Personal Loan For High Debt To Income Ratio

Alright, let's talk about something we've all probably felt at some point: that sinking feeling when you realize your debt-to-income ratio (DTI) is looking less like a friendly puppy and more like a grumpy, debt-fueled dragon. Think of it like this: your income is the yummy burger you're holding, and your debt is that flock of hungry seagulls trying to snatch it away. The more seagulls (debt), the harder it is to enjoy your burger (income). We've all been there, right?

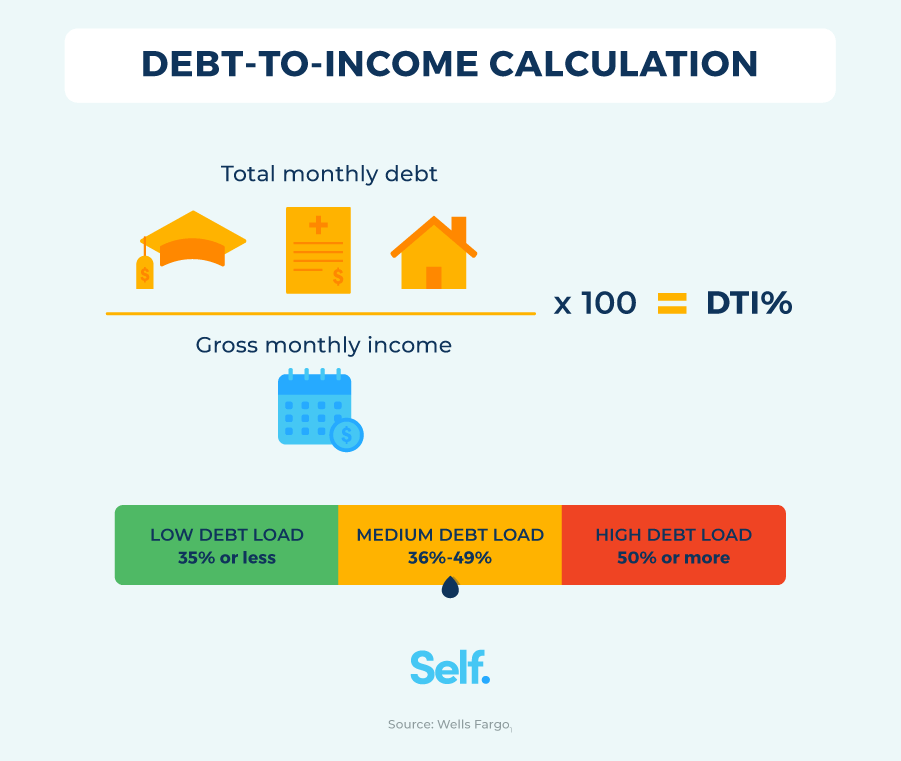

So, what is this DTI thing everyone's always whispering about? Simply put, it's the percentage of your monthly income that goes towards paying off debt. Rent, student loans, car payments, that lingering credit card balance from that "treat yourself" weekend – it all counts. Lenders use this number to gauge how risky it is to lend you money. A low DTI is like saying, "Hey, I'm responsible! I can totally handle more burger-defending!" A high DTI? Well, that's more like, "Please help me, the seagulls are winning!"

The Struggle is Real (and Relatable)

Getting a personal loan with a high DTI can feel like trying to parallel park a monster truck in a Smart Car space. It's not impossible, but it definitely requires some finesse. Lenders get nervous when they see a big chunk of your income already spoken for. They worry you might not be able to handle another payment. Think of them as concerned parents, and you're trying to convince them you can totally handle a new pet iguana even though you already have three cats, a dog, and a hamster.

Must Read

But don't despair! It's not game over. Just because your DTI is higher than you'd like doesn't mean you're doomed to a life of ramen noodles and bill collectors. There are options. You just might need to get a little creative.

So, What Can You Do? A Few Ideas to Consider:

1. Co-Signer Power! Think of a co-signer as your financial wingman (or wingwoman!). Someone with a solid credit history and lower DTI can vouch for you, telling the lender, "Hey, I trust this person. I'll help them defend their burger against the seagulls!" Of course, make absolutely sure you can make the payments, because if you don't, your co-signer will be on the hook. Don't ruin Thanksgiving dinner over a personal loan gone wrong!

2. Secured Loans: Collateral is Your Friend. A secured loan is backed by something of value, like your car or even savings account. It's like saying to the lender, "Here, take my prized baseball card collection as collateral. If I can't pay, you can have it!" (Okay, maybe not baseball cards, but you get the idea.) This reduces the lender's risk, making them more likely to approve your loan, even with that pesky high DTI. Be aware that you risk losing your collateral if you can’t pay back the loan.

3. Credit Union Magic. Credit unions are often more flexible than big banks. They're like the friendly neighborhood lenders who actually care about your story, not just your numbers. They might be willing to work with you on interest rates and loan terms, even with a higher DTI. Plus, they usually have cookies in the lobby!

4. Debt Consolidation: Taming the Seagulls. Consider consolidating your debt into a single, more manageable loan. This simplifies your payments and might even lower your interest rate, freeing up some of your income. It's like building a giant burger cage to keep those seagulls away!

5. Boost Your Income: More Burgers! This might seem obvious, but even a small increase in income can make a big difference in your DTI. A side hustle, a part-time job, selling that collection of Beanie Babies you've been hoarding – anything to bring in a little extra cash.

The Bottom Line

Getting a personal loan with a high DTI isn't a walk in the park, but it's also not an impossible mission. Be honest with yourself about your financial situation, explore your options, and be prepared to do a little extra work. With some careful planning and a bit of luck, you can get the loan you need without being completely devoured by debt (or seagulls). And remember, every little bit helps when it comes to improving that DTI! Good luck!