Which Of The Following Are Product Costs For A Manufacturer

Hey there, friend! Ever wondered what sneaky costs go into making that awesome gizmo you just bought? We're diving into the fascinating world of product costs for manufacturers. Don't worry, it's not as scary as it sounds (unless you're the one paying the bills, haha!). Think of it as uncovering the secret recipe for a manufactured product.

So, What Exactly Are Product Costs?

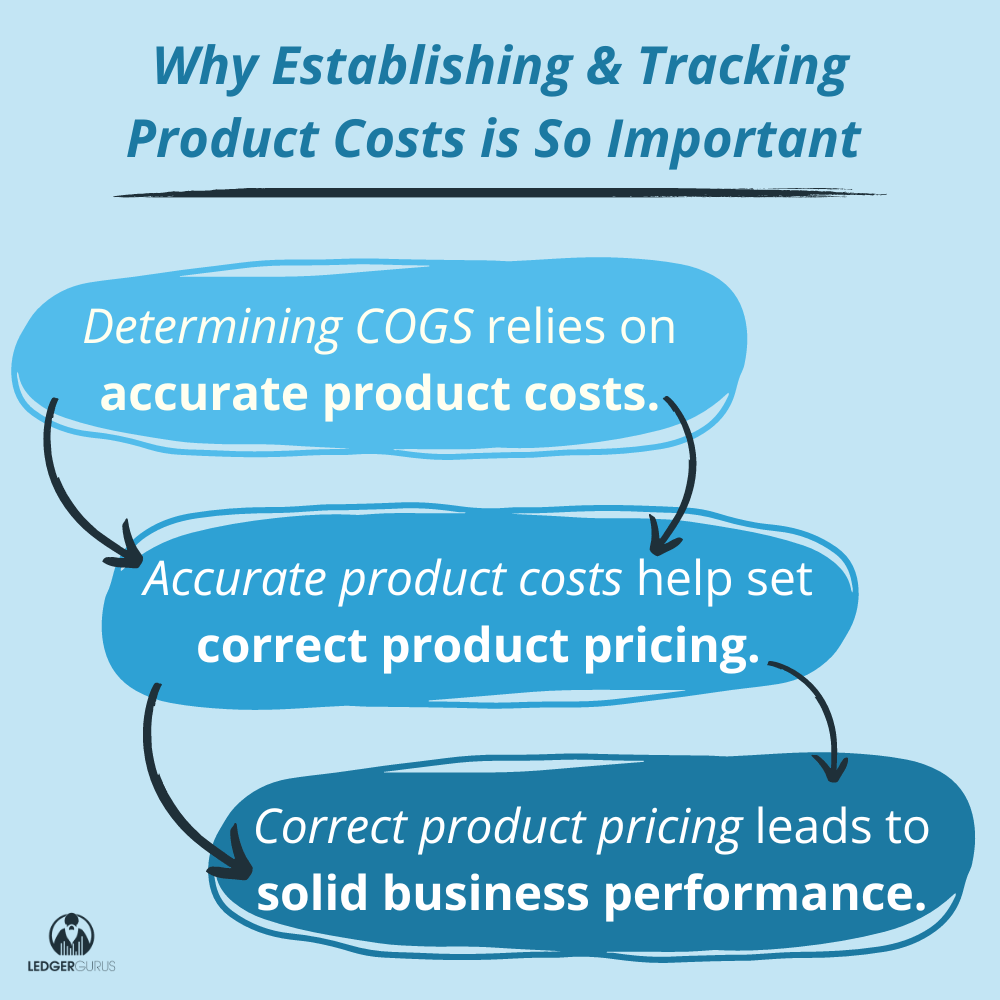

Simply put, product costs are all the direct and indirect expenses a manufacturer incurs to create a product. They’re the costs that are directly tied to bringing a tangible item into existence. These costs get "stuck" to the product until it's sold. Until then, they chill out on the balance sheet as inventory. Think of them as tiny hitchhikers, clinging on for the ride.

