Unsecured Line Of Credit For Bad Credit

Let's face it, nobody wants to be thinking about credit, especially when it’s less than stellar. But imagine a situation: your car needs a sudden repair, a family emergency crops up, or an unexpected bill arrives. In those moments, having access to funds can be a lifesaver. That's where the idea of an unsecured line of credit, even with bad credit, comes into play. It offers a potential solution for those financial hiccups that life throws our way, offering a flexible way to borrow money and manage unexpected expenses.

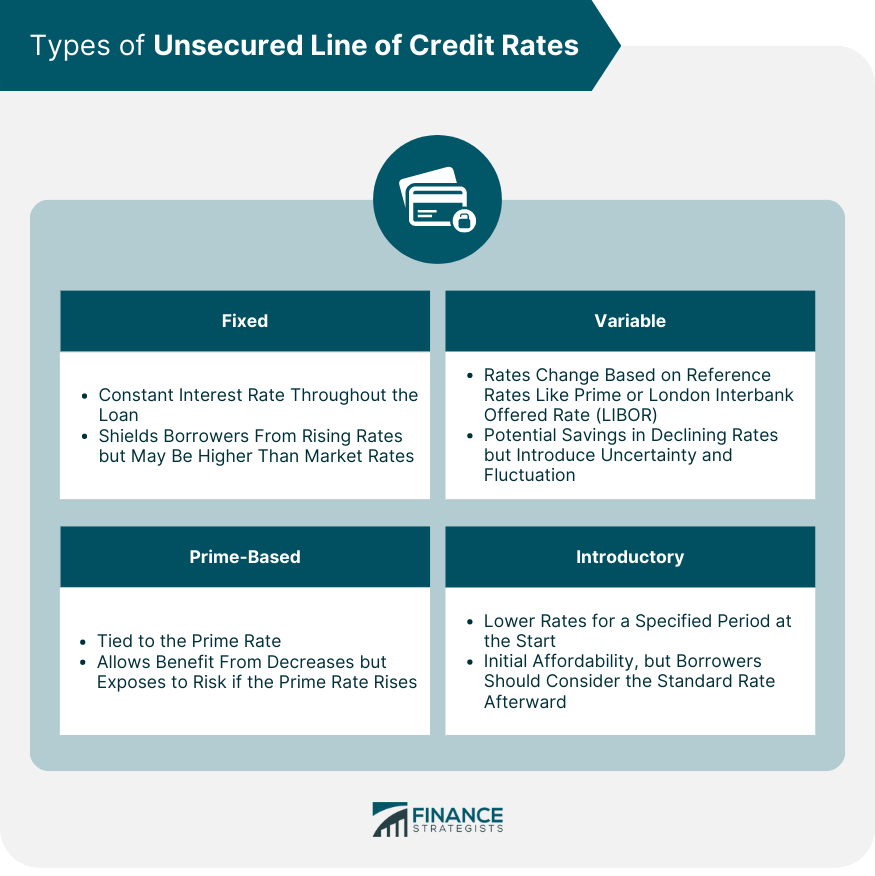

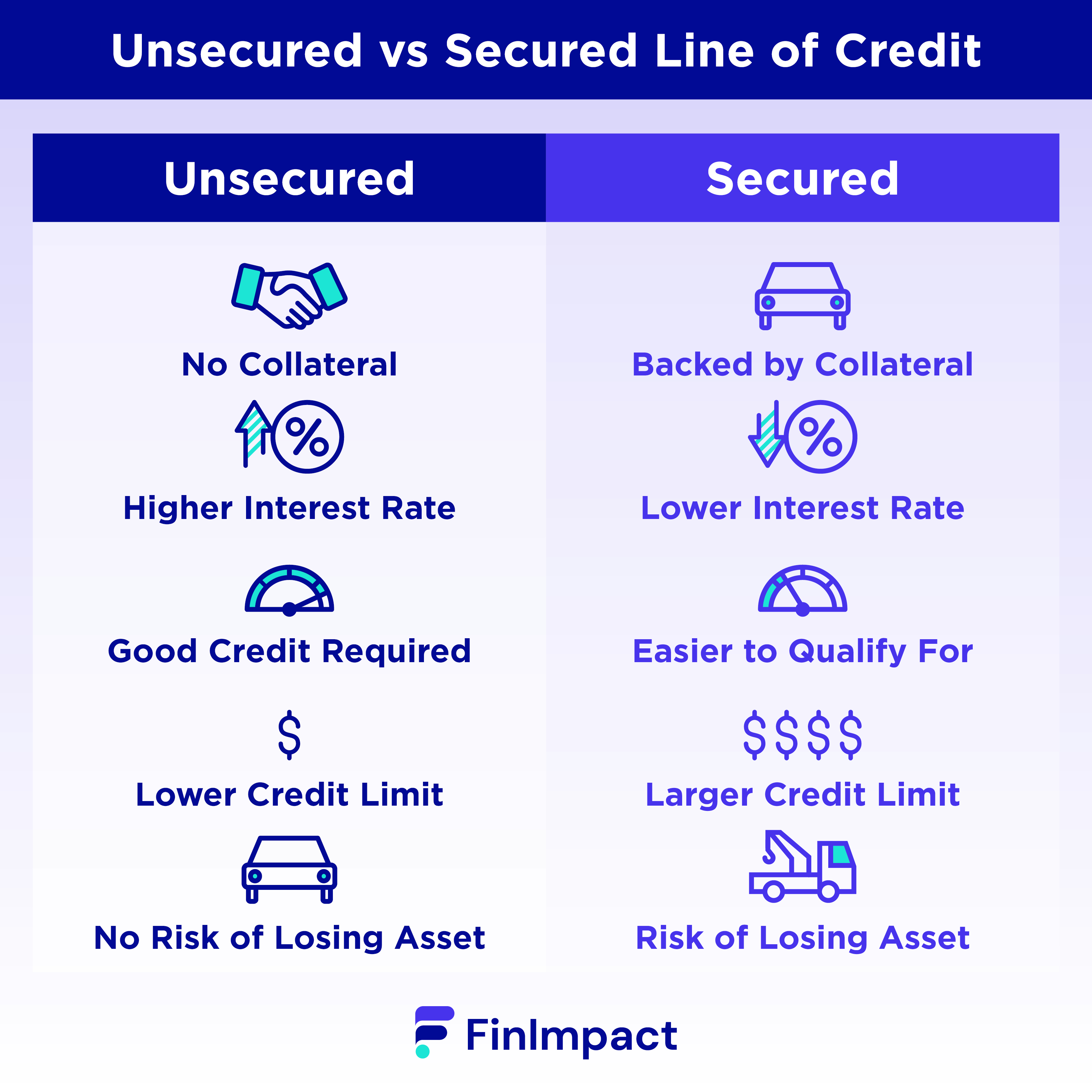

So, what exactly is an unsecured line of credit, especially when we’re talking about bad credit? Simply put, it's a pre-approved amount of money you can borrow and repay as needed. The "unsecured" part means it's not backed by any collateral like your house or car. This makes it riskier for the lender, hence the typical higher interest rates and fees associated with them, particularly for individuals with a lower credit score. However, the beauty lies in its flexibility. You only borrow what you need and only pay interest on what you borrow. Think of it as a financial safety net, ready to catch you when you stumble.

The purpose it serves in everyday life is primarily to handle those unforeseen expenses. Imagine your refrigerator giving up the ghost right before a big holiday. Or perhaps you have a sudden medical bill that your insurance doesn't fully cover. An unsecured line of credit can help you bridge that gap, allowing you to handle the situation without derailing your entire budget. Some people even use it for smaller, strategic purposes, such as consolidating smaller debts with potentially even higher interest rates or handling emergency travel expenses.

Must Read

