Personal Loan For Bad Credit With Cosigner

Okay, let's talk about something nobody really loves talking about: credit. Especially when it's, shall we say, less than stellar. We've all been there! Maybe you missed a payment or two (or ten, no judgment!), or perhaps you’re just starting out and haven’t built up a good credit history. Whatever the reason, that little credit score can feel like a giant gatekeeper, slamming the door on your dreams of, say, buying a car or finally tackling that mountain of medical bills.

Enter the Superhero: Your Cosigner!

But fear not, intrepid adventurer! There's a secret weapon in the battle for financial freedom: the cosigner. Think of them as your credit score's personal cheerleader, willing to vouch for you and help you get that personal loan you desperately need.

Basically, a cosigner is someone with good credit who agrees to be responsible for your loan if you, well, aren't. It's like saying, "Hey lender, I know my credit isn't the greatest, but my awesome friend/family member believes in me and they promise to pay if I don't!" It's a big responsibility for them, so choose wisely!

Must Read

Why a Cosigner is Your Bad Credit BFF

So, why is a cosigner such a game-changer when you have less-than-perfect credit? Let’s break it down in terms that even your grandma could understand (no offense, Grandma!).

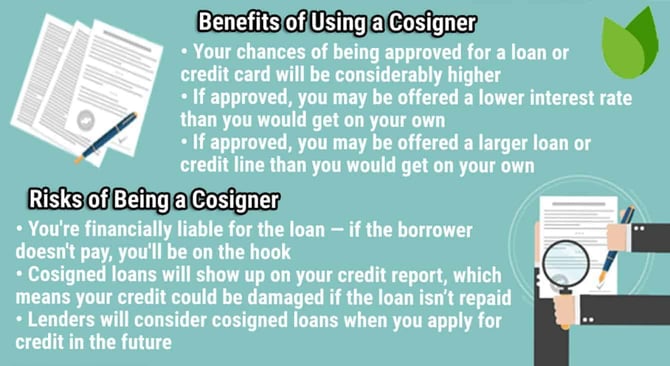

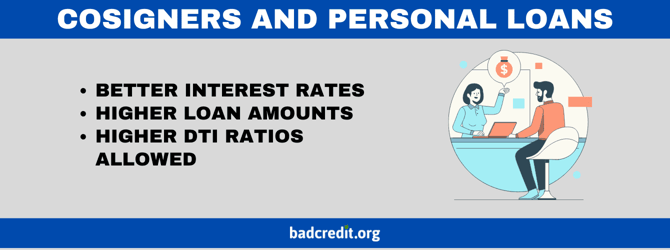

First, a cosigner significantly increases your chances of getting approved for a loan. Lenders are much more willing to take a risk on someone with shaky credit if they know there's a responsible adult (with a shining credit score) backing them up.

Second, you'll likely get a better interest rate. A higher credit score means less risk for the lender, which translates into lower interest rates for you. It's like getting a discount just for having a responsible friend!

Finally, getting a loan with a cosigner can actually help you rebuild your credit. By making on-time payments (and seriously, MAKE. ON-TIME. PAYMENTS!), you’re proving to the world that you are, in fact, a responsible borrower. Your credit score will thank you for it.

But Wait, There's a Catch (or Two)!

Now, before you start rounding up every vaguely responsible person you know, let's talk about the potential downsides. Because, like a free puppy, there are responsibilities involved.

The biggest catch? If you don't pay, your cosigner is on the hook. That's right, they're legally obligated to pay back the loan. This can seriously strain relationships, especially if it's Mom or Dad. Imagine Thanksgiving dinner after you've defaulted on a loan they cosigned. Awkward!

Also, your cosigner's credit score can be affected. Even if you're making payments on time, the loan will still show up on their credit report, increasing their debt-to-income ratio. This could make it harder for them to get approved for their own loans in the future.

So, Who Should You Ask?

Choosing a cosigner is like choosing a dance partner: you want someone reliable, trustworthy, and with good rhythm (or, in this case, a good credit score!).

Ideally, you'll want to ask a close friend or family member who trusts you and believes in your ability to repay the loan. They should also be financially stable and have a good understanding of the risks involved.

Here are a few potential candidates (and some you should probably avoid!):

- Good choices: Your parents (if you have a good relationship with them!), a close sibling, a trusted friend who's financially responsible.

- Maybe: Your super cool aunt who just won the lottery (they might be too generous for their own good!), your best friend who's always borrowing money (red flag!).

- Definitely not: Your flaky cousin who's always late on rent, your grandma who lives on a fixed income, anyone who makes you feel uncomfortable asking.

Preparing to Pop the Question (The Cosigning Question, That Is!)

Asking someone to be your cosigner is a big deal, so you need to approach the situation with respect and honesty. Don’t just spring it on them at a family barbecue!

First, explain why you need the loan and how you plan to repay it. Show them you've done your research and have a solid plan. Maybe even create a budget to demonstrate your commitment.

Next, be upfront about the risks involved. Make sure they understand that they'll be responsible for the loan if you default. No sugarcoating!

Finally, offer to provide them with regular updates on your loan payments. This will show them that you're taking the responsibility seriously and that you value their trust.

Finding the Right Lender

Not all lenders are created equal. Some specialize in working with borrowers who have bad credit and are willing to accept cosigners. Do your research and shop around for the best rates and terms. Don’t just jump at the first offer you see!

Look for lenders that are transparent about their fees and interest rates. Read the fine print carefully before signing anything. And if something seems too good to be true, it probably is.

Consider checking out online lenders, credit unions, and even some traditional banks. Each has its own pros and cons, so compare your options and choose the one that best fits your needs.

Cosigner Alternatives (If You're Feeling Shy)

Okay, let's say you're too nervous to ask someone to be your cosigner. Or maybe you just don't have anyone in your life who fits the bill. Don't despair! There are other options available.

Secured loans are one possibility. These loans are backed by collateral, such as a car or savings account. The collateral reduces the lender's risk, making them more willing to approve you even with bad credit.

Credit builder loans are another option. These loans are specifically designed to help you improve your credit score. The loan amount is typically small, and you make payments over a set period. Each on-time payment helps boost your credit.

The Takeaway: Don't Give Up!

Having bad credit can feel like you're stuck in a financial rut. But it doesn't have to be a life sentence! With a little bit of effort and the help of a trusty cosigner (or another alternative), you can get the loan you need and start rebuilding your credit.

Remember, financial responsibility is a marathon, not a sprint. Be patient, stay focused, and celebrate your successes along the way. You got this!

So, go forth and conquer your financial goals! And may your credit score forever be in your favor!