What Percentage Of Your Income Should Be Mortgage

So, you're thinking of buying a home and you're wondering what percentage of your income should go towards your mortgage. Well, you're not alone! This is a question that has puzzled many a prospective homeowner. The good news is that there's a general guideline to help you figure it out.

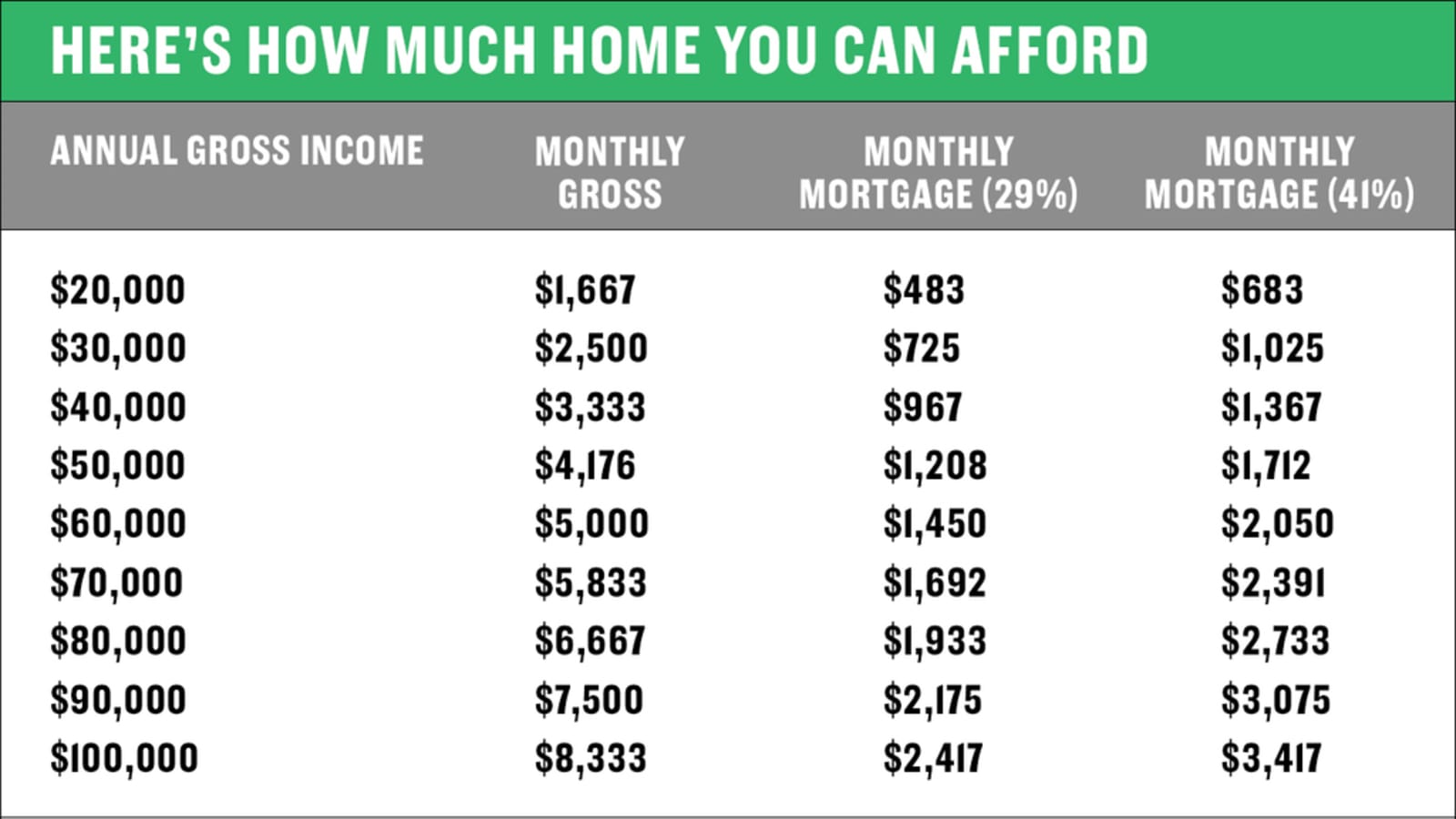

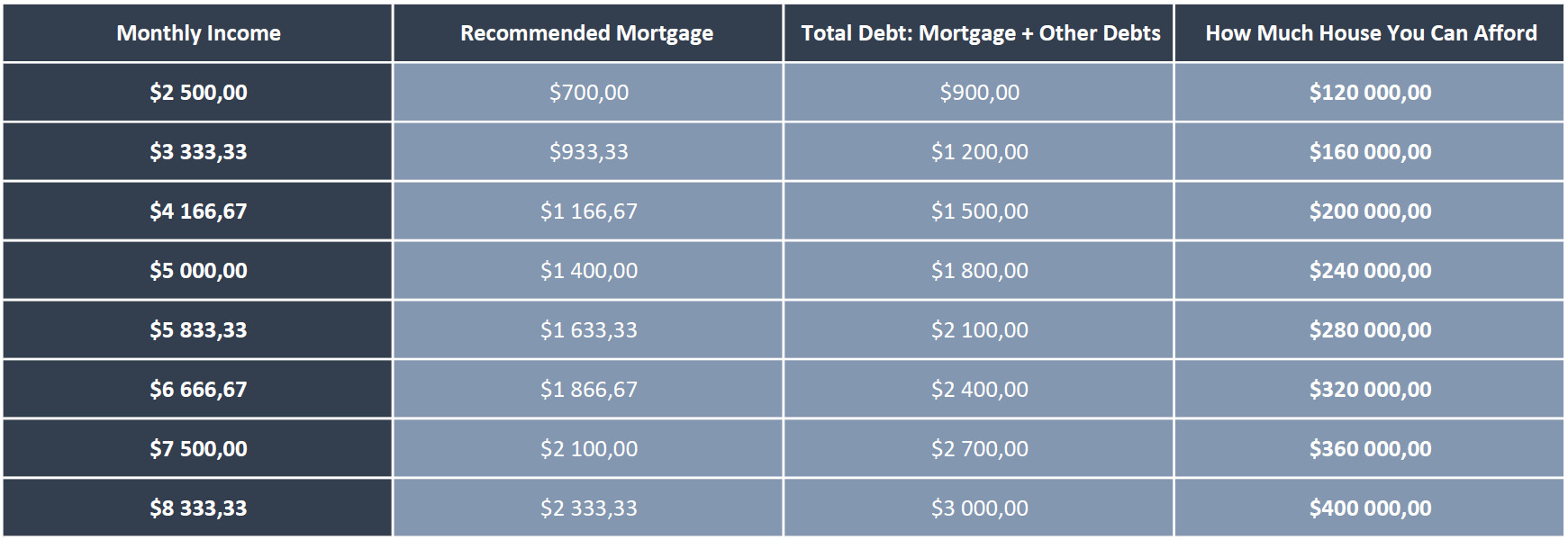

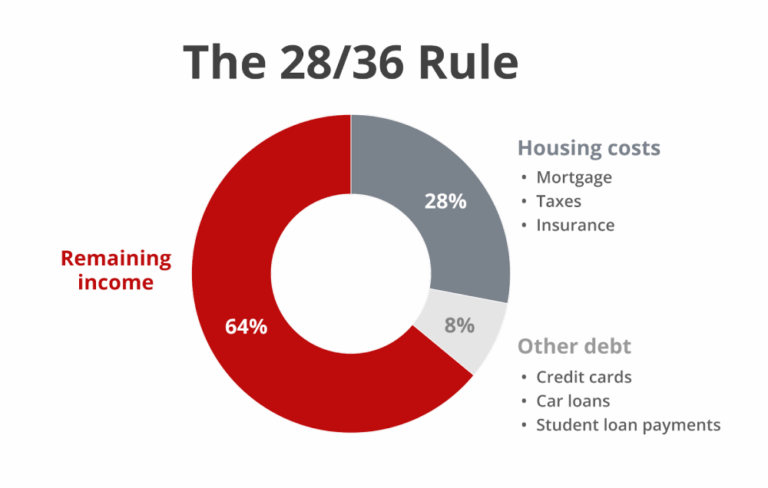

In general, it's recommended that you spend no more than 30% of your gross income on mortgage payments, property taxes, and insurance. This is often referred to as the front-end ratio. But why is this percentage so important? The answer is simple: it's all about affordability. You want to make sure you have enough money left over for other expenses, like food, transportation, and entertainment.

The Importance of Budgeting

Budgeting is key when it comes to determining how much of your income should go towards your mortgage. You need to consider all your expenses, including credit card debt, student loans, and other financial obligations. As financial expert Dave Ramsey says,

"You must budget to achieve financial stability. It's not about being frugal, it's about being wise with your money."So, take some time to review your budget and see where your money is going.

Must Read

Another important factor to consider is the back-end ratio, which includes all your debt payments, including credit cards, car loans, and student loans. It's recommended that you spend no more than 43% of your gross income on these expenses. This will help you avoid debt overload and ensure you have enough money for savings and investments.

What About Other Expenses?

