Which Statement Regarding Universal Life Insurance Is Correct

Okay, let's talk Universal Life Insurance. Sounds thrilling, right? Maybe not as exciting as binge-watching the latest K-drama, but understanding the basics can save you a world of stress (and maybe even some real money) down the road. The insurance world can feel like navigating a particularly dense fog, so let’s clear up one specific question: which statement regarding universal life insurance is actually correct?

Before we dive in, let’s acknowledge something: insurance isn't a one-size-fits-all deal. It's like finding the perfect pair of jeans – what works for your best friend might not be right for you. But fear not! We’re here to demystify things.

Universal Life Insurance: The Basics

Think of Universal Life (UL) insurance as a flexible, customizable version of traditional life insurance. It's like that super-organized friend who always has a plan but is also cool with changing it up last minute. Here are a few key characteristics:

Must Read

- Flexible Premiums: Unlike term life, you often have some leeway in how much you pay and when (within certain limits, of course).

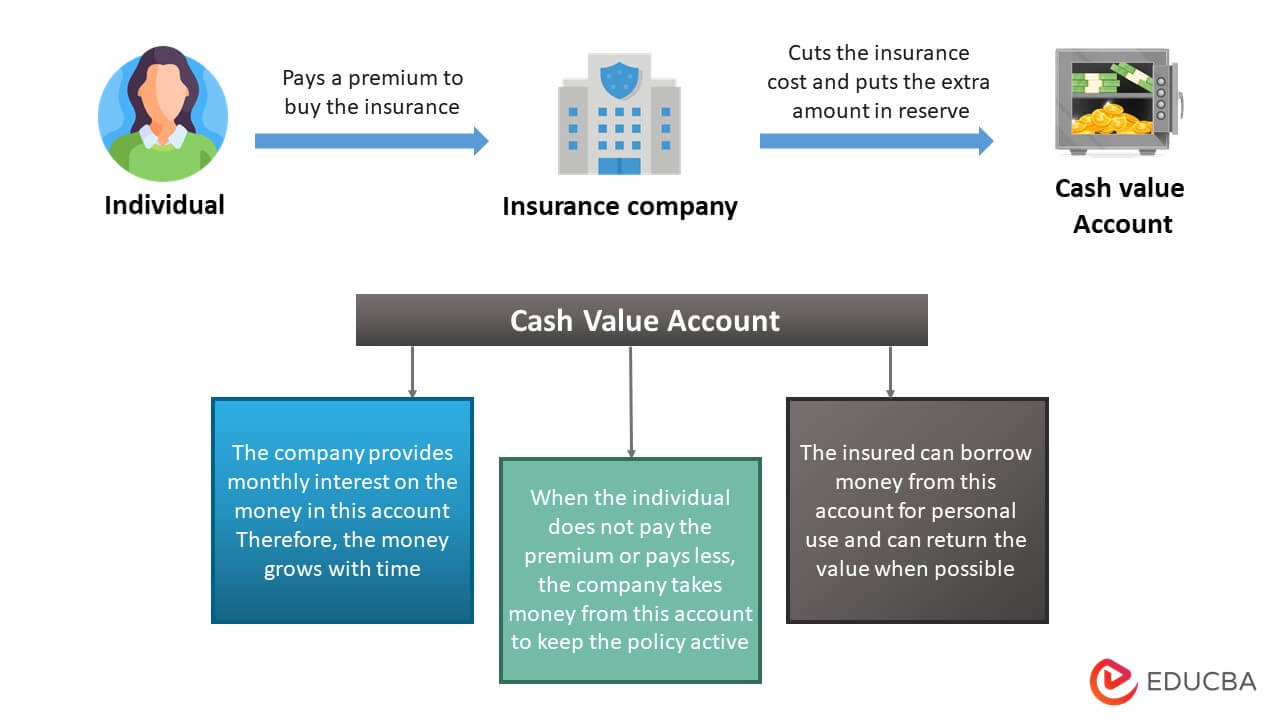

- Cash Value: A portion of your premium goes toward building a cash value that grows over time, tax-deferred. Think of it as a savings account tucked inside your insurance policy.

- Adjustable Death Benefit: In some cases, you can adjust the death benefit, although this can impact the cash value and premiums.

Now, let’s get to the heart of the matter. You'll often see statements like these about Universal Life insurance:

* "Universal Life policies have fixed premiums throughout the life of the policy." * "The cash value grows at a guaranteed rate." * "The death benefit is never adjustable." * "Universal Life policies offer premium and death benefit flexibility."The correct statement is: Universal Life policies offer premium and death benefit flexibility.

Let's break down why the others are wrong:

* Fixed Premiums? Nope. One of the biggest selling points of UL is its flexibility. You can adjust your premiums, although it’s crucial to understand the impact on your policy. Consistent lower premiums could eat into the cash value, and even cause the policy to lapse. * Guaranteed Growth? Not Always. While some UL policies may offer a minimum guaranteed interest rate, the actual rate can fluctuate based on market conditions. It's more like an index fund than a high-yield savings account, so understanding the nuances of the specific policy is critical. * Never Adjustable Death Benefit? Think Again. You can typically adjust the death benefit. However, be aware that increasing it will likely increase your premiums. Decreasing it could impact the cash value. Consult your financial advisor before making any big changes!Practical Tips and Considerations

So, you're considering a Universal Life policy? Awesome! Here are a few things to keep in mind:

Fun Fact: Did you know the first life insurance policy in America was issued way back in 1762? Back then, policies were a lot less flexible!

In short, flexibility is key with Universal Life. Think of it like choosing between streaming services. With Netflix, you're locked into a monthly fee. With something like Hulu, you can add or subtract channels to customize your subscription. UL is more like the Hulu option, which requires you to monitor and adjust your plan for maximum value.

Life and Lessons: A Little Reflection

Life, like Universal Life Insurance, is all about balance and adjustments. We set goals, make plans, and then, inevitably, life throws us a curveball. The key is to be adaptable, informed, and willing to reassess as needed. Just as you wouldn't blindly invest your savings, don't blindly choose an insurance policy. Do your research, seek expert advice, and make informed decisions that align with your unique circumstances. And remember, like that favorite playlist, your financial strategy is a work in progress, constantly evolving to create the perfect soundtrack for your life.