Common examples of how people apply this include using the credit line to pay for auto repairs (as mentioned earlier), covering unexpected medical costs, handling urgent home repairs (like a leaky roof), or even managing expenses related to a job loss until you can secure new employment. The key is to use it responsibly and only when absolutely necessary.

Now, how can you enjoy this financial tool more effectively, especially if you're dealing with less-than-perfect credit? Here are a few practical tips:

- Shop around: Don't settle for the first offer you see. Compare interest rates, fees, and repayment terms from multiple lenders. Even small differences can add up over time.

- Borrow only what you need: Just because you're approved for a certain amount doesn't mean you have to use it all. Only borrow what you absolutely need to avoid unnecessary interest charges.

- Make timely payments: This is crucial. Late payments can negatively impact your credit score and trigger additional fees. Set up automatic payments to ensure you never miss a due date.

- Create a repayment plan: Don't just rely on the minimum payment. Develop a strategy to pay off the balance as quickly as possible. The faster you pay it down, the less interest you'll accrue.

- Improve your credit score: Use the line of credit responsibly to demonstrate your ability to manage debt. This can help you improve your credit score over time, potentially leading to better interest rates and terms in the future.

- Consider alternatives: Before relying on an unsecured line of credit, explore other options like negotiating with creditors, seeking assistance from non-profit organizations, or borrowing from friends or family.

Ultimately, an unsecured line of credit for bad credit can be a valuable tool, but it's essential to approach it with caution, responsibility, and a clear understanding of the terms and conditions. Use it wisely, and it can be a stepping stone to improving your financial situation.