives to standard overdraft coverage, like linking your checking account to a savings account or a credit card. If you overdraft, they'll automatically transfer funds from the linked account to cover the shortage. This can be a cheaper way to avoid the embarrassment (and the fees!). Though, heads up, credit cards are expensive!

So, What Can You Do? (Besides Eating Ramen for the Rest of the Month)

Okay, so you're stuck at the café, contemplating a life of instant noodles. Don't despair! Here are a few tips to avoid this scenario in the future:

Keep a Close Eye on Your Balance: I know, it sounds painfully obvious, but seriously. Download your bank's app, sign up for text alerts, or even keep a handwritten ledger (if you're feeling particularly retro). Knowledge is power, and knowing how much money you actually have is the first step to financial freedom (or at least avoiding overdraft fees).

Consider Overdraft Protection: If you're prone to accidental overdrafts (we all slip up sometimes), it might be worth considering overdraft protection. Just be sure to read the fine print and understand the fees associated with it. Compare it to the cost of not having it and paying those hefty, one-time overdraft fees.

:max_bytes(150000):strip_icc()/overdraft-4191679-899410ea0c854304b930597f7126d1e0.jpg)

Link Your Accounts: As mentioned earlier, linking your checking account to a savings account can provide a safety net. Just make sure you actually have money in your savings account. Otherwise, you're just transferring the problem to a different pot.

Budget Like a Boss: This is the holy grail of financial management. Create a budget, stick to it (as much as possible), and track your spending. There are tons of budgeting apps and tools available, so find one that works for you. Think of it like a video game, but instead of leveling up your character, you're leveling up your bank account.

The Bottom Line: Overdrafting is a pain, but it's not the end of the world. By understanding why banks are hesitant to let you go into the red and taking proactive steps to manage your finances, you can avoid the embarrassment (and the fees!) of insufficient funds. And maybe, just maybe, you'll finally be able to afford those artisanal pastries without breaking the bank.