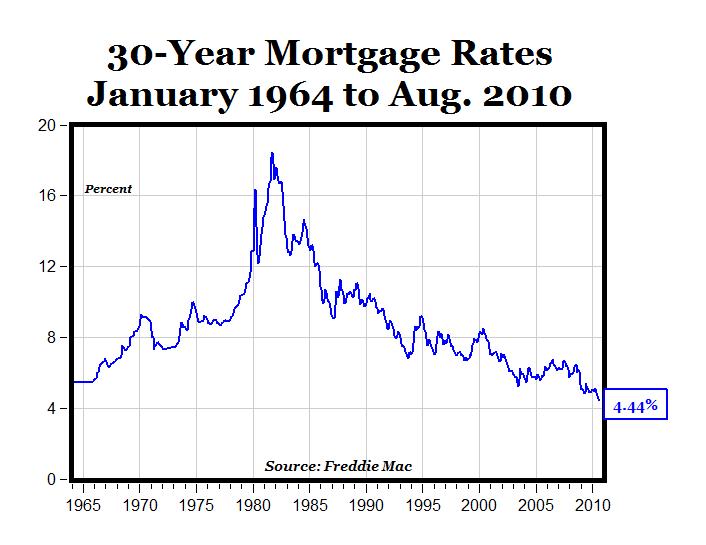

Mortgage Rates Lowest Ever

Okay, folks, let's talk mortgages. I know, I know. The very word can send shivers down your spine. But hear me out. We're living in a weird time. A time where mortgage rates are, shall we say, historically low. Lowest ever, they keep saying. Which brings me to my (possibly) unpopular opinion.

Should You Even Bother? (Hear Me Out!)

Seriously! Everyone's yelling, "Buy! Buy! Buy!" It's like Black Friday, but for houses. And everyone's acting like you're a fool if you don't refinance. But hold your horses. Has anyone stopped to consider the actual...effort involved? The paperwork? The phone calls? The explaining to Aunt Mildred what APR even means?

I'm not saying don't do it. I'm just saying, maybe take a deep breath first. Think about your sanity. Because honestly, sometimes the stress isn't worth saving a few bucks a month. Especially if those "few bucks" are immediately spent on celebratory takeout after you've finally finished signing all the forms.

Must Read

Look, I get it. The allure of a lower rate is strong. It's like finding a twenty-dollar bill in your old jeans. But before you start envisioning that new big-screen TV, let's remember the application process. It's basically like a financial colonoscopy. Everyone wants to know every detail of your life. Your income, your spending habits, your questionable Amazon purchases from 2017.

The Paperwork Apocalypse

And the paperwork! Oh, the paperwork! It's a Mount Everest of documents. W-2s, bank statements, tax returns… They demand proof of everything! Did you eat a sandwich last Tuesday? Show me the receipt! Did you breathe air? Provide a certified statement! It's exhausting.

And then there's the appraisal. This is where a stranger comes to your house and judges all your life choices. "Hmm, avocado green appliances. Interesting." They'll poke around, measure things, and make cryptic notes. Then they'll deliver their verdict: your house is worth… well, probably less than you thought. Thanks, appraisal person.

My Radical Suggestion: Maybe…Just Wait?

Okay, I'm going to say it. Maybe, just maybe, the best thing to do is… nothing. Just chill. Enjoy your current mortgage. Binge-watch Netflix. Eat some pizza. Let the housing market do its thing.

I know, I know. Sacrilege! But hear me out. Rates might go even lower (unlikely, but hey, stranger things have happened). Or they might go up. Who knows? The economy is about as predictable as a toddler with a marker. But at least you'll have saved yourself the headache of refinancing.

Of course, do your own research. Talk to a financial advisor. Don't base your entire financial future on this one (admittedly hilarious) article. But seriously, think about the stress factor. Think about your time. And think about whether saving a few dollars a month is really worth the hassle. Because sometimes, the peace of mind is priceless.

As Dave Ramsey might say (if he were feeling particularly mellow), "Sometimes, it's okay to just be content!"

Besides, what are you going to do with all that extra cash you save anyway? Probably buy more avocado toast, right? And then you'll need to prove you bought it to the mortgage company when you do decide to refinance. It's a vicious cycle, people. A vicious, paperwork-filled cycle. So, maybe… just maybe… don't jump on the lowest mortgage rates ever bandwagon. It's an unpopular opinion, I know. But I stand by it. Now, if you'll excuse me, I'm going to go enjoy my slightly-higher-than-average interest rate and my sanity.

And remember folks: this isn't financial advice. I'm just a person on the internet with an opinion. And probably too much time on my hands. But think about it! You've got this.