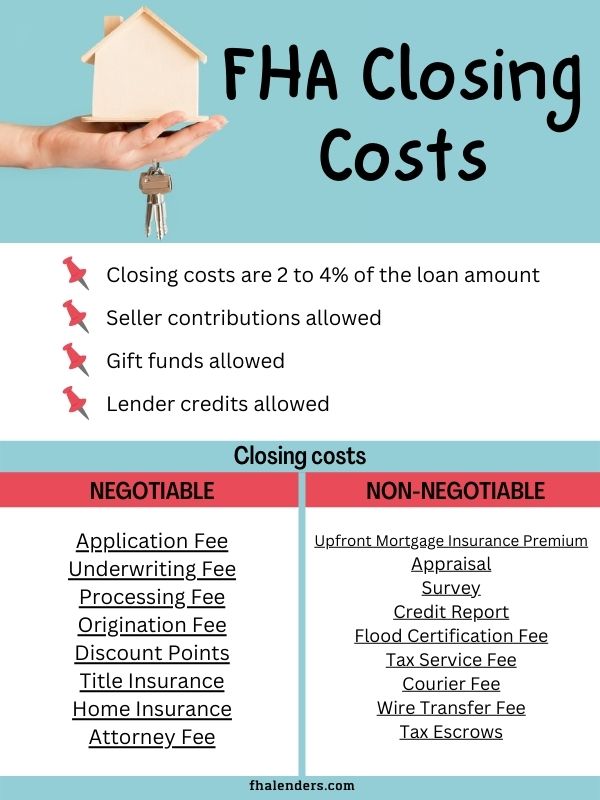

Mr Cooper Refinance Closing Costs

So, you're thinking about a refinance with Mr. Cooper, huh? Smart move! Maybe you want to snag a lower interest rate, consolidate some debt, or finally build that backyard tiki bar you've been dreaming of. Whatever the reason, refinancing can be a financial superpower. But before you go full superhero, let's talk about something that can sometimes feel like Kryptonite: closing costs.

Now, I know what you're thinking: "Ugh, closing costs. That sounds boring and expensive." And you're not entirely wrong. But think of it like this: it's the price you pay for unlocking all those sweet refinancing benefits. Plus, understanding them beforehand can help you avoid any surprises that could drain your "fun money" jar.

The Closing Cost Crew: A Rogues' Gallery (But Mostly Just Harmless Folks)

Imagine closing costs as a quirky group of characters, each with their own unique role in the refinance process. Let's meet a few:

Must Read

The Appraiser: This is the person who comes to your house and says, "Yep, this is a house! And it's worth approximately this much." Think of them as the Zillow estimate, but with actual eyeballs and a clipboard. Their fee covers their time and expertise in determining your home's market value.

Then there's the Title Company. They're like the librarians of property ownership, meticulously searching records to make sure everything is legit and that no one else is secretly claiming ownership of your prize-winning rose bushes. They charge fees for their title search, title insurance (protecting you and Mr. Cooper), and handling the closing itself.

Don't forget the Escrow Company! These folks are the neutral third party who make sure the money goes where it's supposed to go. They're like the Switzerland of the refinance world, ensuring a fair and transparent transaction.

You might also encounter fees for things like credit reports (because Mr. Cooper wants to make sure you're not secretly a financial supervillain) and recording fees (for officially registering the transaction with your local government).

The Art of Negotiation (or How to Haggle Like a Pro)

Here's a secret: some closing costs are negotiable! Think of it as a chance to unleash your inner bargain hunter. Ask Mr. Cooper if they offer any lender credits to offset some of these expenses. Sometimes, they'll be willing to cover certain fees to win your business.

Also, don't be afraid to shop around for things like title insurance. Different companies offer different rates, so doing a little comparison shopping can save you some serious coin. Just make sure you're comparing apples to apples (or, in this case, title policies to title policies).

The Big Picture: Is it Worth It?

Okay, so closing costs can be a bit of a pain. But before you throw in the towel and resign yourself to a life without that tiki bar, take a step back and look at the big picture. Will the long-term savings from a lower interest rate outweigh the upfront costs? Will consolidating your debt make your monthly budget less stressful?

Think of it this way: paying a few thousand dollars in closing costs now could save you tens of thousands of dollars over the life of your loan. Plus, that tiki bar is going to be epic. And that's priceless, right?

Ultimately, refinancing with Mr. Cooper is a big decision. Do your research, ask lots of questions, and don't be afraid to negotiate. With a little planning and a dash of humor, you can conquer those closing costs and unlock the financial freedom you deserve. Now go forth and refinance! And maybe send me an invitation to that tiki bar opening. I make a mean Mai Tai.