Unused Line Of Credit On Balance Sheet

Hey! Grab a seat. Coffee's on me. Let's talk about something super exciting... well, maybe not super exciting, but important if you're even remotely interested in business finances: an unused line of credit on the balance sheet.

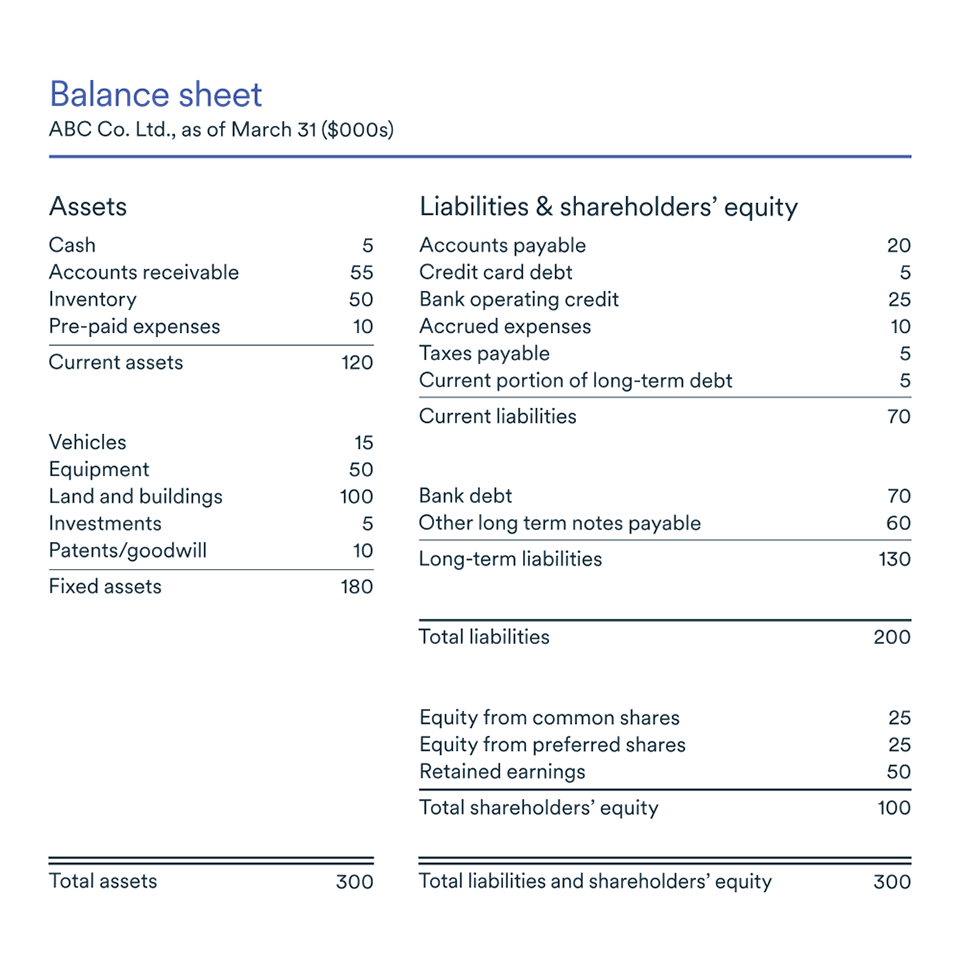

Now, a balance sheet? Sounds scary, right? Like some dusty old ledger guarded by a dragon. But honestly, it's just a snapshot. A picture of a company's assets, liabilities, and equity at a specific point in time. Think of it as a financial selfie.

What's a Line of Credit Anyway?

Okay, before we dive into the balance sheet of it all (pun intended!), let’s make sure we're all on the same page. A line of credit is basically pre-approved loan. Imagine having a credit card, but instead of swiping it for that essential new pair of shoes, it's for, you know, business stuff.

Must Read

The bank says, "Hey, we trust you. You can borrow up to $X amount whenever you need it." You only pay interest on what you actually use. Pretty neat, huh?

Unused? So... It's Just Sitting There?

Exactly! An unused line of credit is precisely that – a line of credit that a company has available but hasn't tapped into yet. It’s like having a spare tire in your trunk. You hope you never need it, but you're really glad it's there if you do.

Think of it this way: You have a magic money tree (we all wish, right?). You can pick the fruit (money) whenever you want, but you haven't picked any yet. The potential fruit is the unused line of credit.

So, Where Does It Live on the Balance Sheet?

This is where it gets a little... technical, but stick with me! The unused portion of a line of credit doesn't actually appear as an asset or liability on the balance sheet itself. Confused? Don't be! It's more like a footnote. A little whisper in the notes to the financial statements.

Why? Because it's not real money yet. It's potential borrowing power. Think of it as off-balance-sheet financing. It's important to know about, but doesn't affect the immediate asset/liability equation.

The used portion, however, does show up! If you borrow from the line of credit, that amount becomes a liability (specifically, a short-term liability, usually) on the balance sheet. Because, well, you owe it. That's how borrowing works!

Why Bother Having an Unused Line of Credit?

Great question! Why would a company pay fees to have access to money they're not using? Several reasons, actually:

- Peace of Mind: Remember the spare tire analogy? It provides a safety net. A cushion for unexpected expenses or temporary cash flow crunches. Let's say a huge client is late with payment. The line of credit can help bridge the gap.

- Financial Flexibility: Opportunities arise quickly! Need to buy that new equipment right now to snag a big contract? An unused line of credit gives you the power to pounce.

- Improved Credit Rating (Potentially): Believe it or not, having a line of credit and not using it can sometimes boost your creditworthiness. It shows responsibility! It's like saying, "Hey, I'm trustworthy! They even offered me money, and I didn't even need it!"

The Downside?

Of course, nothing's perfect. Even unused lines of credit have potential drawbacks. The main one? Fees! Banks often charge a fee (sometimes called a commitment fee) for making the line of credit available, even if you don't use it. It's like paying rent on an apartment you never live in. Ouch!

Also, remember that the interest rate on the line of credit can fluctuate. It's usually tied to some benchmark rate (like the prime rate), so it could become more expensive to borrow if interest rates rise.

Key Takeaways (because who doesn't love a good summary?)

Okay, so what should you remember from our little chat?

- An unused line of credit represents potential borrowing power.

- It doesn't appear directly on the balance sheet, but it's usually mentioned in the notes to the financial statements.

- It provides financial flexibility and a safety net.

- There are usually fees associated with having a line of credit, even if it's unused.

So, there you have it! The somewhat-exciting (okay, maybe mildly interesting) world of unused lines of credit. Now, who wants dessert?