Do I Need Building Insurance On A Leasehold Flat

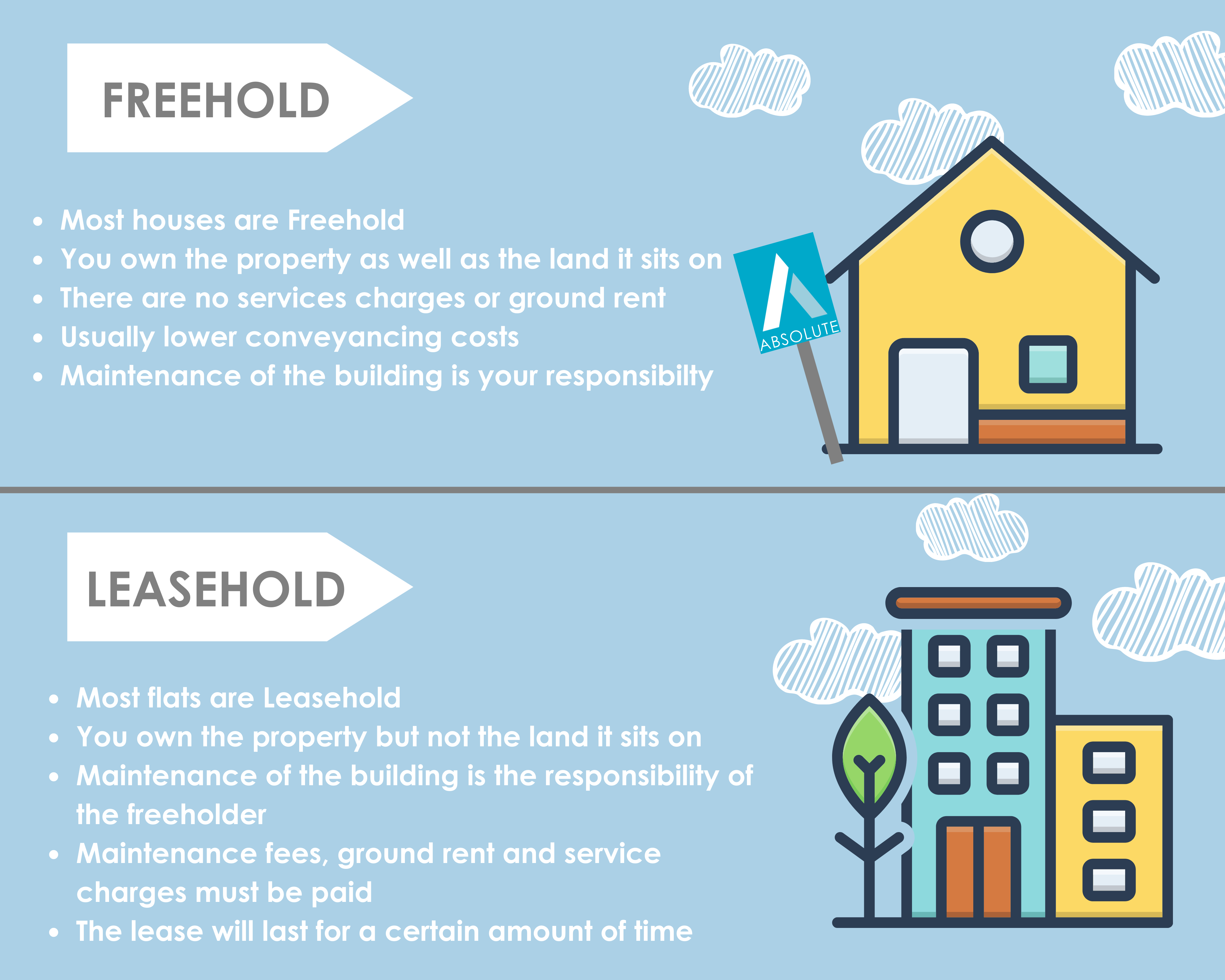

When it comes to leasehold flats, one of the most critical considerations is insurance. As a leaseholder, you may be wondering if you need building insurance on your leasehold flat. The answer lies in understanding the intricacies of leasehold agreements and the legal requirements surrounding insurance. In essence, building insurance is typically the responsibility of the freeholder or the landlord, as they are the ones who own the building. However, as a leaseholder, you still have a vested interest in ensuring that the building is properly insured, as any damage or losses could affect your property and your livelihood.

The science behind building insurance lies in risk management and probability analysis. Insurance companies use complex algorithms and statistical models to determine the likelihood of certain events occurring, such as natural disasters or accidents, and then calculate the premiums accordingly. As a leaseholder, it's essential to understand these concepts and how they apply to your situation. By doing so, you can make informed decisions about your insurance needs and ensure that you're adequately protected.

In terms of biology, the concept of homeostasis comes into play when considering building insurance. Homeostasis refers to the ability of a system to maintain a stable internal environment despite changes in the external environment. In the context of building insurance, homeostasis can be applied to the balance between the premiums paid and the risk coverage provided. By finding the optimal balance between these two factors, you can maintain a stable financial environment and ensure that you're protected against potential losses.

Must Read

Understanding Leasehold Agreements and Insurance Requirements

A leasehold agreement is a contract between the freeholder and the leaseholder that outlines the terms and conditions of the lease. These agreements can be complex and often include clauses related to insurance. It's essential to carefully review your leasehold agreement to understand your insurance obligations and any requirements imposed by the freeholder. In some cases, the freeholder may require you to take out a specific type of insurance or to pay a contribution towards the building's insurance premiums.

