How To Refund Overdraft Fees

Alright, settle in, folks! Let's talk about something near and dear to all our hearts: getting back money that banks unfairly snatched away! I'm talking, of course, about the dreaded overdraft fee. Those sneaky charges that appear seemingly out of nowhere, like a ninja accountant ambushing your bank account.

We've all been there, right? You check your balance, think you're in the clear, and BAM! Suddenly you're $35 poorer because you bought that latte that one time. It's like they're punishing you for participating in the capitalist system! (But I digress.)

But fear not, my financially-challenged friends! There is hope! You don't have to just accept these fees as an inevitable part of adulting. You can fight back! And that's exactly what we're gonna discuss today.

Must Read

Step 1: Know Thy Enemy (a.k.a. Understand Overdraft Fees)

Before we can launch our counter-offensive, we need to understand what we're up against. An overdraft fee, in its purest form, is a charge your bank hits you with when you try to spend more money than you actually have in your account. Think of it like trying to pay for a diamond necklace with lint and good intentions. The store (in this case, the bank) is not amused.

Banks offer "overdraft protection" which, ironically, often leads to even more fees. It’s like offering you a parachute made of lead. Thanks, but no thanks.

Fun Fact: Did you know that banks make BILLIONS of dollars each year from overdraft fees? That's enough to buy a small island...or, you know, pay off everyone's student loans. But hey, who needs societal improvement when you can have bigger bonuses for bank executives, right?

Step 2: Gather Your Ammunition (a.k.a. Review Your Bank Statement)

Okay, soldier, time to gear up. First, grab your bank statement. This is your intel. Look for those pesky overdraft fees. Note the date, the amount, and the transaction that triggered it. Was it a legitimate mistake? Or did the bank reorder your transactions to maximize the fees? (They do that sometimes, the sneaky devils! It's called "transaction reordering," and it's like organizing your spice rack alphabetically when your house is on fire.)

Pro Tip: Online banking makes this much easier. If you're still getting paper statements, it's time to embrace the 21st century! Think of all the trees you'll save! (And all the papercuts you'll avoid.)