The Usual Suspects: Product Cost Edition

Let's break down the main players in this cost-conscious drama. We've got three main categories:

Must Read

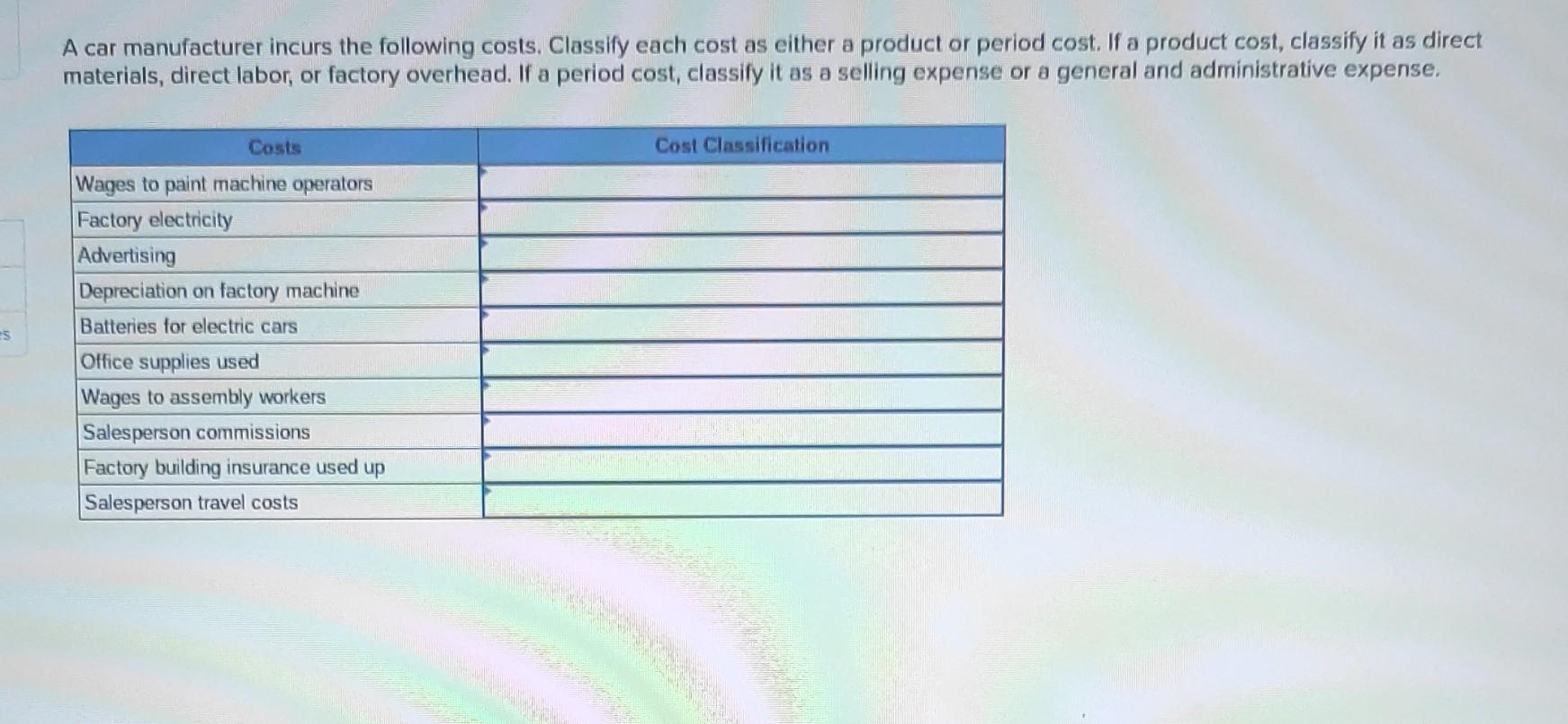

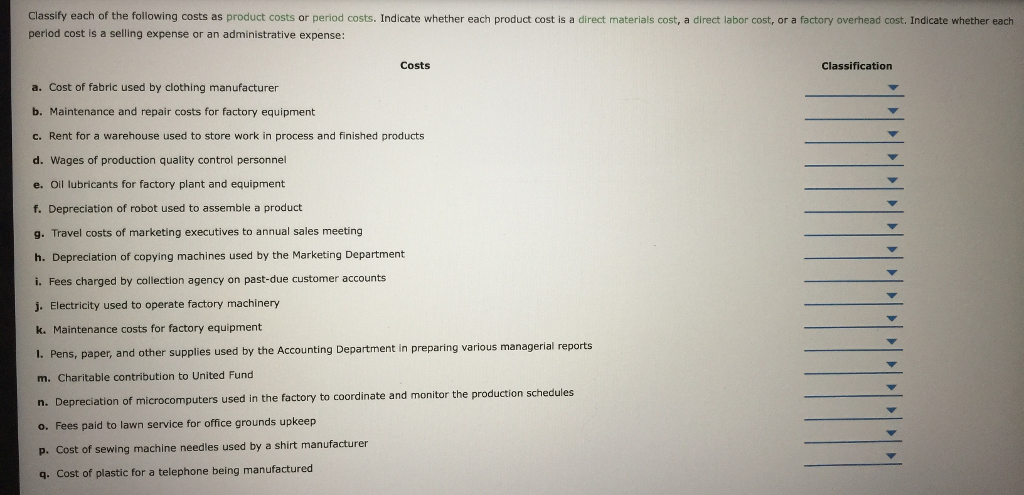

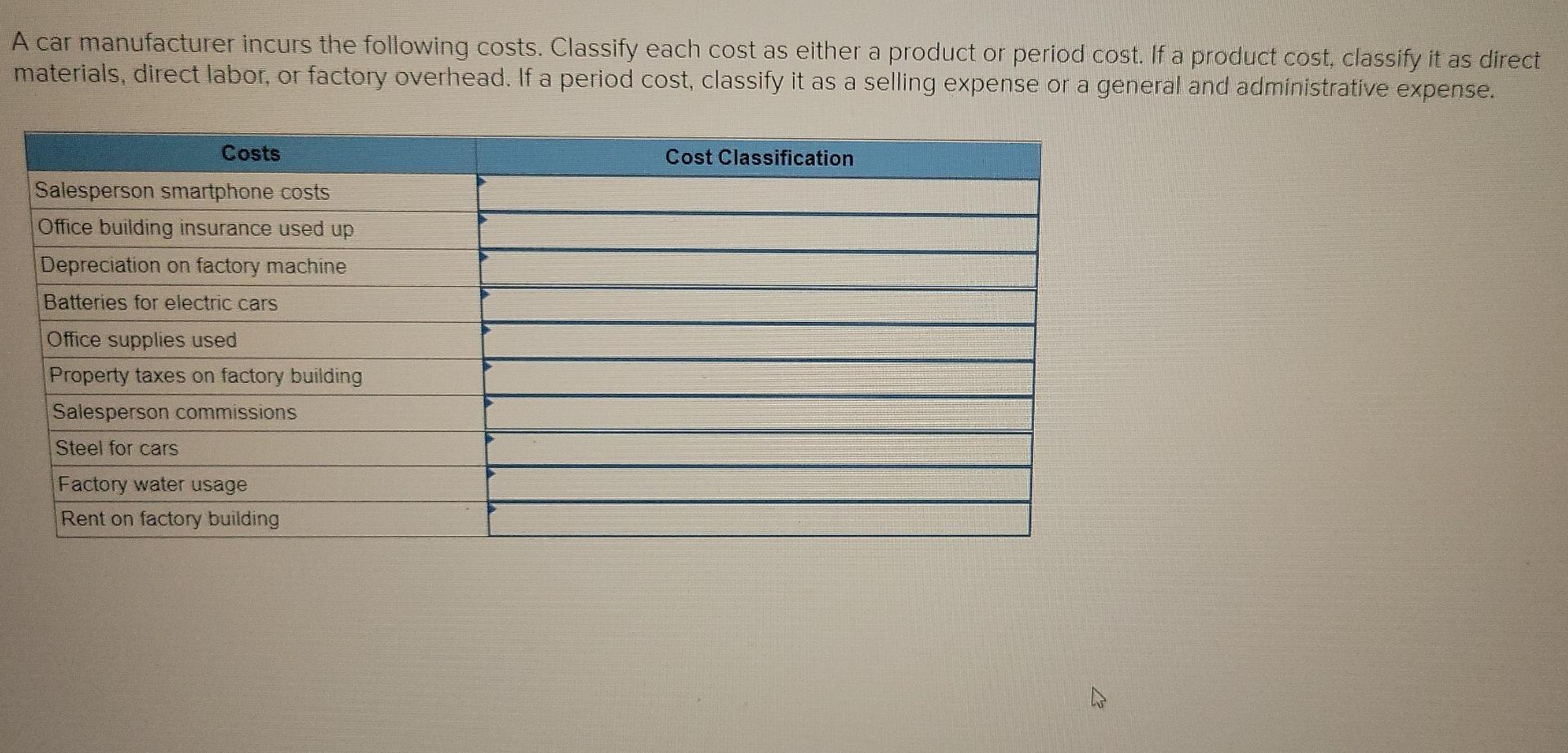

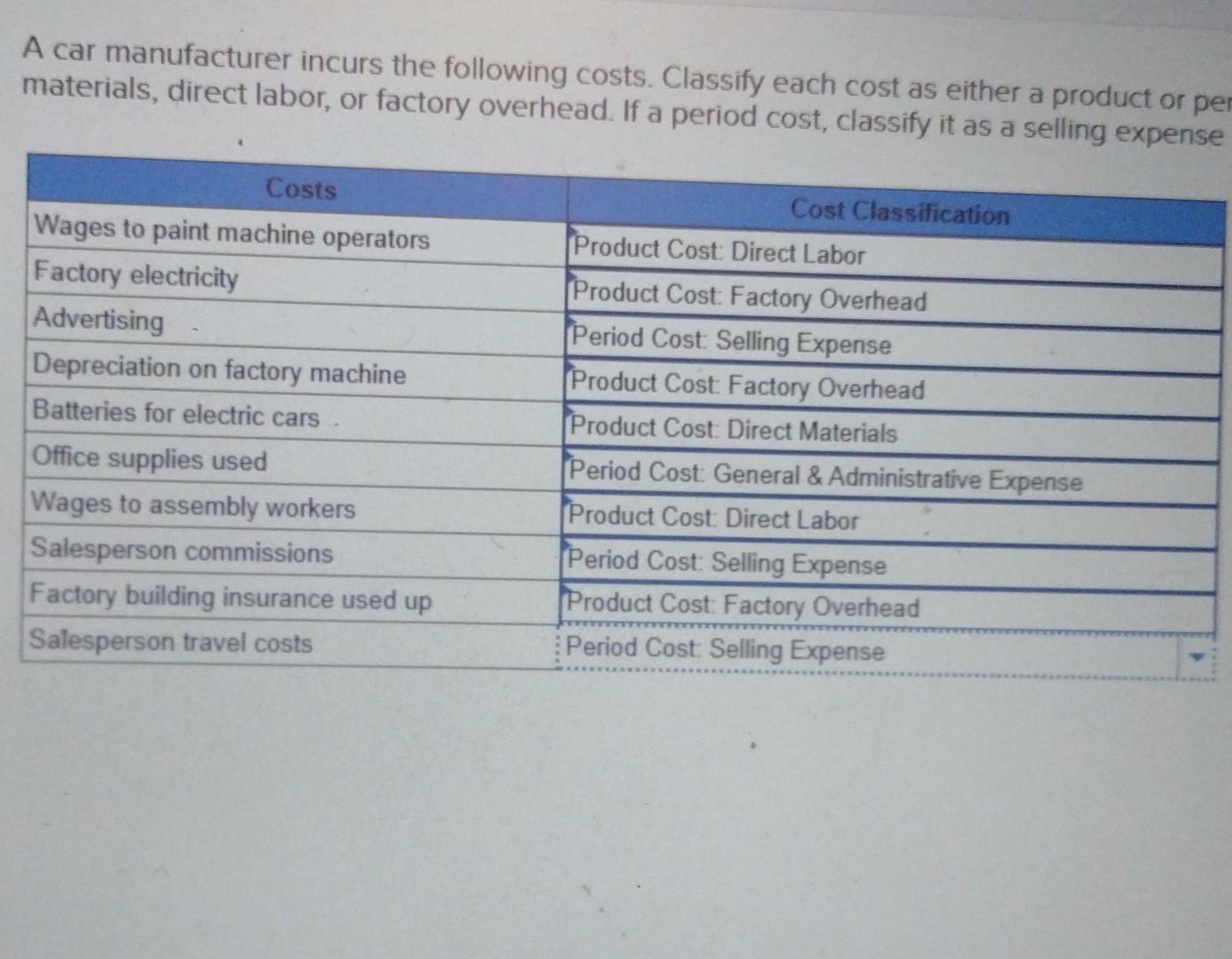

1. Direct Materials: This one’s pretty straightforward. It's all about the raw stuff that becomes your product. Wood for a chair? Direct material! The screen for your smartphone? Direct material! The glitter for that unicorn figurine? Definitely direct material. If you can physically touch it in the finished product, it's likely a direct material. Just imagine the manufacturer running around, gathering up all the ingredients. Fun, right?

2. Direct Labor: These are the wages paid to the folks who are directly involved in making the product. The person assembling the chair? Direct labor! The person soldering the circuits on your smartphone? Direct