From a chemical perspective, the concept of catalysts can be applied to the relationship between leasehold agreements and insurance. A catalyst is a substance that speeds up a chemical reaction without being consumed by it. In the context of leasehold agreements, the freeholder can be seen as a catalyst, as they facilitate the insurance process and ensure that the building is properly covered. However, it's crucial to understand the specific reaction mechanisms at play and how they affect your insurance needs.

The systemic reactions related to leasehold agreements and insurance are complex and multifaceted. They involve a range of stakeholders, including the freeholder, leaseholder, insurance companies, and regulatory bodies. By understanding these system dynamics, you can better navigate the insurance landscape and make informed decisions about your coverage. This requires a deep understanding of the feedback loops and interdependencies within the system, as well as the ability to analyze and respond to emergent behavior.

In terms of optimization, it's essential to consider the Pareto principle when evaluating your insurance needs. This principle states that approximately 80% of results come from 20% of efforts. By focusing on the most critical aspects of your insurance coverage, you can achieve optimal results with minimal effort. This requires a deep understanding of the key performance indicators (KPIs) and success metrics related to your insurance coverage.

Mastering Building Insurance on Your Leasehold Flat

To master building insurance on your leasehold flat, it's essential to develop a strategic approach that takes into account your specific needs and circumstances. This requires a deep understanding of the insurance market, as well as the ability to analyze and compare different policies. By doing so, you can identify the most cost-effective solutions and ensure that you're adequately protected against potential losses.

One of the most effective strategies for mastering building insurance is to benchmark your coverage against industry standards. This involves researching and comparing different insurance policies to identify the most comprehensive and cost-effective options. By doing so, you can ensure that you're getting the best possible coverage for your money and that you're not overpaying for unnecessary features.

Another key strategy is to optimize your premium payments by taking advantage of discounts and incentives. Many insurance companies offer discounts for long-term policies, bundle deals, or loyal customers. By understanding these pricing mechanisms, you can negotiate better rates and reduce your premium payments. Additionally, you can consider installment plans or payment scheduling to make your premium payments more manageable.

In terms of life hacks, one of the most effective ways to master building insurance is to automate your payments. By setting up automatic payments, you can ensure that your premiums are paid on time, and you can avoid late fees or penalties. Additionally, you can consider insurance brokers or financial advisors to help you navigate the insurance landscape and identify the most cost-effective solutions.

Frequently Asked Questions

What is the difference between building insurance and contents insurance?

Building insurance and contents insurance are two distinct types of insurance that serve different purposes. Building insurance covers the physical structure of the building, including the walls, roof, and foundations, as well as any permanent fixtures and fittings. Contents insurance, on the other hand, covers the personal belongings and possessions within the building, such as furniture, electronics, and jewelry. As a leaseholder, you may be responsible for taking out contents insurance to cover your personal belongings, while the freeholder is typically responsible for the building insurance.

In terms of troubleshooting, it's essential to understand the grey areas between building insurance and contents insurance. For example, if you have a fixtures and fittings clause in your leasehold agreement, you may be responsible for insuring certain aspects of the building, such as the kitchen or bathroom. By understanding these boundary conditions, you can ensure that you have adequate coverage and avoid gaps in coverage.

How do I determine the value of my leasehold flat for insurance purposes?

Determining the value of your leasehold flat for insurance purposes requires a deep understanding of the property market and the valuation methods used by insurance companies. One approach is to hire a professional valuer to assess the value of your flat, taking into account factors such as the location, size, and condition of the property. Alternatively, you can use online valuation tools or consult with real estate agents to estimate the value of your flat.

In terms of practical troubleshooting, it's essential to understand the sensitivity analysis involved in determining the value of your leasehold flat. For example, small changes in the valuation methodology or assumptions can result in significant differences in the estimated value. By understanding these uncertainty factors, you can develop a more accurate estimate of your flat's value and ensure that you have adequate insurance coverage.

What happens if I don't have building insurance on my leasehold flat?

If you don't have building insurance on your leasehold flat, you may be exposed to significant financial risks in the event of damage or loss. For example, if the building is damaged in a fire or natural disaster, you may be responsible for contributing to the repair costs, even if you're not the freeholder. Additionally, if you're found to be in breach of your leasehold agreement, you may face penalties or legal action.

In terms of troubleshooting, it's essential to understand the escalation procedures involved in responding to insurance claims. For example, if you need to make a claim, you'll typically need to notify your insurance company and provide documentation to support your claim. By understanding these process maps, you can ensure that you're taking the correct steps to resolve the issue and minimize any potential losses.

By respecting the science behind building insurance on leasehold flats, we can become better, more efficient humans. By understanding the complex system dynamics and feedback loops involved in insurance, we can make informed decisions and optimize our coverage to minimize risks and maximize benefits. Additionally, by developing a deep understanding of the biological and chemical principles underlying insurance, we can better navigate the insurance landscape and identify the most cost-effective solutions.

In conclusion, building insurance on leasehold flats is a critical aspect of responsible property ownership. By mastering the science behind insurance and developing a strategic approach to coverage, we can protect our assets, minimize risks, and ensure that we're adequately prepared for any eventuality. By applying the principles of homeostasis, optimization, and system thinking, we can create a more stable and secure financial environment, both for ourselves and for future generations.