How Many Rollovers Can You Do In A Year

Alright, settle in, folks, because we're about to tackle a question that's plagued humankind for, well, at least five minutes: How many rollovers can you actually do in a year? Now, I know what you're thinking. You're picturing yourself, a majestic tumbleweed of human flesh, cartwheeling your way through 365 days. But hold your horses (or unicorns, if that's more your style), it's a bit more nuanced than that.

First, let's clarify what kind of rollover we're talking about. Are we discussing the delicious chocolate variety that cures all existential dread? Or perhaps the strategic kind related to your retirement accounts? Because, let's be honest, I'd love to write about the chocolate kind, but my editor is staring daggers at me through the screen right now. So, it's the retirement account kind. Bummer, I know.

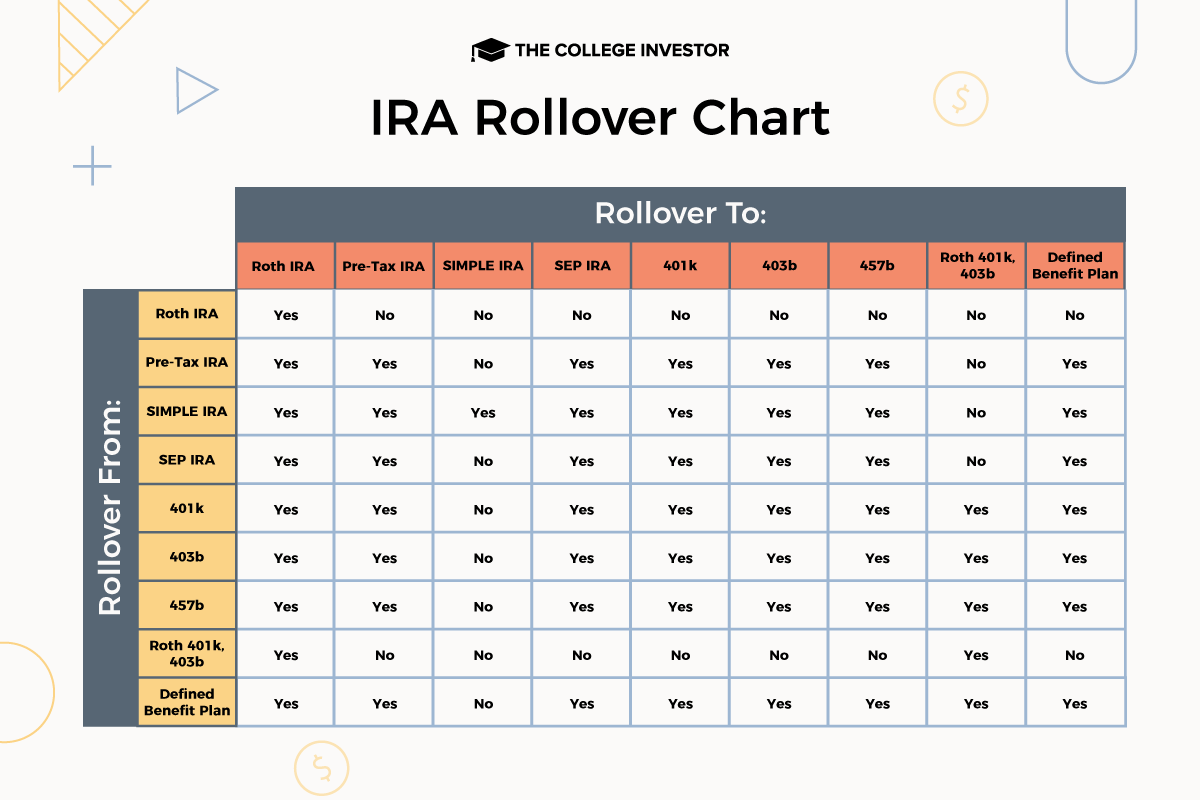

The One-Rollover-Per-Year Rule (For IRAs, Anyway)

Okay, so here's the lowdown on your IRA. The IRS has this thing called the "one-rollover-per-year rule." Sounds intimidating, right? Basically, you can only do one rollover from one IRA to another IRA in any 365-day period. Think of it like a cosmic rollover permit. Use it wisely!

