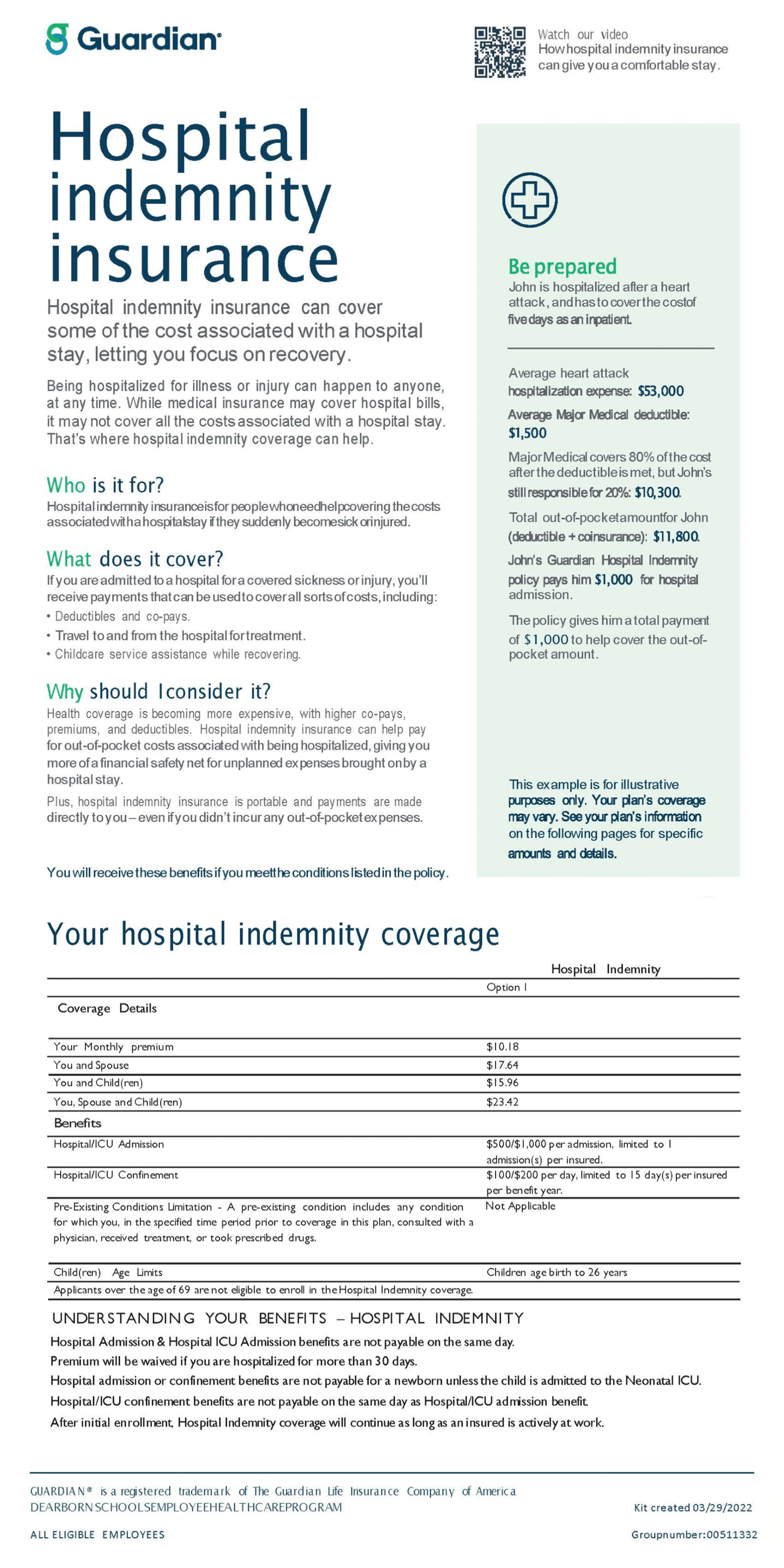

Is Hospital Indemnity Insurance Worth It

Okay, so picture this: My cousin, bless her heart, is the queen of DIY projects. She decided to build a chicken coop. From scratch. YouTube tutorials and all. Long story short, a rogue hammer, a startled hen, and a trip to the ER later, she's sporting a very impressive, very real cast. Thankfully, she's okay, but the medical bills? Yikes! That got me thinking: Do we really know what our insurance covers? And is there something more we should be considering? Enter: hospital indemnity insurance.

