What Is The Point At Which Supply And Demand Intersect

Ever tried selling your slightly-used, definitely-not-antique porcelain cat collection at a garage sale? Or maybe you’ve been desperately hunting down the last bag of Flamin' Hot Cheetos in a five-mile radius? If so, you’ve already tangoed with the mysterious forces of supply and demand.

The Great Economic Meet-Cute

Now, picture supply and demand as two awkward teenagers at a middle school dance. Supply is that shy kid who brought a ton of extra cookies, just in case. He's hoping people want them. Demand is the popular kid who's got their eye on those cookies, but only if they're the right kind and the price is right.

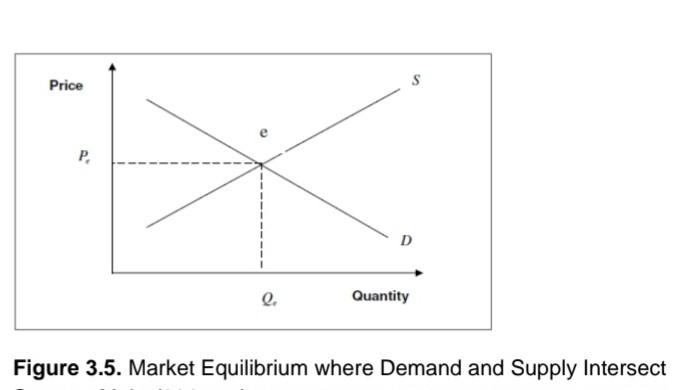

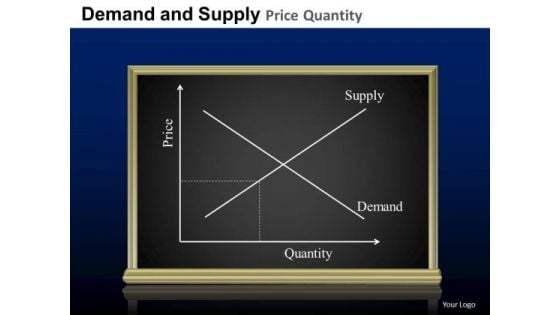

The point where these two finally lock eyes and awkwardly shuffle onto the dance floor is what we call the equilibrium point, or the market clearing price. It's that sweet spot where the quantity of goods or services suppliers are willing to offer perfectly matches the quantity consumers are willing to buy. It's like economic harmony, baby!

Must Read

Supply: The 'How Many We Got?' Side

Let's break it down. Supply is all about how much of something is available. Think about it: if your local bakery only makes five blueberry muffins a day, that's the supply. If they suddenly start churning out 500, the supply has dramatically increased. Usually, the higher the price, the more suppliers want to supply. It's simple human (or baker) nature – more money, more motivation!

Imagine your grandma knitting scarves. If she can only sell them for $5 a pop, she might only knit one or two. But if someone's willing to shell out $50 for a hand-knitted scarf (maybe it's got a celebrity endorsement!), she'll be knitting like a woolly, whirlwind grandma machine.

Demand: The 'I Want It NOW!' Side

Demand, on the other hand, is all about how much people want something. And crucially, how much they're willing to pay for it. Generally, the lower the price, the more people want it. Makes sense, right? A Lamborghini for $1? Everyone wants one! A slightly used sock for $1,000? Probably not so much.

Remember those Flamin' Hot Cheetos? If they're readily available everywhere, the demand isn't as fierce. But if there's a national shortage because of, say, a rogue squirrel attack on the Cheeto factory (hypothetically speaking, of course!), demand skyrockets. People are willing to pay a premium just to get their spicy, cheesy fix.

The Intersection: Where the Magic Happens (and Prices are Set)

So, what happens when supply and demand finally meet? Well, that's where the price is determined. If there are tons of cookies available (high supply) and not many hungry kids (low demand), the price of the cookies will likely be low. Maybe even free! But if there's only one cookie left and everyone is starving (low supply, high demand), someone's going to pay a hefty price for that cookie.

That magic intersection isn't just some theoretical concept. It's happening all around you, all the time. It's why gas prices fluctuate, why concert tickets sell out in minutes, and why that limited-edition Beanie Baby you hoarded in 1998 is now worth approximately… well, probably less than you paid for it.

Think of it this way:

- Too much supply, not enough demand? Clearance sale! Bargain bin bonanza!

- Not enough supply, too much demand? Prepare to pay a premium, my friend. Prepare to battle it out.

Finding the Balance: It's All About the Equilibrium

The equilibrium point is the economic sweet spot. It's where everyone is relatively happy (or at least, not actively complaining too much). Suppliers are making enough money to keep producing, and consumers are getting the goods or services they want at a price they're willing to pay.

Of course, things rarely stay in perfect equilibrium for long. Tastes change, new technologies emerge, and rogue squirrel attacks happen. But understanding the basic principles of supply and demand and how they intersect can help you make sense of the economic world around you – and maybe even snag a good deal on a slightly used porcelain cat.