Why Are Refinance Rates Lower Than Purchase Rates

Hey friend! Ever noticed something kinda…off? Like, when you buy a house, the interest rate is higher than when you refinance it later? What's the deal?! Is the universe playing a trick on us?

Don’t worry, you're not losing it. It's a real thing. And honestly? It’s a bit of a financial head-scratcher. But that's why we're here, right? To untangle the weirdness.

Risk Assessment: The Adult Version of "Trust Me, Bro"

Okay, so banks aren't just giving away money for funsies. They're all about risk. Think of it like this: lending money is like letting your friend borrow your prized vinyl collection. Are you more nervous letting a responsible, settled friend borrow it or a new acquaintance you just met at a punk rock show?

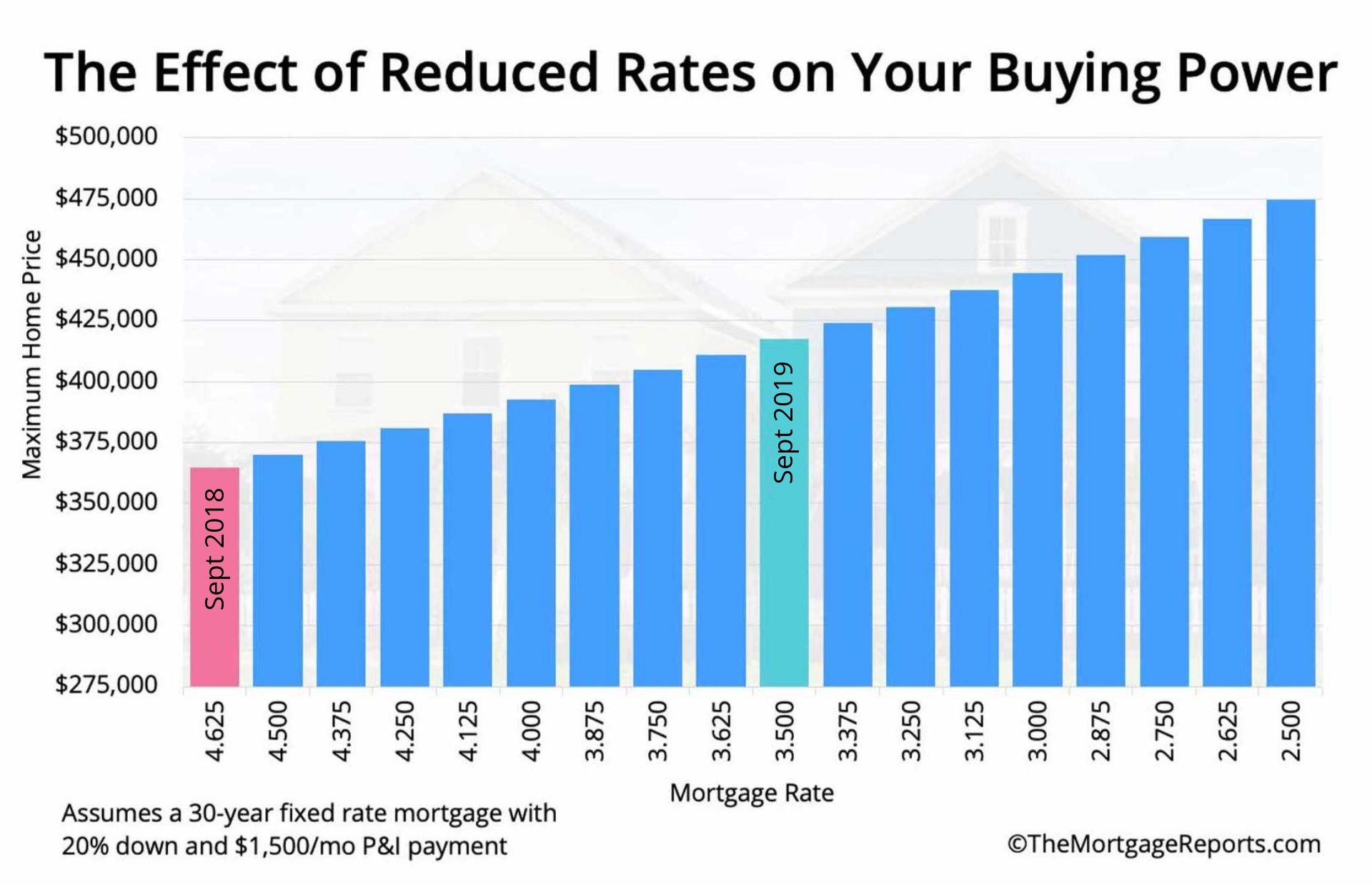

Must Read

Buying a house is like that first, hesitant loan. Banks don't really know you yet. They see your credit score, your income, your sparkly personality (maybe), but it's still a gamble. Higher risk = higher interest rates.

Refinancing? That’s like your friend returning your vinyl collection, and cleaning your apartment as a thank you! They've proven they’re responsible! You've already been paying them for years (your mortgage). The bank sees you're a good bet. Lower risk = potentially lower interest rates!

Quirky fact: Banks are like REALLY into assessing risk. They have teams of analysts crunching numbers and building algorithms. It’s intense!

The Economy, Stupid! (And Other Boring Stuff)

Sorry, had to quote that movie. But seriously, the overall economy plays a HUGE role. Interest rates fluctuate based on what's happening in the world. Inflation? Recession fears? The Federal Reserve doing mysterious things? All impact rates.

Think of it like the weather. Sometimes it's sunny mortgage rates, sometimes it's a blizzard of high rates. It's all connected!

So, maybe when you bought your house, the economic climate was…rough. Rates were high. But a few years later, things mellow out. The economy chills, and rates drop. Refinancing becomes a way to snag those lower rates.

Funny Detail: Economists have like, a million different indicators they watch. It’s basically their own secret language. Good luck trying to decipher it all!

