What Do Mortgage Brokers Look For On Bank Statements

Imagine you're ABOUT to embark on the journey of buying your dream home, but there's a crucial step that can either make or break the deal: the mortgage application process. It's a moment when every little detail matters, and one aspect that's under intense scrutiny is your bank statement. The document speaks volumes about your financial health, providing a snapshot of your spending habits, income, and ability to manage your money. But have you ever wondered what exactly mortgage brokers look for when reviewing these statements? It's time to dive into the world of financial assessment and uncover the secrets that lie within those pages of transactions.

The history of mortgage brokering dates back to the 1980s, when it first emerged as a distinct profession. Over the years, the role of a mortgage broker has evolved significantly, from merely acting as a bridge between lenders and borrowers to becoming a key financial advisor who guides clients through the complex landscape of loan options. Today, with the rise of digital banking and online transactions, the way mortgage brokers analyze bank statements has also transformed. Gone are the days of manual checks; now, advanced algorithms and software are used to assess creditworthiness with unprecedented precision.

So, why does it matter what mortgage brokers find on your bank statement? The answer lies in the risk assessment process. Lenders need to gauge the likelihood of you repaying the loan, and your bank statement is a critical tool in this evaluation. By examining your account activity, brokers can identify potential red flags such as overdrafts, late payments, or unusual transactions that might indicate financial instability. On the other hand, a clean and healthy bank statement can significantly strengthen your mortgage application, making you a more attractive candidate for lenders. It's a delicate balance of financial responsibility and prudent management, all reflected in those seemingly mundane pages of transactions.

Must Read

Delving Deeper: The Anatomy of a Bank Statement

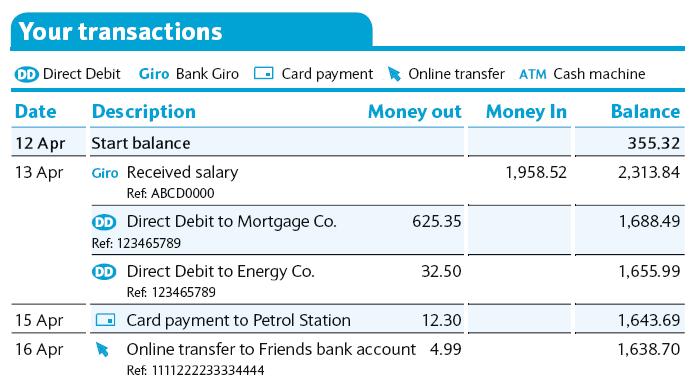

When a mortgage broker reviews your bank statement, they're not just looking at the numbers; they're analyzing the narrative it tells about your financial life. The account balance is, of course, a crucial figure, but it's the transactions that provide the real insight. For instance, regular deposits from your employer can demonstrate a stable income, while large withdrawals might raise questions about your spending habits. The presence of direct debits for utility bills or loan repayments can indicate responsibility, as it shows you're committed to meeting your financial obligations. However, overdraft fees or returned payments can tell a different story, one of potential financial stress or poor planning.

Mortgage brokers are also on the lookout for unusual activity, such as sudden large deposits or international transactions, which might necessitate further explanation. The source of these funds is critical; if they're from a legitimate source like a gift from a family member or inheritance, it's less of a concern. However, if the funds are from an unknown or suspicious source, it could lead to additional scrutiny. The goal is to ensure that the borrower's financial situation is transparent and stable, with no hidden risks that could impact the mortgage repayments.

In this age of digital banking, mortgage brokers must also consider the impact of online transactions and e-commerce activity. With the rise of contactless payments and mobile banking apps, the lines between personal and business transactions can sometimes blur. This is where the broker's expertise comes into play, as they need to accurately differentiate between personal expenses and business-related transactions, ensuring that the borrower's financial health is accurately represented. It's a complex task, requiring a deep understanding of both financial regulations and the nuances of modern banking practices.

The psychological aspect of reviewing bank statements should not be underestimated. Mortgage brokers are not just analyzing numbers; they're also gaining insight into the borrower's financial mindset and behavioral patterns. A person who regularly saves a portion of their income or makes timely payments might be viewed more favorably than someone with a history of impulsive purchases or late payments. It's about demonstrating a commitment to financial responsibility, a trait that lenders associate with lower risk and higher creditworthiness.

Scenarios and Strategies: Navigating the Mortgage Application Process

For prospective homebuyers, understanding what mortgage brokers look for in bank statements can be a game-changer. By preparing wisely, borrowers can strengthen their application and increase their chances of securing a favorable mortgage deal. One strategy is to maintain a healthy account balance for several months leading up to the application, demonstrating financial stability. Additionally, avoiding large purchases or significant changes in spending habits can prevent raising unnecessary red flags. It's also essential to ensure that all transactions are legitimate and traceable, as unexplained funds or suspicious activity can complicate the application process.

Another critical aspect is credit score management. While bank statements provide a snapshot of current financial health, credit scores reflect long-term credit behavior. Borrowers should check their credit reports for errors, work on improving their credit score if necessary, and avoid applying for multiple credit cards or loans in the months leading up to the mortgage application. This demonstrates a responsible approach to credit and can positively impact the mortgage broker's assessment. Furthermore, building an emergency fund can provide a cushion against financial shocks, showing lenders that you're prepared for the unexpected.

