If You Cosign A Loan Does It Affect Your Credit

Ever found yourself in that situation where a friend or family member needs a loan, and they ask you to cosign? It can feel like a kind gesture, a way to help someone you care about achieve their goals, whether it's buying a car, getting a student loan, or starting a business. But before you sign on that dotted line, it's really important to understand exactly what you're getting into. One of the biggest questions people have is: Does cosigning a loan affect my credit? Let's dive in and explore this topic in a straightforward way.

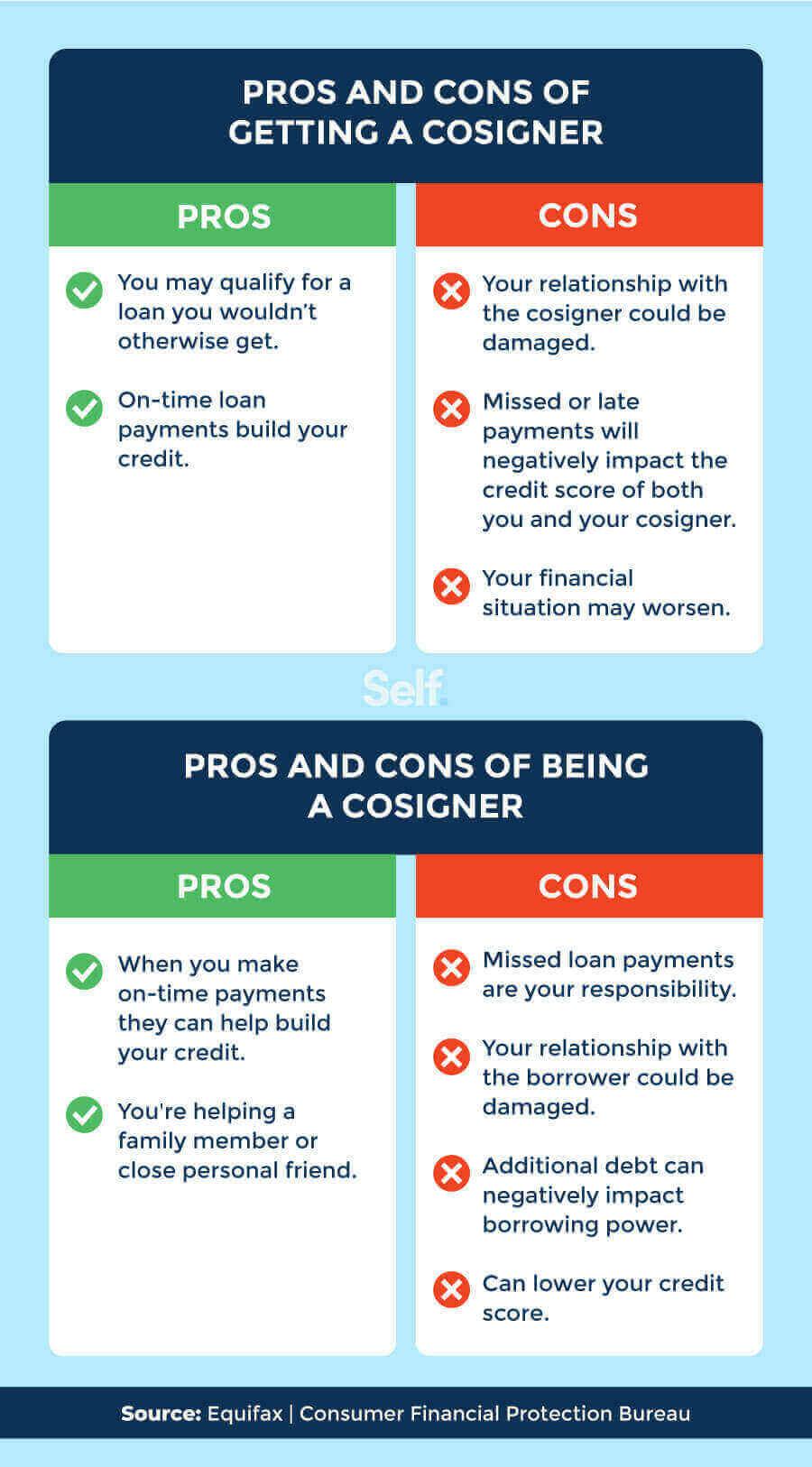

The core purpose of a cosigner is to provide assurance to the lender. When someone has a limited credit history, a lower credit score, or insufficient income, the lender might be hesitant to approve their loan application. A cosigner, with their stronger credit profile, essentially promises to repay the loan if the primary borrower defaults. Think of it as a safety net for the lender.

So, how does this impact your credit? The short answer is: yes, it can. When you cosign a loan, it shows up on your credit report just like any other loan you've taken out yourself. The loan appears as an obligation for which you are responsible. That means the loan amount will factor into your overall debt obligations, influencing your debt-to-income ratio. Lenders consider this when you apply for your own loans, like a mortgage or a car loan. A higher debt-to-income ratio can make it harder to get approved or result in less favorable interest rates.

Must Read

Beyond just showing up on your credit report, the performance of the primary borrower directly impacts your credit. If they make their payments on time, your credit score will generally be unaffected. However, if they are late on payments, or worse, default on the loan, that negative information will be reported to the credit bureaus and reflected on your credit report, causing your credit score to take a hit. This is perhaps the most important thing to understand. You're not just passively agreeing to help; you're actively putting your credit on the line.

Let's consider a few examples. Imagine you cosign a student loan for your younger sibling. If they consistently make their payments while in college and after graduation, your credit will likely be fine. But if they struggle to find a job and start missing payments, your credit score could suffer. Or, perhaps you cosign a car loan for a friend who then gets into financial trouble and can't keep up with the payments. Again, your credit score could be negatively impacted.

So, what can you do to protect yourself? First and foremost, carefully consider whether you're comfortable taking on the risk. Ask yourself if you truly trust the borrower to manage the loan responsibly. Secondly, discuss a clear repayment plan with the borrower and communicate openly about their financial situation. You can also request to be notified if the borrower misses a payment so you can address the issue promptly. Thirdly, check your credit report regularly to monitor the loan's status and catch any problems early. Services like Credit Karma or AnnualCreditReport.com offer free access to your credit report.

Cosigning a loan can be a generous act, but it's crucial to understand the potential impact on your own financial well-being. Do your research, weigh the risks and benefits, and only cosign if you're fully prepared to potentially repay the loan yourself. You can explore online resources from reputable financial institutions and credit bureaus for more in-depth information. The more informed you are, the better equipped you'll be to make a responsible decision.