Revolving Line Of Credit For Bad Credit

Okay, so you're thinking about a revolving line of credit, huh? And your credit score... well, let's just say it's seen better days. Don't sweat it! You're definitely not alone. Life happens, right? Sometimes your credit takes a nosedive. But guess what? Even with a less-than-stellar credit score, it is possible to snag a revolving line of credit. Let’s dive in, shall we?

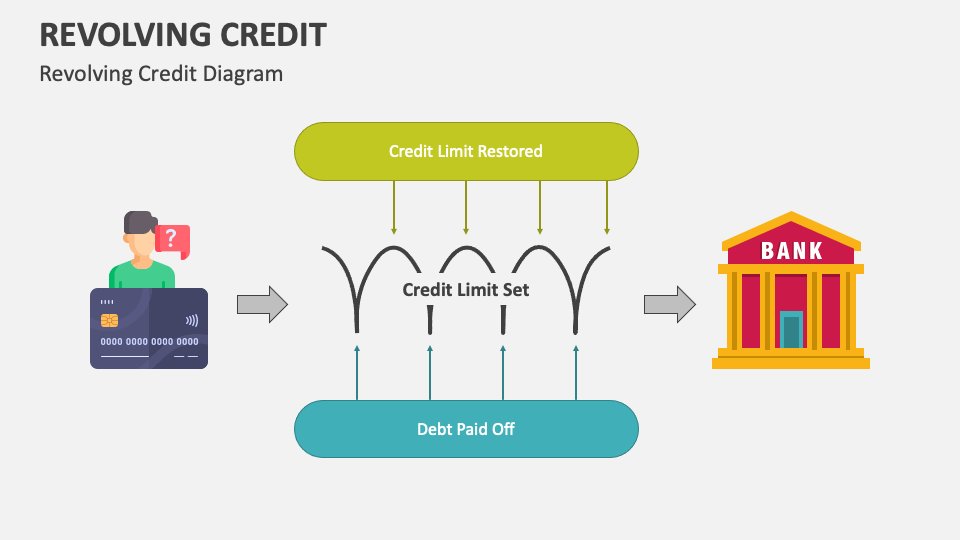

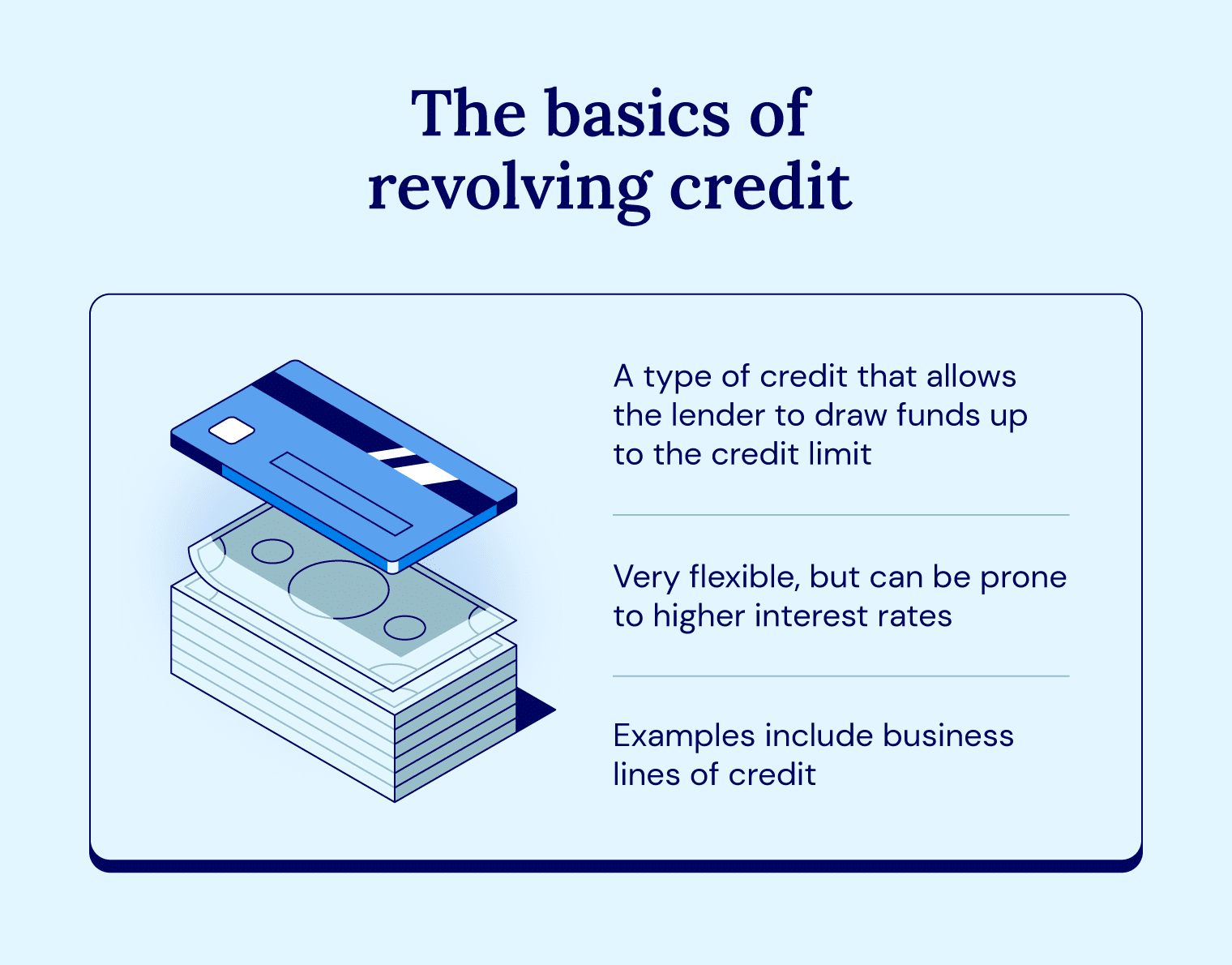

First off, what exactly is a revolving line of credit? Imagine it like this: it's a pre-approved loan amount that you can borrow from, repay, and borrow again. Think of it as your own personal financial playground! You only pay interest on what you borrow. Pretty neat, right?

Now, the tricky part: getting one with bad credit. Banks and credit unions (you know, those places that love good credit scores) might not exactly be throwing open their doors for you. But don't despair! There are still options. We just gotta be a little strategic. Think ninja-level strategic!

Must Read

Secured Revolving Lines of Credit

This is where things get interesting. A secured revolving line of credit means you’re putting up some collateral. What's collateral, you ask? It's basically something of value (like your car or maybe even a savings account – talk to your financial advisor!) that the lender can take if you don't repay the loan. A little scary sounding, maybe? But it significantly lowers the lender's risk, making them much more likely to say "yes" to someone with a less-than-perfect credit history.

Think of it as a confidence booster for the lender. You're saying, "Hey, I'm serious about repaying this. See? I'm putting my prized vintage comic book collection on the line!" (Okay, maybe not your comic books, but you get the idea!).

Credit Unions and Community Banks

Don't underestimate the power of your local credit union or community bank! They're often more willing to work with individuals than those massive, faceless corporate giants (no offense, Big Banks!). They might have programs specifically designed for people who are trying to rebuild their credit. Worth checking out, wouldn't you say?

