What States Allow Reverse Mortgage At Age 55

Think of your home. It's more than just bricks and mortar; it's a haven, a place of memories, and often, a significant source of wealth. Many people, as they approach or enter retirement, start considering how to best leverage that wealth to enjoy their golden years to the fullest. One avenue that's gaining traction is the reverse mortgage, offering a way to tap into home equity without having to sell. But what if you're not quite at traditional retirement age? What if you're 55 and thinking about a reverse mortgage? Let's dive in.

The core purpose of a reverse mortgage is simple: it allows homeowners aged 62 and older to borrow against the equity in their homes, receiving the funds as a lump sum, a monthly payment, a line of credit, or a combination of these. The borrower doesn't make monthly mortgage payments; instead, the loan balance grows over time as interest and fees accrue. The loan is repaid when the borrower sells the home, moves out, or passes away. The appeal? It provides extra income, funds home improvements, or covers healthcare costs without dipping into savings.

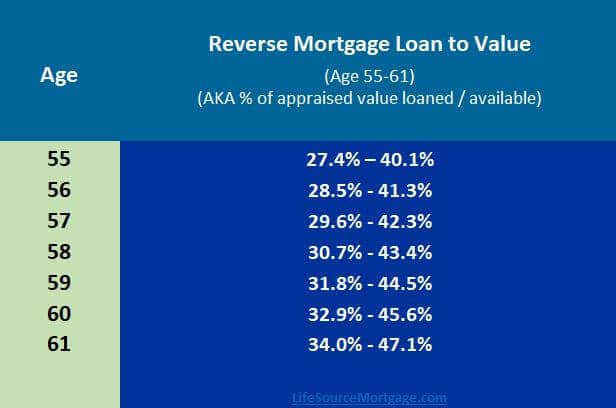

However, the standard government-insured Home Equity Conversion Mortgage (HECM) requires borrowers to be at least 62. That's where proprietary reverse mortgages come in. These are offered by private lenders and aren't subject to the same age restrictions as HECMs. This means that while HECMs have a firm 62-year-old lower age limit, proprietary reverse mortgages can be available to homeowners as young as 55, depending on the lender and the state they live in. Unfortunately, there isn't a definitive list of states where reverse mortgages for 55-year-olds are explicitly allowed. It heavily depends on individual lender policies and state regulations, which can change. Some states with potentially more options might be those with larger populations of homeowners nearing retirement, where there's greater market demand for such products.

Must Read

The benefits for someone at 55 are clear. Perhaps you're facing unexpected medical expenses, want to renovate your home to age in place comfortably, or need funds to start a new business venture. A reverse mortgage could provide the financial cushion you need. Imagine being able to fix up your kitchen, ensuring it’s accessible and safe for the future, without having to worry about immediate monthly payments. Or picture launching that small business you’ve always dreamed of, using your home equity to secure your financial future.

But how can you approach this effectively? First, research thoroughly. Don't jump at the first offer you see. Contact several lenders, compare their terms, fees, and interest rates. Second, understand the fine print. Reverse mortgages can be complex, so make sure you fully grasp the loan terms, repayment obligations (taxes and insurance still need to be paid!), and potential consequences of default. Third, seek professional advice. Talk to a financial advisor or housing counselor who can help you assess whether a reverse mortgage is the right choice for your individual circumstances. They can provide unbiased guidance and help you avoid potential pitfalls. Consider that while you don't make monthly mortgage payments, you are responsible for property taxes and homeowner's insurance. Failure to pay these can lead to foreclosure, so it's crucial to factor these ongoing costs into your budget.

Finally, remember that a reverse mortgage is a significant financial decision. Approach it with careful planning and due diligence to ensure it helps you achieve your financial goals and enhances your quality of life in the years to come. It's about making informed choices that empower you to live comfortably and securely.