Is A Payday Loan Installment Or Revolving

Hey everyone! Ever been in that spot where your wallet's feeling a little...lighter than usual, and payday seems like a million miles away? We've all been there, right? Maybe you've even looked into a payday loan. But have you ever stopped to wonder, what actually is a payday loan? Specifically, is it an installment loan or a revolving credit account?

Payday Loans: The Quick Cash Crew

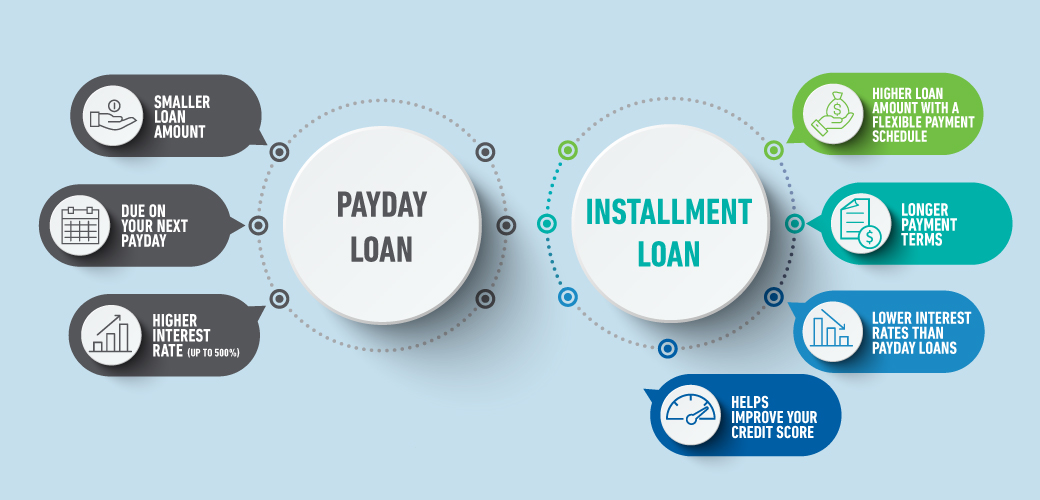

Think of payday loans as the flashy sprinters of the loan world. They’re designed for short-term emergencies – a sudden car repair, an unexpected bill. The idea is simple: you borrow a small amount of money, and you pay it back, plus interest and fees, on your next payday. Boom. Problem solved (hopefully!).

But here's the thing: are they like a mortgage, where you pay off a fixed amount each month? Or are they more like a credit card, where you can keep borrowing as you repay?

Must Read

Installment Loans: The Marathon Runners

Let's talk about installment loans first. These are the steady marathon runners. Think of your car loan or a student loan. You borrow a lump sum, and you pay it back in regular, fixed installments over a set period. Each payment includes a portion of the principal (the original amount you borrowed) and interest.

Once you've paid it all back, you're done! The loan is closed. You can't just borrow more money on that same loan without taking out a new one. Does that sound like a payday loan to you?

