Do You Need A Credit Score To Buy A House

Have you ever wondered what it takes to buy a house? Is a credit score a necessity, or can you still achieve your dream of homeownership without one? Let's dive into the world of credit scores and explore their role in the home-buying process. Understanding how credit scores work and their importance can be empowering and even fun to learn, especially if you're planning to purchase a house in the near future.

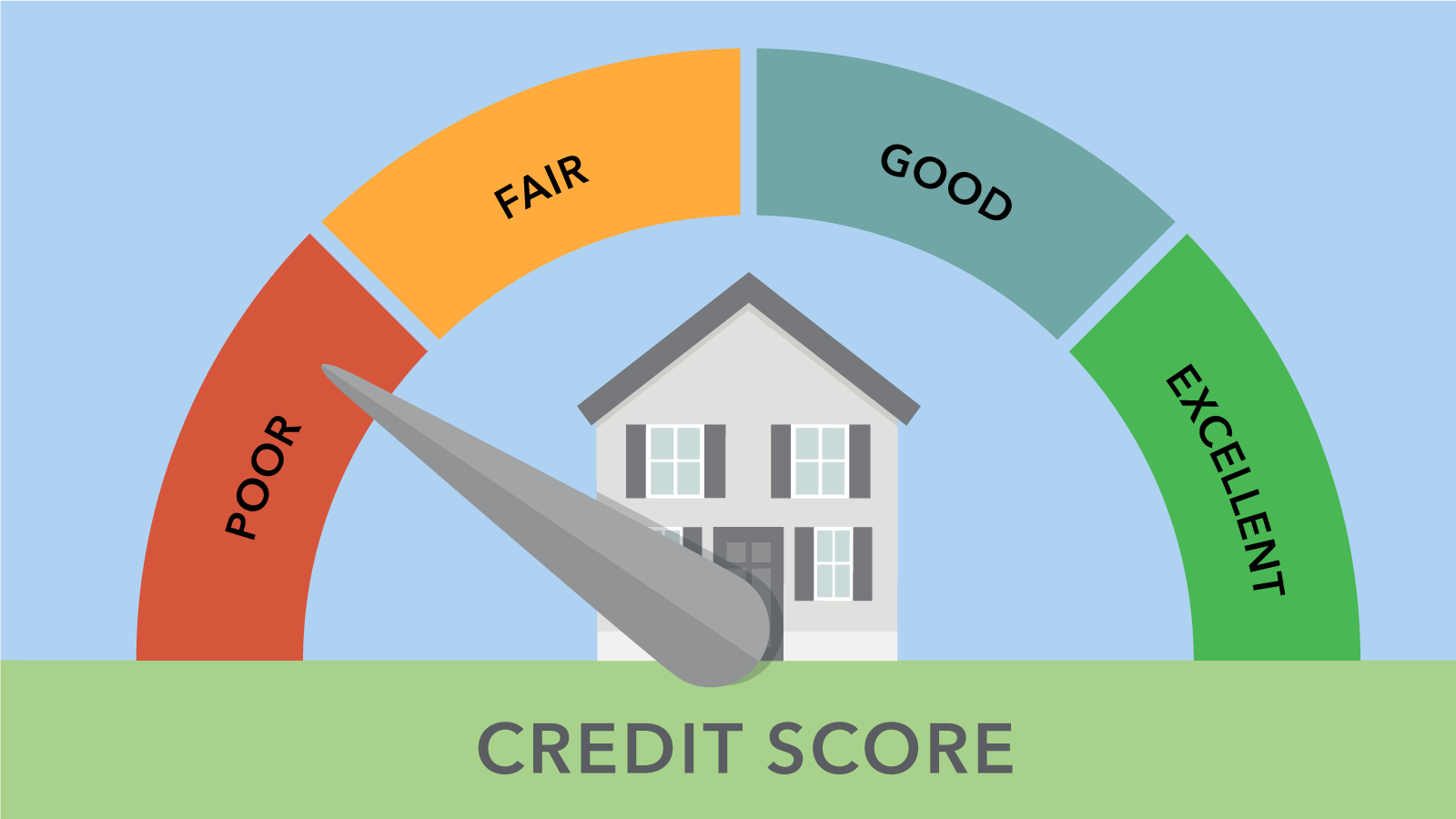

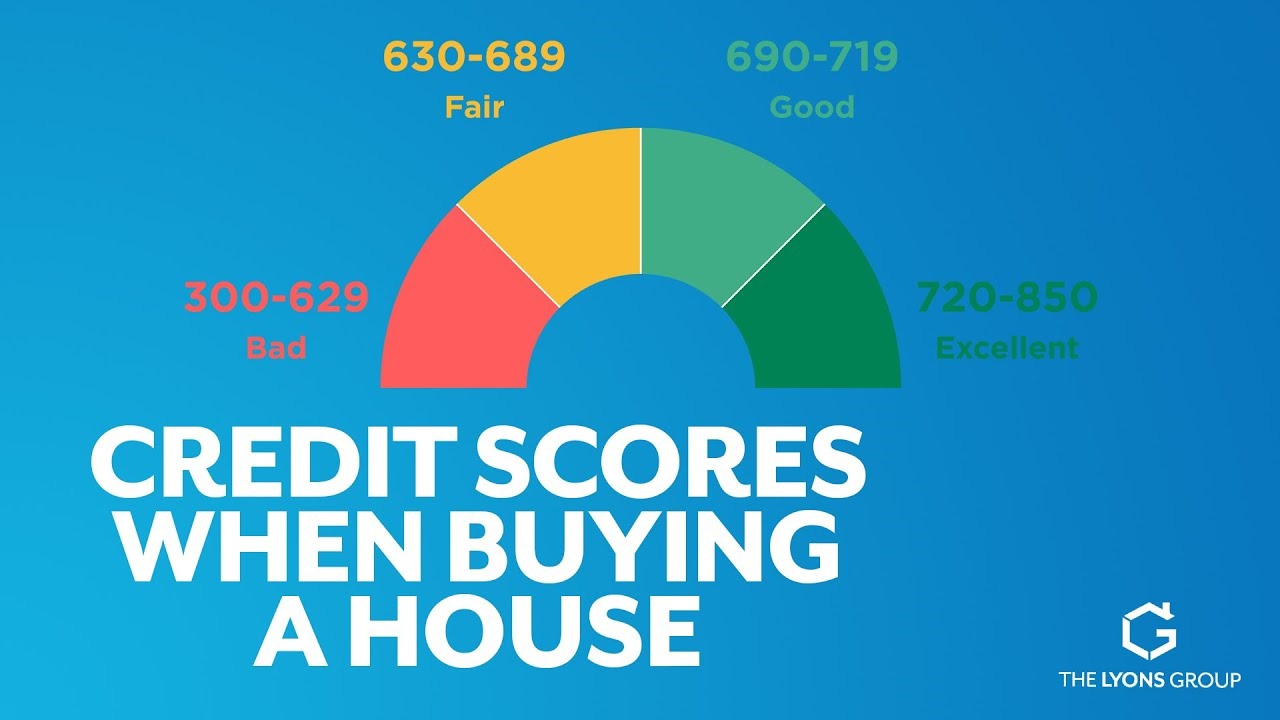

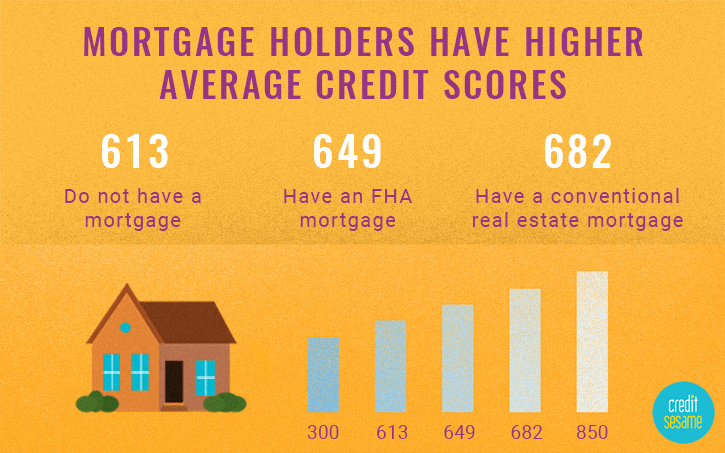

The purpose of a credit score is to provide lenders with a way to evaluate your creditworthiness. It's a three-digit number that represents your history of borrowing and repaying debts, such as credit cards, loans, and mortgages. A good credit score can offer numerous benefits, including lower interest rates, better loan terms, and even lower deposits. For instance, a high credit score can help you qualify for a lower interest rate on your mortgage, which can save you thousands of dollars over the life of the loan.

In everyday life, credit scores are used by lenders to determine the risk of lending to you. For example, when you apply for a credit card, a personal loan, or a mortgage, the lender will typically check your credit score to assess your creditworthiness. A good credit score can also be beneficial when renting an apartment or buying a car. In education, understanding credit scores can help students make informed decisions about their financial aid and student loans.