In some cases, borrowers may face unique challenges, such as being self-employed or having a variable income. For these individuals, it's crucial to provide comprehensive documentation, including detailed financial statements and tax returns, to give mortgage brokers a clearer picture of their financial situation. Sometimes, seeking the advice of a financial advisor can be beneficial, as they can offer tailored strategies to improve financial stability and mortgage eligibility. It's about presenting a strong financial case that aligns with the lender's requirements.

Finally, communication is key. If there are any unusual transactions or concerns on the bank statement, it's better to address them proactively. Providing a clear explanation or supporting documentation can alleviate potential issues and demonstrate transparency, which is highly valued by lenders. This proactive approach not only facilitates a smoother application process but also builds trust between the borrower and the mortgage broker, potentially leading to a more favorable outcome.

Frequently Asked Questions

How Do Mortgage Brokers Handle Bank Statements with Multiple Incomes or Complex Financial Situations?

Mortgage brokers are trained to handle a variety of financial scenarios, including those with multiple incomes or complex financial situations. When reviewing bank statements for individuals with non-traditional income sources, such as the self-employed or those with investment income, brokers will often require additional documentation to accurately assess creditworthiness. This might include business financial statements, tax returns, or letters from accountants explaining the nature of the income. The goal is to understand the stability and sustainability of the income, ensuring that it can support the mortgage repayments.

In cases where borrowers have complex financial situations, such as shared bank accounts or joint investments, clear explanations and supporting documentation are essential. Mortgage brokers need to differentiate between personal and business-related transactions, which can sometimes be challenging. However, by providing a detailed breakdown of income and expenses, and explaining the purpose of each transaction, borrowers can help facilitate a more accurate assessment of their financial health. It's a collaborative process that requires transparency and a willingness to provide comprehensive information.

Can Mortgage Brokers Accept Bank Statements with Some Overdrafts or Late Payments?

While overdrafts and late payments on a bank statement can raise concerns, they don't necessarily mean a mortgage application will be rejected. The impact of these issues depends on their frequency, severity, and the overall context of the borrower's financial situation. If the overdrafts are infrequent and quickly rectified, or if late payments are isolated incidents with a valid explanation, mortgage brokers might view them as minor blips rather than indicative of a deeper financial issue. However, a pattern of overdrafts or repeated late payments could suggest poor financial management, potentially affecting the lender's willingness to approve the mortgage.

In some cases, borrowers might be able to mitigate the impact of overdrafts or late payments by providing a clear explanation for the issues and demonstrating a commitment to improving their financial habits. This could involve creating a budget, setting up direct debits for bill payments, or seeking advice from a financial advisor. By showing that they're proactive about their financial health and willing to make changes, borrowers can sometimes overcome initial concerns and secure a mortgage offer. It's about demonstrating financial responsibility and a willingness to learn and adapt.

How Can Borrowers Prepare Their Bank Statements to Ensure a Smooth Mortgage Application Process?

Preparing for a mortgage application involves more than just gathering documents; it's about presenting a strong financial case that showcases your creditworthiness. One of the first steps borrowers can take is to review their bank statements for any errors or discrepancies, ensuring that all transactions are accurately recorded and easily explainable. It's also wise to avoid large purchases or significant changes in spending habits in the months leading up to the application, as these can raise unnecessary questions about financial stability.

Borrowers should also focus on building a healthy account balance and maintaining a stable income. This demonstrates financial responsibility and reduces the risk associated with lending. Furthermore, keeping detailed records of all financial transactions, including receipts, invoices, and bank statements, can be incredibly useful. These documents provide a clear picture of financial health, making it easier for mortgage brokers to assess the application and for lenders to make an informed decision. By being proactive and transparent, borrowers can navigate the mortgage application process with confidence, knowing they've presented their financial situation in the best possible light.

As we navigate the complex world of mortgage applications and financial assessments, it's clear that bank statements play a crucial role in determining creditworthiness. They offer a unique window into a borrower's financial life, revealing patterns of behavior and management that can make or break a mortgage deal. By understanding what mortgage brokers look for in these statements, prospective homebuyers can take proactive steps to strengthen their application, demonstrating their commitment to financial responsibility and stability.

The connection between bank statements and human nature is also fascinating. It reflects our relationship with money and our financial values. A well-managed bank account can indicate a disciplined approach to finances, while issues like overdrafts might suggest impulsivity or a lack of financial planning. This is why mortgage brokers don't just look at the numbers; they also try to understand the story behind the transactions, the motivations and habits that drive a borrower's financial decisions.

In the end, the process of securing a mortgage is not just about financial assessment; it's also about trust and transparency. Borrowers who can demonstrate a commitment to financial health, who are open about their transactions and proactive in managing their finances, are more likely to find favor with lenders. It's a mutual relationship built on confidence and responsibility, where both parties work together to achieve a common goal: securing a home and building a future.