Does Sgli Continue After Retirement

So, you're thinking about hanging up your boots, kicking back, and finally mastering the art of competitive napping? Awesome! But a little voice in the back of your head is whispering, "What about my SGLI?" Let's tackle that burning question with the enthusiasm of a puppy chasing a squeaky toy!

The short and sweet answer? Generally, your standard Servicemembers' Group Life Insurance (SGLI) doesn't automatically continue at the same premium and coverage level once you officially retire or separate from the military. Think of it like your military ID – it's fantastic while you're serving, but it’s time to say goodbye when your service ends.

But don't start hyperventilating into a paper bag just yet! This isn't the end of the life insurance road. It's more like a detour onto a slightly different, but potentially even more scenic, route.

Must Read

The VGLI Option: Your Post-Service Superhero

Enter VGLI, or Veterans' Group Life Insurance! Consider it SGLI's older, wiser, and slightly more expensive cousin. VGLI is designed to give you continued life insurance coverage after you leave the military.

Think of it like this: SGLI is your initial training wheels, and VGLI is your cool, customized road bike. You’ve proven you can handle the basics, now it's time to upgrade to something that fits your needs as a civilian.

How VGLI Works (Without the Headache)

The good news is, you're typically eligible for VGLI if you had SGLI coverage while on active duty. It’s almost like a reward for your service, a thank you gift wrapped in insurance jargon!

The best part? You don't have to jump through a million hoops to apply. The application process is usually pretty straightforward, though always read the fine print, of course. No one wants to accidentally sign up for a lifetime supply of kale chips when they just wanted life insurance.

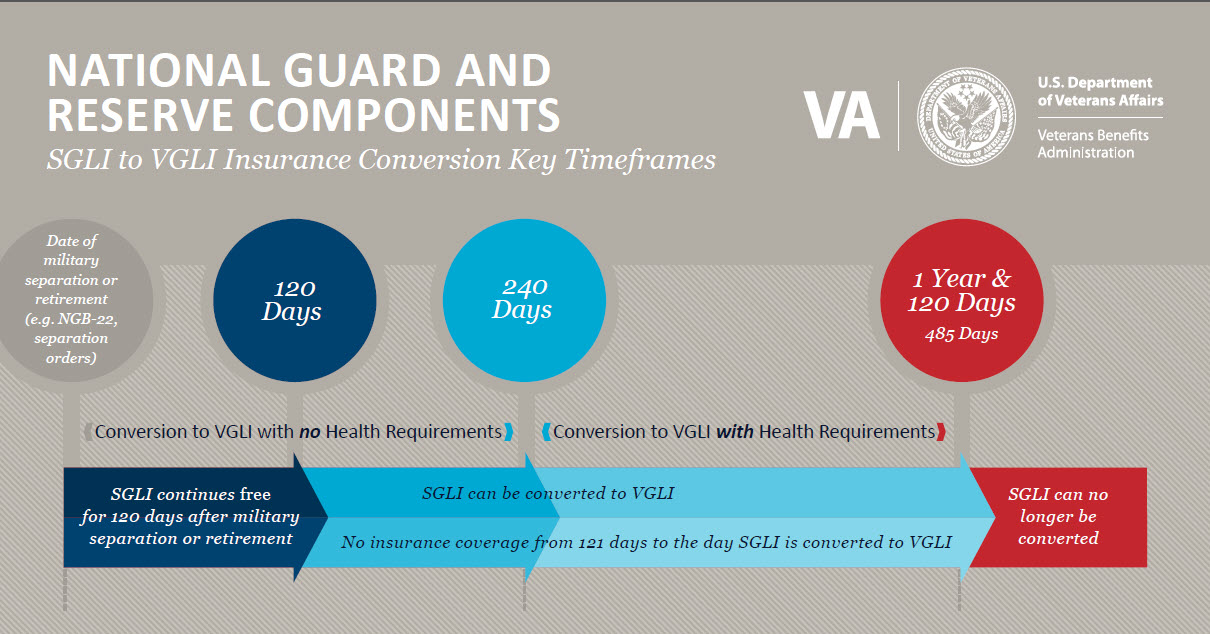

You generally have a window of time after leaving the service to apply for VGLI. Missing this window is like missing the last train home – a bummer you definitely want to avoid. Make sure you know the deadline!

VGLI: What's the Catch? (Spoiler: It's Not That Scary)

Okay, let's be real. There's always a "catch," right? Well, with VGLI, the biggest difference you'll notice is the premium. It generally costs more than SGLI. Think of it as the price of freedom... from worrying about life insurance coverage!

This is because SGLI rates are subsidized by the government, while VGLI is based on your age. As you get older, the risk of, well, gestures vaguely... things happening... increases, so the premiums go up accordingly.

But don't let that scare you off! VGLI is still often a very competitive option, especially if you're relatively young and healthy. Shop around and compare rates, but VGLI is a fantastic starting point.

Converting to a Commercial Policy: Spreading Your Wings

Another option to explore is converting your SGLI to a commercial life insurance policy. This basically means you'd switch from a government-backed plan to one offered by a private insurance company.

Think of it like leaving the nest. SGLI and VGLI are like your parents' cozy home, providing a safe and familiar environment. Converting to a commercial policy is like buying your own place – more responsibility, but also more freedom!

The advantage of converting is that you can often get a policy that's tailored specifically to your needs and budget. Want extra coverage for skydiving? Done! Need a policy that covers your prize-winning poodle? Maybe! (Okay, probably not, but you get the idea.)

Finding the Right Commercial Policy: A Treasure Hunt

Finding the right commercial policy can feel like searching for buried treasure. There are so many companies out there, all promising the best rates and coverage. It is crucial to do a research and get quotes from multiple insurers.

Don't be afraid to ask questions! A good insurance agent will be happy to explain the different policy options and help you find one that fits your situation like a glove. Think of them as your friendly insurance sherpa, guiding you through the treacherous terrain of deductibles and riders.

Read the fine print! Seriously. Twice. Make sure you understand exactly what's covered and what's not. You don't want to discover that your policy doesn't cover incidents involving rogue squirrels just when you need it most.

Making the Decision: It's All About You!

So, does SGLI continue after retirement? Not in its original form. But you have options! VGLI and converting to a commercial policy are both excellent ways to maintain life insurance coverage after leaving the military.

The best choice for you depends on your individual needs, budget, and preferences. Consider factors like your age, health, financial situation, and how much coverage you need.

Think of it like ordering pizza. Do you want the classic pepperoni (VGLI – reliable and familiar), or do you want to create your own gourmet masterpiece with artichoke hearts and goat cheese (a commercial policy – customized and potentially more expensive)? The choice is yours!

Don't be afraid to seek professional advice. A financial advisor or insurance agent can help you weigh your options and make an informed decision. They can also help you navigate the paperwork and avoid any potential pitfalls.

Ultimately, the goal is to ensure that you have the peace of mind knowing that your loved ones will be taken care of, no matter what. So, take a deep breath, do your research, and choose the option that's right for you.

Retirement is an exciting new chapter in your life. Don't let worrying about life insurance cast a shadow over your well-deserved relaxation! Go forth, conquer that retirement to-do list, and enjoy the fruits of your labor. You've earned it!

Remember, knowledge is power! Now go forth and confidently navigate the world of post-military life insurance. You got this!