Must Read

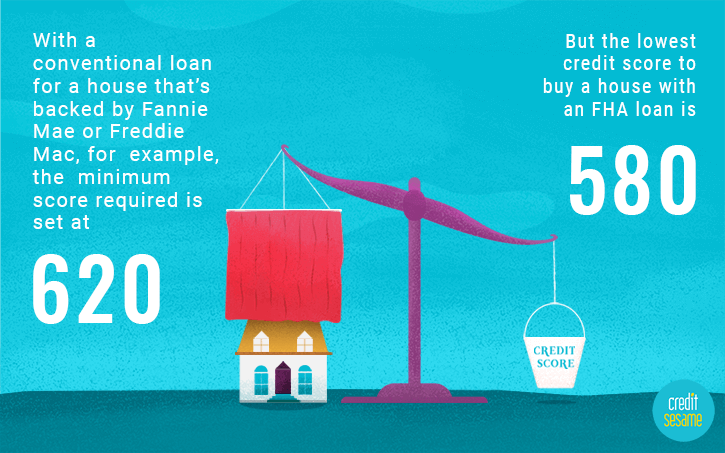

So, do you need a credit score to buy a house? The answer is, it depends. While it's possible to buy a house without a credit score, it can be more challenging and expensive. Some lenders offer alternative credit scoring models or non-traditional credit scoring methods, which can consider other factors such as rent payments or utility bills. However, these options may come with higher interest rates or stricter terms.

If you're planning to buy a house, it's essential to understand your credit score and how it can impact your mortgage application. Here are some practical tips to get you started: check your credit report regularly to ensure it's accurate, make on-time payments to demonstrate responsible credit behavior, and avoid applying for too much credit at once. You can also consider working with a credit counselor or a financial advisor to help you improve your credit score and achieve your goal of homeownership.

Exploring the world of credit scores can be rewarding and informative. By understanding how credit scores work and their importance in the home-buying process, you can make informed decisions about your financial future. So, take the first step today and start learning about credit scores. With a little knowledge and planning, you can achieve your dream of homeownership and enjoy the many benefits that come with it.