Must Read

Now, before you start panicking, this rule applies to each individual IRA you own. So, if you've got five IRAs scattered around like forgotten socks, you could theoretically roll over each of them once within a year. But, honestly, if you have that many IRAs, maybe consolidation is something to look at. Just a suggestion from your friendly neighborhood finance guru (that's me!).

Important note: This "one-rollover-per-year" rule applies to each IRA you own. Let's say you have a Traditional IRA and a Roth IRA. You can do one rollover in each, in the same year, as it is in two separate IRA accounts.

Imagine trying to explain this at a party. “Oh, yeah, I just maxed out my IRA rollovers for the year.” People will either think you're a genius or incredibly boring. Or both!

Direct vs. Indirect Rollovers: A Fork in the Road

Alright, things are about to get spicy (well, maybe lukewarm). There are two main types of rollovers: direct and indirect. Direct rollovers are like a VIP transfer. The money goes directly from your old account to your new account, without you ever touching it. It's smooth, seamless, and usually involves a friendly phone call or online form.

Indirect rollovers, on the other hand, are a bit more… dramatic. You receive a check from your old retirement account. Then, you have 60 days to deposit that check into a new retirement account. If you miss the deadline, the IRS considers it a distribution, and you'll owe taxes (and possibly penalties!). Missing that deadline is a financial disaster, the equivalent of accidentally microwaving your car keys.

Also, in an indirect rollover, your old account provider must withhold 20% for federal income tax. It means the amount you have available for your new account is reduced by this amount. You must make up this shortfall from other funds when you deposit it to your new retirement account. When you file your taxes, you will get this amount returned, as long as you completed the rollover properly.

The "one-rollover-per-year" rule only applies to indirect rollovers. So, if you're doing a direct rollover, you don't have to worry about that particular limitation. Hallelujah!

Now, some people love the thrill of an indirect rollover. Maybe they enjoy living on the edge, tempting fate with that 60-day deadline. But if you're anything like me, you prefer the path of least resistance (and minimal chance of messing things up). Direct rollovers are your friend.

What About 401(k)s? A Different Ballgame

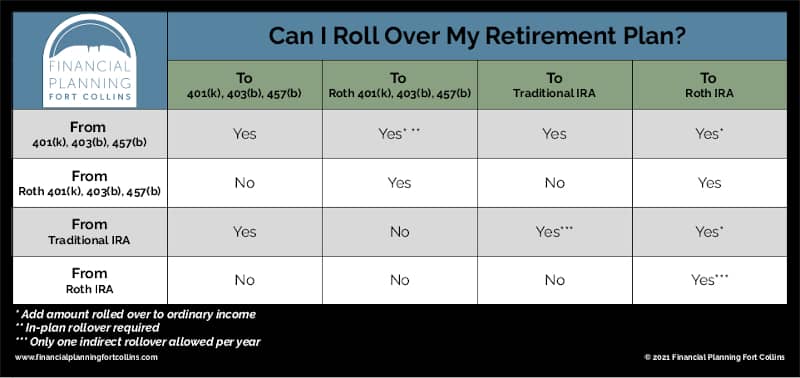

Hold on to your hats because 401(k)s operate under a slightly different set of rules. The "one-rollover-per-year" rule doesn't apply to rollovers from a 401(k) to an IRA, or vice versa. You can generally roll over your 401(k) money to an IRA whenever you want, as long as your plan allows it. This is a crucial distinction!

Also, you can rollover your traditional 401(k) to a Roth 401(k), as long as your plan allows this in-plan conversion.

However, there might be restrictions on when you can take money out of your 401(k). Many plans require you to be separated from service (i.e., leave your job) before you can roll over your funds. Always check with your plan administrator to understand the specific rules.

The Bottom Line (and a Funny Anecdote)

So, to recap: You get one indirect IRA rollover per year, per IRA account. Direct rollovers are generally unlimited. 401(k) rules are a bit different, so check your plan documents. Got it? Great! Now you can impress your friends at trivia night with your newfound rollover knowledge.

Speaking of trivia night, I once tried to explain this whole rollover situation to my friend Dave. He ended up accidentally ordering a plate of chicken wings and a side of onion rings. I’m not saying my explanation was confusing, but apparently, it was delicious. So, if all else fails, just remember: rollovers might be complicated, but chicken wings are always a good idea.

Disclaimer: I'm not a financial advisor, and this is not financial advice. Consult with a qualified professional before making any important decisions about your retirement accounts. And maybe order some chicken wings while you're at it.