labor! The person meticulously gluing glitter onto those unicorn figurines (again, yes, the glitter requires a person, probably)? Direct labor! It's important these people touch the product directly and are part of the manufacturing process.

3. Manufacturing Overhead: Ah, the big catch-all category! This is where things get a little more interesting. Manufacturing overhead includes all the other costs incurred in the factory except direct materials and direct labor. It's basically everything else that keeps the manufacturing process humming along. Think of it as the supporting cast for the main event.

Examples of Manufacturing Overhead (aka the Supporting Cast)

This list could go on forever, but here are a few key players:

- Indirect Materials: These are materials used in the manufacturing process but aren't directly part of the finished product. Think glue, sandpaper, cleaning supplies for the factory, and oil for the machinery. The paper towels in the breakroom? Probably overhead, but probably not "manufacturing" overhead. (Accountants LOVE details!)

- Indirect Labor: These are the wages of people who support the manufacturing process but don't directly assemble the product. Think factory supervisors, maintenance workers, and security guards.

- Factory Rent & Utilities: You gotta keep the lights on (and the machines running)!

- Depreciation on Factory Equipment: Those machines don't last forever, sadly.

- Factory Insurance: Gotta protect that precious factory!

What Isn't a Product Cost? Hold On To Your Hats!

Now, let's talk about what doesn't make the cut. Costs incurred outside the factory aren't typically included in product costs. These are called period costs. We are talking about things like:

- Marketing Expenses: Gotta get the word out about those unicorn figurines!

- Sales Commissions: Pay the folks who sell 'em!

- Administrative Expenses: The salaries of the CEO and the accounting department. Important, but not directly related to making the actual product.

Putting it All Together: A Mini Quiz!

Okay, time to test your knowledge! Which of the following are product costs for a manufacturer?

- The cost of wood used to build tables?

- The salary of the factory foreman?

- The cost of advertising the tables?

- Depreciation on the factory equipment?

…Drumroll, please!… The correct answers are 1, 2, and 4! The cost of advertising is a period cost, not a product cost. You got this!

I hope that helps clarify those pesky product costs. It might seem confusing at first, but the key is to break it down and remember the basic categories: direct materials, direct labor, and manufacturing overhead.

Remember, understanding product costs helps manufacturers make informed decisions about pricing, production levels, and overall profitability. Knowledge is power, my friend!

Now go forth and conquer the world of cost accounting! You've got this!