Which Of The Following Is True Of Level Term Insurance

Okay, picture this: you’re at a family barbeque. Aunt Mildred is grilling burgers (slightly charred, as always), Uncle Jerry is telling the same fishing story for the tenth time, and you're cornered by your cousin, Brenda, who’s suddenly become a life insurance guru. Brenda's launching into a detailed explanation of… well, something insurance-y. Your eyes start to glaze over.

But hold on! Before you fake a sudden phone call, let's talk about one type of life insurance that’s actually pretty straightforward: Level Term Insurance. And let's answer the question: Which of the following is true of level term insurance? Skip the insurance jargon and dive into some real-world, relatable stuff.

The "Level" Part: It's All About Consistency

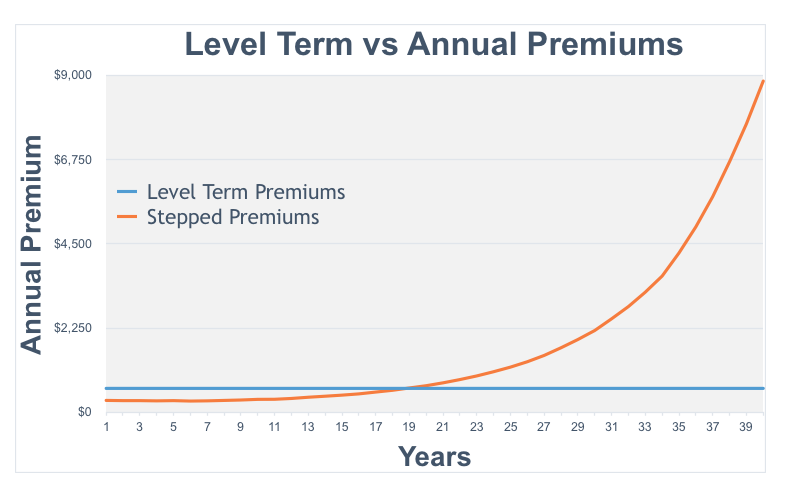

The key word here is "level." This applies to the premium you pay (that's the amount you pay regularly, like your Netflix subscription, but hopefully more useful) and the death benefit (that's the amount your loved ones get if, you know, you kick the bucket). Both stay the same throughout the term of the policy.

Must Read

Think of it like this: you're renting an apartment. You agree to pay $1,500 a month for two years. Boom! Predictability. That’s kind of how level term insurance works. You pay the same premium for a set period – say, 10, 20, or even 30 years – and the amount your beneficiaries (the people who get the money) receive stays the same throughout that entire period.

Why is this a Big Deal? Because Life is Unpredictable (Except When It Isn't)

Life throws curveballs, we all know that. Unexpected car repairs, surprise birthday parties your kids guilt you into hosting, Brenda’s insurance pitches at family gatherings... But with level term, at least your insurance cost and payout are predictable. You can budget accordingly, and your family can count on a specific amount of support if something happens to you during the term. This is particularly helpful if you have young children or a mortgage that needs to be paid off.

Consider this scenario: Sarah and John just bought their first house. They have a mountain of debt from student loans, but they are happy. They take out a 30-year level term insurance policy to cover the mortgage in case something happens to John. This way, Sarah and their future children can stay in their home, safe in the knowledge that their financial worries are taken care of. No more moving in with Aunt Mildred because the mortgage is underwater!

Don't Confuse It with Your Grandma's Antique Vase (It's Not An Investment)

Here's a crucial point that often gets lost in translation: level term insurance is NOT an investment. You're not going to get rich off it. It's pure insurance, designed to protect your family financially during a specific period. There's no cash value that builds up over time.

Think of it like paying for car insurance. You're hoping you never need it, but it's there to provide financial protection if you get into an accident. If you don't get into an accident, you don't get your premiums back. Same deal with term life insurance. If you outlive the term, the policy simply ends, and you've paid for the peace of mind of knowing your family was protected.

What Happens When the Term Ends? The Great Insurance Cliff!

So, what happens when the term is up? Well, like a TV show that gets cancelled after a few seasons, the policy ends. You no longer have coverage. You generally have a few options:

- Renew the policy: This usually comes at a much higher premium, especially as you get older. Remember how your car insurance went up after your, ahem, "spirited" driving incident? Similar idea.

- Convert to a permanent policy: Some term policies allow you to convert to a permanent life insurance policy, such as whole life. This can be a good option if you still need coverage but be aware that permanent policies typically have higher premiums.

- Let it expire: If you no longer need the coverage (maybe the kids are grown, the mortgage is paid off, and you're living off the interest of your vast fortune), you can simply let the policy expire.

Ultimately, deciding if level term insurance is right for you depends on your individual circumstances and financial goals. However, understanding the basics can help you navigate the sometimes-confusing world of insurance and make informed decisions for you and your loved ones.

So, next time Brenda corners you at the barbeque, you can confidently explain that the beauty of level term insurance is its predictability and simplicity. Or you can just fake that phone call. Your call!