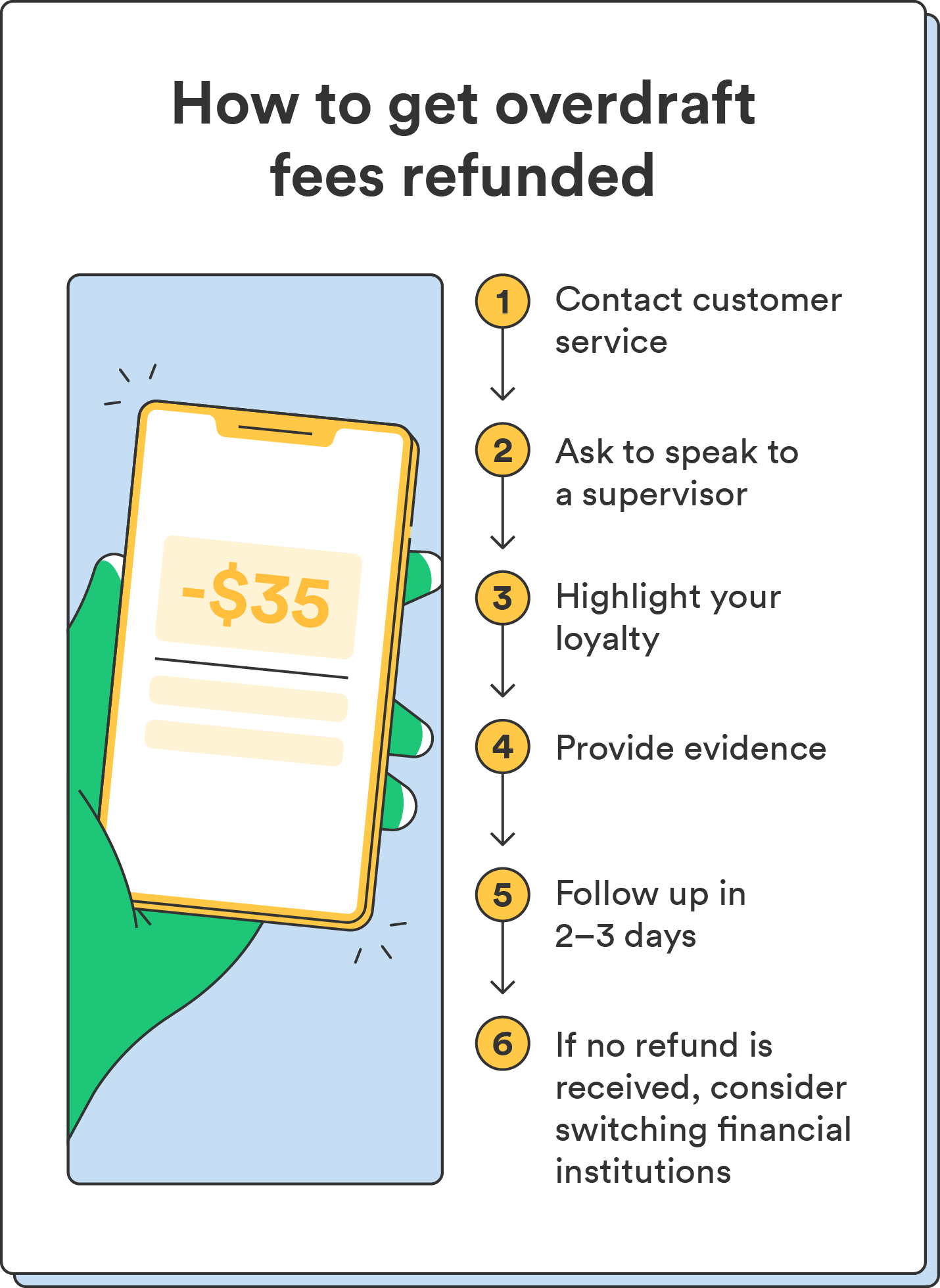

Step 3: The Art of Persuasion (a.k.a. Call Your Bank)

Alright, time to put on your most charming voice. Call your bank. Be polite, be firm, and be prepared to explain your case. Remember, honey catches more flies than vinegar… unless you’re trying to catch vinegar flies, in which case, never mind.

Here's a script you can adapt:

"Hi, I'm calling about an overdraft fee I incurred on [date] for [amount] due to [reason]. I've been a loyal customer for [number] years, and I've rarely had any issues. I was hoping you might be able to waive this fee as a one-time courtesy."

Important: Use phrases like "long-time customer," "good standing," and "one-time courtesy." Banks love hearing that stuff. It's like sweet music to their corporate ears.

What if they say no? Don't give up! Escalate the call to a supervisor. Sometimes, persistence pays off. Think of it as leveling up in a video game, but instead of getting a cool sword, you get your money back. Which, let's be honest, is way more useful.

Step 4: The Nuclear Option (a.k.a. Write a Letter)

If the phone call doesn't work, it's time to bring out the big guns: a formal written complaint. This shows the bank you're serious. Type up a polite but firm letter outlining the situation, just like you explained on the phone. Include all the relevant details (date, amount, reason, your account number, etc.). Mail it via certified mail with return receipt requested. This gives you proof that they received it, just in case they try to play dumb.

Extra points: CC the Consumer Financial Protection Bureau (CFPB). Banks hate the CFPB. It's like kryptonite to their profit-mongering schemes. Simply mentioning the CFPB can sometimes be enough to get them to budge.

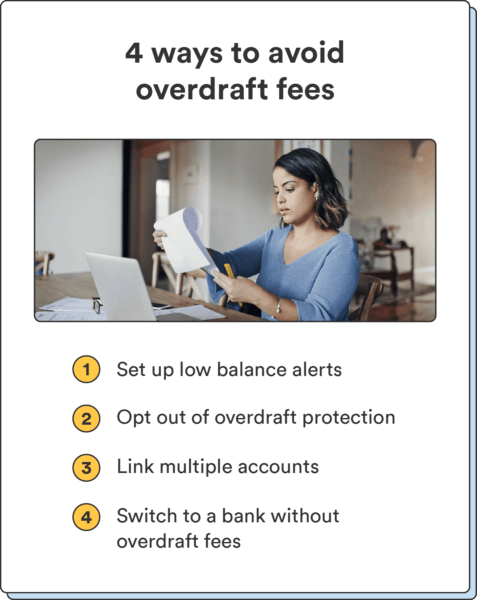

Step 5: Avoid Overdraft Fees in the First Place (a.k.a. Be Proactive)

Okay, let's be honest. The best way to avoid overdraft fees is to not overdraft in the first place. Mind-blowing, I know. But sometimes the simplest solutions are the most effective.

Here are a few tips:

- Set up low-balance alerts: Your bank probably offers this. Get notified when your balance dips below a certain threshold.

- Link your checking account to a savings account: This allows the bank to automatically transfer funds to cover overdrafts (usually for a small fee, but still cheaper than an overdraft fee).

- Use budgeting apps: Track your spending and avoid surprises.

- Say "no" to overdraft protection: Seriously, it's often more trouble than it's worth.

Final Thought: Getting hit with an overdraft fee is annoying, but it doesn't have to be a life sentence. With a little knowledge, persistence, and maybe a dash of luck, you can often get your money back. Now go forth and reclaim what is rightfully yours! And maybe treat yourself to that latte… you’ve earned it.