When figuring out what percentage of your income should go towards your mortgage, don't forget to consider other expenses like property taxes and insurance. These costs can add up quickly, so make sure you factor them into your budget. As real estate expert Suze Orman says,

"You must consider all the costs of homeownership, including property taxes and insurance, to ensure you're making a smart investment."It's also important to think about maintenance costs, like repairs and renovations, which can be unpredictable and expensive.

In addition to these expenses, you should also consider your credit score and interest rate. A good credit score can help you qualify for a lower interest rate, which can save you thousands of dollars over the life of your loan. So, make sure you check your credit report regularly and work on improving your score if necessary.

Conclusion

So, what percentage of your income should be mortgage? The answer is, it depends on your individual circumstances. But as a general guideline, aim to spend no more than 30% of your gross income on mortgage payments, property taxes, and insurance. And don't forget to consider all your other expenses, including credit card debt, student loans, and maintenance costs. By following these guidelines and being mindful of your budget, you can make a smart investment in your dream home and achieve long-term financial stability.

Ultimately, the key to successful homeownership is finding a balance between your mortgage payments and your other expenses. As financial advisor Jean Chatzky says,

"It's all about finding a balance between enjoying your life today and saving for tomorrow. With careful planning and budgeting, you can achieve your financial goals and live comfortably in your dream home."So, take the time to review your budget, consider all your expenses, and find a mortgage that works for you.