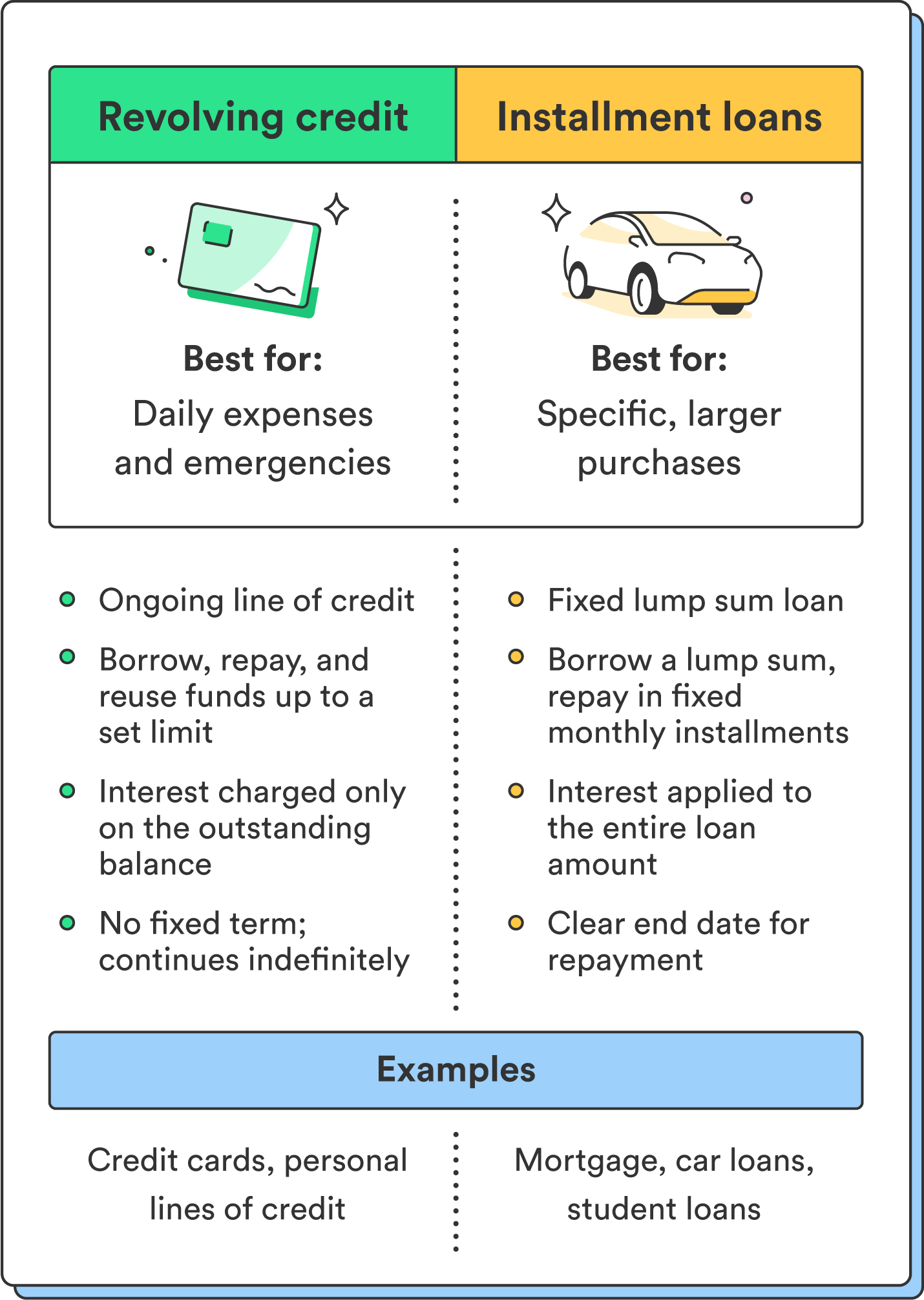

Revolving Credit: The Perpetual Motion Machines

Now, let's switch gears to revolving credit. Imagine a spinning top – always in motion. Credit cards and lines of credit are the prime examples. You have a credit limit, and you can borrow up to that limit. As you repay, your available credit replenishes, allowing you to borrow again. It's a continuous cycle of borrowing and repaying.

The cool (or potentially dangerous) thing about revolving credit is that you don't have to pay off the entire balance each month. You can make minimum payments, but you'll accrue interest on the unpaid amount. Think of it as a flexible friend… who charges interest.

So, Payday Loans: Installment or Revolving? The Verdict!

Okay, drumroll please! The answer is... installment! Payday loans are structured like installment loans, although with some seriously important differences. You borrow a specific amount, and you're expected to pay it back in one single payment on a specific date, usually your next payday.

:max_bytes(150000):strip_icc()/Differences-between-revolving-credit-and-installment-credit_sketch_final-ccac21e2a4a94aeb90443ea2b92ec759.png)

There's no revolving aspect to it. Once you repay the loan, it's closed. If you need to borrow again, you have to take out a new payday loan. It’s more like a single shot of espresso compared to the long, slow burn of a coffee pot.

Why Does It Matter?

You might be thinking, "So what? Who cares if it's installment or revolving?" Well, understanding the difference is super important for a few reasons:

- Financial Planning: Knowing how a loan works helps you budget and plan your finances effectively. You'll be less likely to get caught in a debt trap if you understand the repayment terms.

- Credit Score: While payday loans generally aren't reported to the major credit bureaus (which is why they often appeal to those with bad credit), repeated borrowing can still indirectly affect your credit. For example, if you default and the lender sends your debt to collections, that will impact your credit score.

- Interest Rates and Fees: Payday loans are known for their high interest rates and fees. Understanding that they're structured as a one-time installment helps you better grasp the true cost of borrowing. It's like comparing the price per ounce of a tiny bottle of fancy juice to a gallon of regular juice.

Payday Loan Pitfalls: A Word of Caution

While payday loans can be a quick fix in a pinch, they often come with extremely high interest rates and fees. Many people find themselves trapped in a cycle of debt, constantly borrowing to cover previous loans. It's like chasing your tail – you never quite catch it.

Before taking out a payday loan, consider all your options. Could you borrow from a friend or family member? Could you negotiate a payment plan with the creditor? Could you sell some belongings? Explore all your alternatives before turning to a payday loan. Your wallet (and your stress levels) will thank you.

The Takeaway: Know Your Loans!

The world of loans can seem confusing, but understanding the basics – like the difference between installment and revolving credit – can empower you to make smarter financial decisions. So, the next time you're facing a cash crunch, take a deep breath, do your research, and choose the borrowing option that best suits your needs and your budget. You've got this!