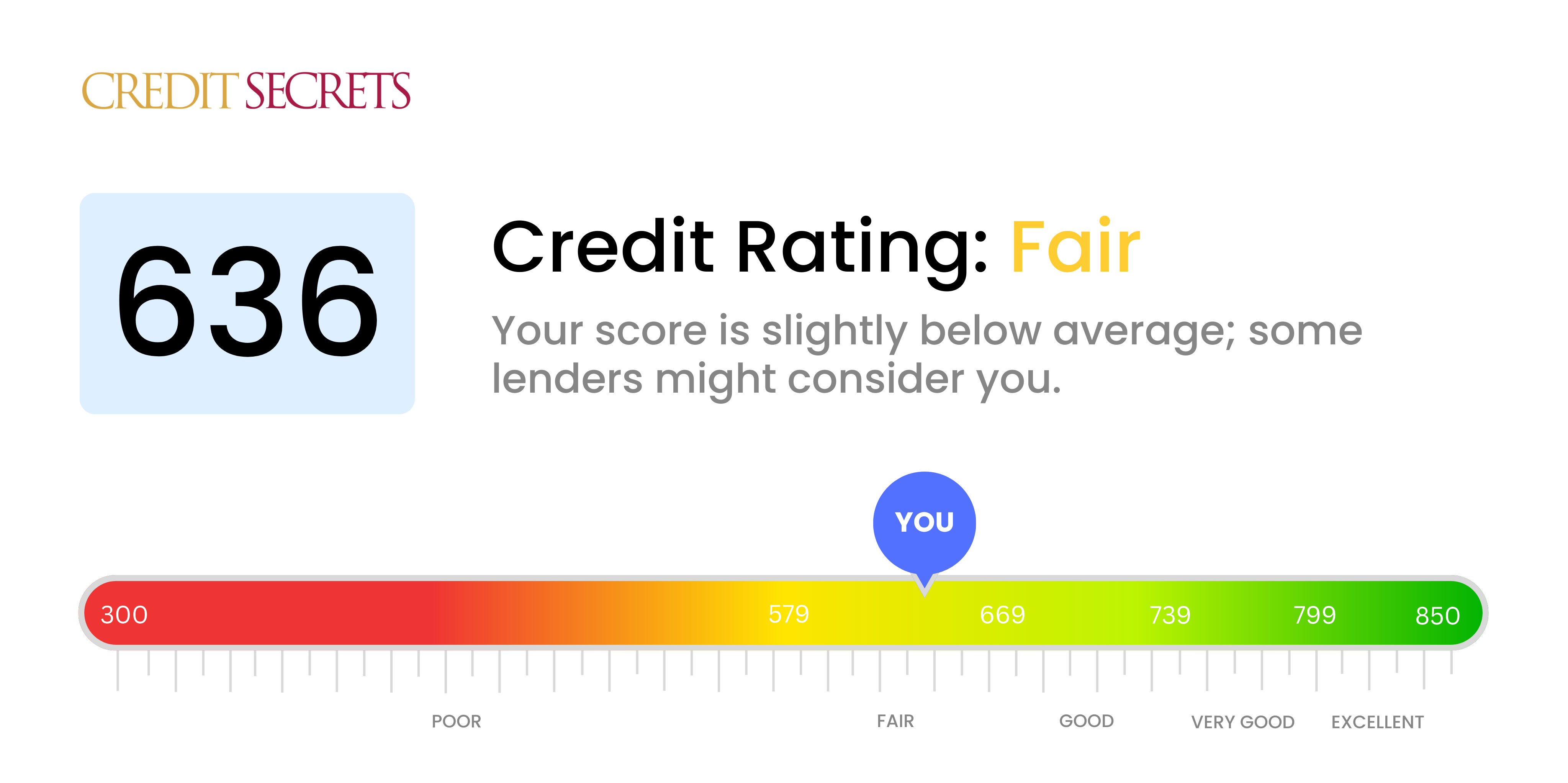

Is 636 A Good Credit Score To Buy A House

So, you're wondering if 636 is the magic number to unlock the door to homeownership? Let's dive in! It's a credit score that lands somewhere in the 'meh' zone. Not terrible, but definitely not amazing. Think of it as the beige of credit scores. Not exciting, but functional!

But hey, don't despair! Buying a house is a big deal. Credit scores are just one piece of the puzzle. Let's break down what 636 actually means, and whether you should start packing those moving boxes.

The Credit Score Lowdown

Credit scores are like your financial report card. They tell lenders how likely you are to pay back borrowed money. A higher score means you're a responsible borrower. Lower score? Well, let's just say lenders get a little more nervous.