Plus, the customer service is usually way better. You might actually talk to a real person who cares! Imagine that!

Online Lenders (Do Your Homework!)

The internet is bursting with online lenders offering all sorts of financial products. Some are great, some... well, let's just say they're less great. Proceed with caution! Research like your financial future depends on it (because, in a way, it kinda does!). Look for reputable lenders with transparent terms and conditions. Steer clear of those that seem too good to be true – because they probably are! Read the fine print! I can't stress that enough.

What to watch out for? Exorbitant interest rates (like, seriously, ouch!), hidden fees (sneaky!), and generally shady business practices. Trust your gut. If something feels off, walk away. There are plenty of other fish in the sea (or, in this case, plenty of other lenders online!).

Improving Your Credit Score: The Long Game

Getting a revolving line of credit with bad credit is a short-term solution. The real goal? Improve your credit score! This opens up a whole world of better interest rates, better loan terms, and fewer financial headaches. It's like leveling up in the game of life!

How do you do it? Pay your bills on time (duh!), keep your credit utilization low (that's the amount of credit you're using compared to your total available credit), and check your credit report regularly for errors. It's not a quick fix, but it's absolutely worth the effort. Think of it as planting a money tree – patience, watering, and sunshine (financial responsibility!) will eventually yield amazing results.

In conclusion, a revolving line of credit for bad credit is achievable, but it requires research, caution, and a healthy dose of realism. And remember, it's just a stepping stone to a brighter financial future. Good luck on your credit-building journey! You got this!