So, is hospital indemnity insurance worth it? That's the million-dollar question, isn't it? Well, grab a cup of coffee (or tea, I'm not judging), and let's dive in. It's not as scary as it sounds, I promise.

What Exactly Is Hospital Indemnity Insurance?

Think of it as a supplemental insurance policy. It pays you a fixed amount for each day (or event) you're in the hospital. This money is paid directly to you, not the hospital. So, you can use it for…well, anything! Co-pays, deductibles, childcare, lost wages, that emergency chicken coop repair fund… (too soon?).

Must Read

Basically, it's a safety net to help cover the out-of-pocket expenses that your regular health insurance might not fully cover. Think of it as that rainy-day fund for medical adventures. Hopefully, you won't need it, but it's nice to know it's there, right?

The Good Stuff: Why It Might Be Worth It

- Helps with Out-of-Pocket Costs: Let's face it, even with "good" insurance, deductibles and co-pays can sting. Hospital indemnity insurance can cushion the blow.

- Flexibility is Key: Remember, the money is yours to use as you see fit. Groceries, rent, paying someone to wrangle those chickens… it's all fair game.

- Peace of Mind: Knowing you have an extra layer of protection can ease your worries, especially if you have a high-deductible health plan. Less stress is always a win.

- Relatively Affordable: Compared to some other insurance types, hospital indemnity can be surprisingly affordable, especially if you're young and healthy. (But always shop around!).

See? It's not a bad idea. But (there's always a but, isn't there?), there are definitely things to consider.

The Not-So-Good Stuff: Things to Think About

- Not a Replacement for Health Insurance: This is crucial. Hospital indemnity insurance is supplemental. It doesn't cover your core medical expenses. You still need a good health insurance plan. (Don't even think about skipping that!).

- Fixed Benefit: The payout is fixed, regardless of your actual expenses. So, if you have a short hospital stay, you might not use the entire benefit.

- Waiting Periods: Many policies have waiting periods before benefits kick in. Read the fine print! You don't want to be caught off guard.

- Policy Variations: Coverage and costs can vary widely. Shop around and compare policies carefully. Don't just jump at the first offer you see.

Think of it this way: It's like buying that extended warranty on your new gadget. Sometimes it's a lifesaver, sometimes it's just extra clutter. It all depends on your individual situation.

So, Is It Worth It? Let's Get Personal

Here's the honest truth: there's no one-size-fits-all answer. Whether hospital indemnity insurance is worth it for you depends on several factors:

- Your Health Insurance Plan: Do you have a high-deductible plan? Are your co-pays high?

- Your Health History: Do you have any pre-existing conditions that might increase your risk of hospitalization?

- Your Financial Situation: Can you comfortably afford the premiums? Do you have other savings to cover unexpected medical expenses?

- Your Risk Tolerance: How comfortable are you with the potential financial risks of a hospital stay?

Honestly, the best advice is to talk to an insurance professional who can assess your specific needs and help you determine if hospital indemnity insurance is a good fit. Do your research! Read reviews! Get multiple quotes! Don't be afraid to ask questions.

Ultimately, the decision is yours. But hopefully, this has given you a little more clarity. Now, if you'll excuse me, I'm off to check on my cousin and her slightly traumatized chickens. And maybe invest in some extra bandages… just in case. Because, you know, life happens.

Disclaimer: I am not a financial advisor. This is just friendly advice based on my own (and my cousin's!) experiences. Always consult with a qualified professional before making any insurance decisions.