Must Read

The most common credit scoring system is FICO. Scores range from 300 to 850. Where does 636 fit in? Generally, it falls into the "fair" category. Think of it as being on the cusp of something better!

Fun fact: Did you know that credit scores are based on algorithms? It's like a secret recipe for financial trustworthiness! Except, unlike grandma's cookies, the ingredients are all your financial habits.

636 and Homeownership: The Reality Check

Okay, the burning question: Can you actually buy a house with a 636 credit score? The short answer: Maybe. It's not a definite yes, but it's also not a definite no.

Here's the deal. Some lenders are more forgiving than others. They might offer mortgages to borrowers with lower credit scores, but there's a catch. Usually, higher interest rates. Think of it as paying a premium for the privilege. Important: Shop around for the best rates!

Quirky detail: Some lenders even offer mortgages specifically designed for first-time homebuyers with less-than-perfect credit! It's like a secret club for those who are just starting their homeownership journey.

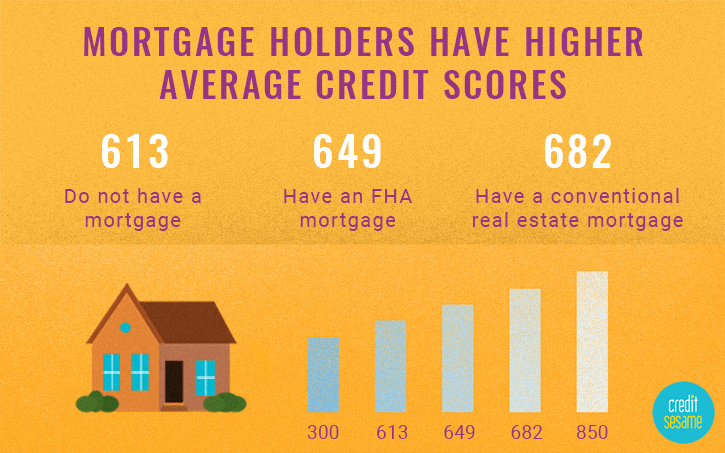

Another factor to consider: the type of loan. FHA loans, for example, are often more lenient with credit score requirements. They're backed by the Federal Housing Administration. Translation? The government helps reduce the risk for lenders, so they're willing to be a bit more flexible. The minimum credit score for an FHA loan can be as low as 500 in some cases. But be careful about the fine print.

Pro Tip: Your down payment also plays a role. A larger down payment can offset a lower credit score. It shows lenders you're serious and have some skin in the game. It’s like saying “Hey, I’m committed!”

Boosting Your Score: Operation Credit Improvement!

If you're not quite ready to dive into the housing market with a 636, don't fret! There are ways to improve your credit score. Think of it as leveling up your financial character.

First, check your credit report. Look for any errors or inaccuracies. Dispute anything that looks fishy. It's like being a credit detective, uncovering hidden secrets!

Second, pay your bills on time. This is huge. Late payments are like little gremlins attacking your credit score. Set reminders, automate payments - whatever it takes to avoid those gremlins!

Third, keep your credit utilization low. This means not maxing out your credit cards. Aim to use less than 30% of your available credit. Think of it as keeping your credit card balance under control.

Fourth, consider becoming an authorized user. If a friend or family member has a credit card with a good payment history, ask if you can be added as an authorized user. Their good habits can rub off on your credit score. But choose wisely! You want someone responsible, not a shopping spree enthusiast.

Fifth, be patient. Building credit takes time. It's not an overnight process. Don't get discouraged if you don't see results immediately. Keep at it, and you'll eventually reach your goal.

Funny thought: Improving your credit score is like training for a marathon. It takes dedication, discipline, and maybe a few blisters along the way. But the reward – homeownership – is totally worth it!

Beyond the Score: The Big Picture

Remember, your credit score is just one piece of the puzzle. Lenders will also consider your income, employment history, and debt-to-income ratio. They want to make sure you can afford the mortgage payments.

It's a good idea to get pre-approved for a mortgage before you start house hunting. This will give you a better idea of how much you can afford and what kind of interest rates you can expect.

Final thought: Buying a house is a big decision. Don't rush into it. Take your time, do your research, and make sure you're financially prepared. And don't be afraid to ask for help from a financial advisor or mortgage broker.

So, is 636 a ticket to homeownership? It depends! But with a little effort and planning, you can definitely increase your odds of getting that dream home. Now go forth and conquer the housing market!