Immediate Line Of Credit For Bad Credit

Let's face it, talking about credit, especially bad credit, isn't exactly a party. But what if I told you there's a way to potentially access funds when you need them most, even with a less-than-stellar credit history? That's where the idea of an "immediate line of credit for bad credit" comes in, and believe it or not, navigating this option can be surprisingly empowering. Think of it as understanding a potential financial tool that could help you out of a jam.

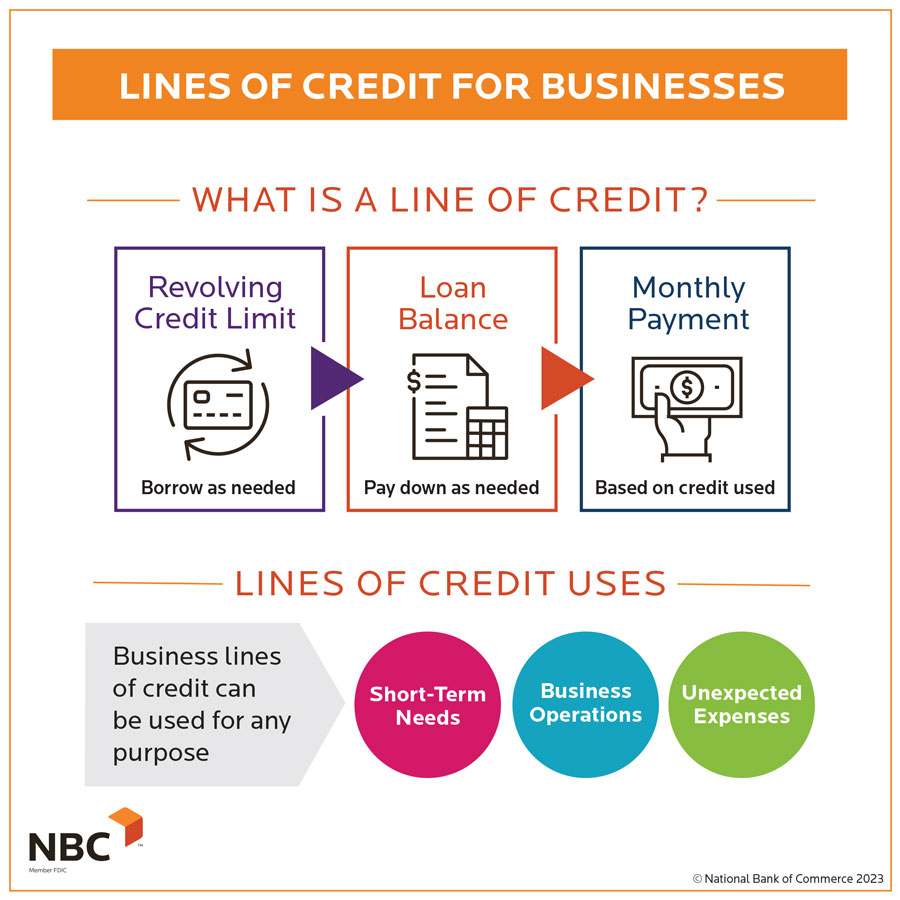

So, what exactly are we talking about? A line of credit is essentially a pre-approved loan that you can draw from as needed, up to a certain limit. Unlike a traditional loan, where you receive a lump sum and start repaying immediately, you only pay interest on the amount you actually use from the line of credit. This can be incredibly useful for unexpected expenses, like a car repair or a medical bill.

Now, the "immediate" part is where things get interesting. While a truly instant line of credit is rare (and often comes with significant drawbacks), some options offer a much faster approval process than traditional bank loans. This is often thanks to online lenders who utilize alternative data and algorithms to assess your creditworthiness, going beyond just your traditional credit score. They might consider your income, employment history, and even banking activity to get a fuller picture of your ability to repay.

Must Read

What are the benefits of exploring this option? Well, first and foremost, it's about access. When your credit score isn't shining, getting approved for any type of financing can feel like climbing Mount Everest. An immediate line of credit, even with slightly higher interest rates, can provide a lifeline when you're facing an urgent need. Secondly, responsible use of a line of credit can actually help you rebuild your credit. By making timely payments and keeping your credit utilization low (using only a small portion of the available credit), you can demonstrate to lenders that you're a reliable borrower.

However, it's crucial to approach this with your eyes wide open. Lines of credit for bad credit often come with higher interest rates and fees compared to those offered to borrowers with good credit. Be sure to carefully review the terms and conditions, paying close attention to the APR (Annual Percentage Rate), any origination fees, and potential late payment penalties. Ask yourself: Can I comfortably afford the monthly payments? What is the total cost of borrowing over time? Don't be afraid to shop around and compare offers from different lenders.

Also, be wary of lenders who promise guaranteed approval or require upfront fees before you even apply. These are often red flags for predatory lending practices. Stick to reputable lenders who are transparent about their terms and fees, and who have a clear track record of ethical lending.

In conclusion, an "immediate line of credit for bad credit" can be a valuable tool in certain situations. But it's essential to do your research, understand the costs involved, and borrow responsibly. Think of it as a potential stepping stone towards a brighter financial future, not a magic bullet. Use it wisely, and it can work for you!

:max_bytes(150000):strip_icc()/dotdash_Final_Line_of_Credit_LOC_May_2020-01-b6dd7853664d4c03bde6b16adc22f806.jpg)