Loan Types: Not All Mortgages Are Created Equal

Did you get an FHA loan? A VA loan? A conventional loan? Each type comes with its own set of rules and risks. For instance, FHA loans often come with Mortgage Insurance Premiums (MIP), which adds to the overall cost.

Maybe when you bought, an FHA loan was the best option. But when you refinance, you might qualify for a conventional loan, ditching the MIP and lowering your overall rate.

It’s like upgrading from coach to first class. Smoother ride, better snacks, and (hopefully) a lower overall financial burden (through lower rates!).

Important Note: Always, always shop around and compare loan types when buying and refinancing. Don't just take the first offer you get!

The Magic of Improved Credit (and Other Financial Awesomeness)

Maybe since you bought your house, you've become a financial rockstar. You've paid down debt, boosted your credit score, and now you look like a dream borrower.

A higher credit score means lower risk to the bank. And lower risk often translates to lower interest rates! It's like leveling up in a video game, but instead of a cool sword, you get a better mortgage rate.

Pro Tip: Check your credit report regularly! Make sure everything is accurate. Even small errors can ding your score.

Closing Costs: The Not-So-Fun Part

Okay, let's be real. Refinancing isn't completely free. There are closing costs. Appraisal fees, title fees, application fees... it adds up. It's kinda like paying for the privilege of getting a lower interest rate.

You need to do the math to make sure refinancing actually makes sense. Will the savings from the lower interest rate outweigh the closing costs? It’s like deciding if that fancy new gadget is really worth the splurge.

Word to the Wise: Negotiate those closing costs! You might be surprised at what you can get reduced or waived.

So, there you have it! A (hopefully) not-too-boring explanation of why refinance rates can be lower than purchase rates. It's a mix of risk, economics, loan types, and your own financial awesomeness.

Go forth and conquer the world of mortgages! Or, at least, understand it a little better. You got this!