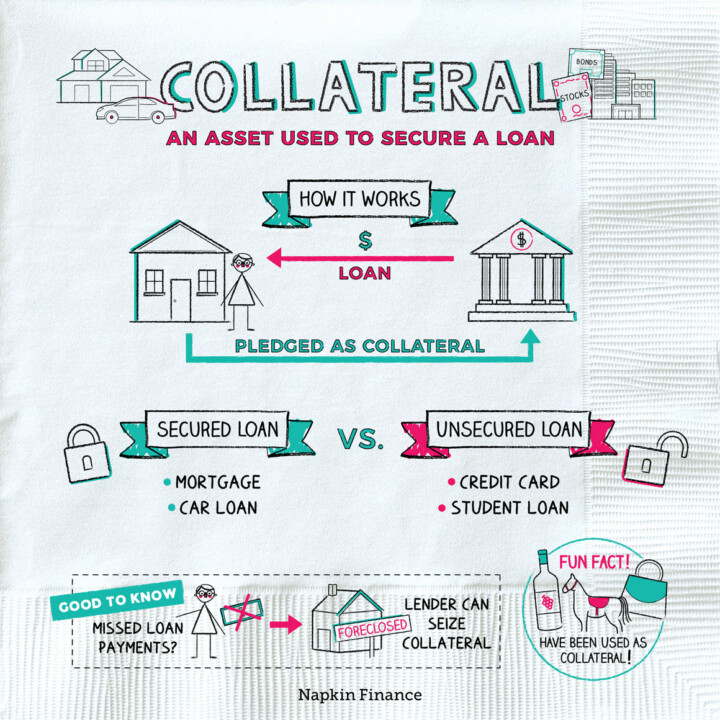

What Can Be Used For Collateral To Secure A Loan

So, you need a loan? Fantastic! But before the bank throws money at you (figuratively, of course!), they need a little something called collateral. Think of it as your promise in physical form. It's like saying, "Hey, I'm good for it, but just in case, here's something valuable you can have if I can't pay you back." What exciting treasures qualify? Let's dive in!

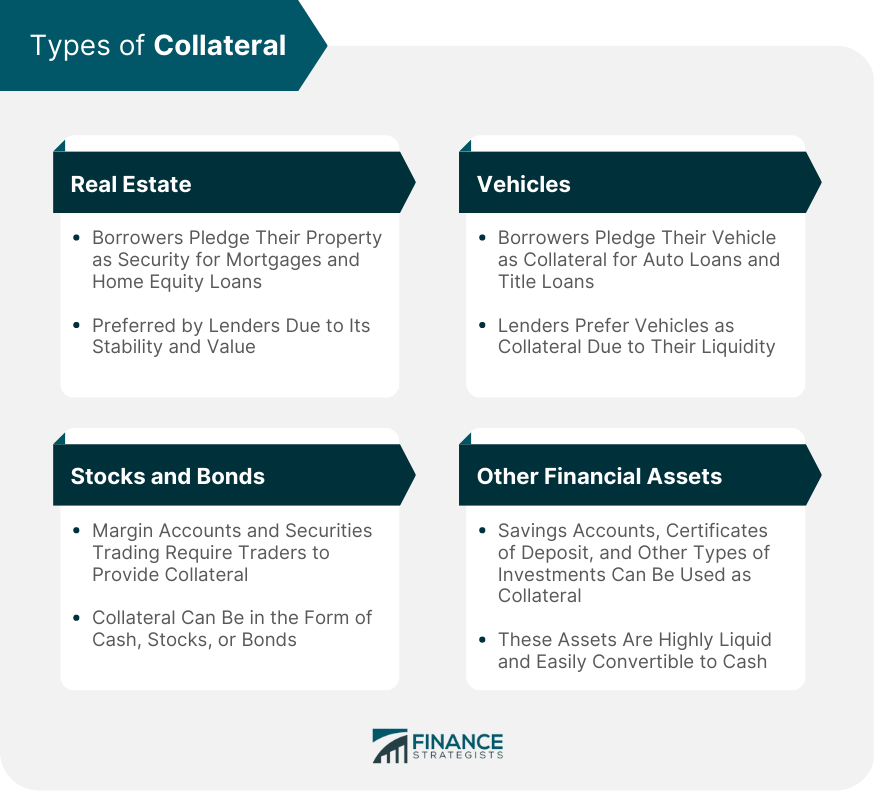

Your House: The Classic Choice

Ah, the home. The cornerstone of the American dream, and a super popular form of collateral! Getting a mortgage is basically the perfect example. The bank lends you money to buy the house, and the house itself becomes the collateral. If you stop making payments, well, the bank can, unfortunately, take back the house. Not ideal, but hey, that's how it works!

Your Car: Vroom Vroom!

Need a car loan? Your shiny new ride can be collateral! Just like with a house, the bank has a lien on the car title until you've paid off the loan. Think of it as a friendly little "IOU" attached to your four wheels. It's a pretty standard practice, so don't be surprised when they ask for it.

Must Read

Savings Accounts and CDs: Money Backing Money

Did you know that your own savings can help you borrow more? It’s true! If you have a Certificate of Deposit (CD) or a hefty savings account, you can often use it as collateral for a loan. It's like borrowing against your own future wealth. Feels a bit like cheating the system, doesn't it? But it’s totally legit!

Stocks and Bonds: Playing the Market

If you're a savvy investor, your stocks and bonds might be eligible for collateral. This can be a bit riskier, as the value of the market can fluctuate, but it also allows you to leverage your investments. Just make sure you understand the terms and potential pitfalls before you pledge your portfolio.

That Prized Possessions: Art, Jewelry, and Collectibles

Got a Picasso hanging on your wall? A diamond the size of your thumb? A baseball card collection worth more than your car? Some lenders might accept these as collateral. It's definitely less common, and you'll need a professional appraisal to determine the value. Imagine explaining to your friends that you took out a loan using your limited edition comic book as collateral. Now that’s a story!

Business Assets: For the Entrepreneurial Spirit

If you own a business, you can use various assets as collateral for a loan. This could include equipment, inventory, accounts receivable, or even real estate owned by the business. Lenders will assess the value and liquidity of these assets to determine the loan amount. It's all part of building that empire!

Insurance Policies: A Safety Net for Your Loan

Believe it or not, certain life insurance policies with a cash value can be used as collateral. This is especially true for whole life insurance policies. The cash value grows over time, making it a potential asset you can tap into. Who knew your life insurance could be so versatile?

What Doesn't Work as Collateral?

While almost anything with value could be considered, some things are generally a no-go. This usually includes things that are difficult to value, quickly depreciate, or are hard to seize. For example, your undying love for your pet goldfish probably won't cut it (sorry!).

:max_bytes(150000):strip_icc()/collateral-loans-315195-v3-5bc4cbf746e0fb002693d842.png)

So, there you have it! A whirlwind tour of the exciting world of collateral. It's a fascinating glimpse into how lenders assess risk and how you can leverage your assets to achieve your financial goals. Just remember to do your research, understand the terms, and always borrow responsibly! Good luck, and may your collateral always be on your side!

And remember, folks, that even though something can be used as collateral, it doesn't always mean it should be! Weigh the risks and benefits carefully before making any decisions.