Difference Between P&l Account And Balance Sheet

Let's face it, accounting can be a real snooze-fest, but stick with me here, because we're about to make it cool (or at least, not completely boring). Imagine you're at a restaurant, and you order your favorite burger and fries. You know, the works. Now, when the waiter brings you the bill, you don't just see a list of everything you've ever eaten at the restaurant, do you? Nope, you see a list of just what you ordered that day, with the prices added up. That's kinda like a P&L account - it shows you how your business is doing over a certain period of time, like a month or a year. It's like a snapshot of your financial performance.

But, have you ever tried to gather all your receipts from the past year to see how much you've spent on food? Yeah, it's a real pain. That's kinda like trying to read a balance sheet. It's a list of everything you own (your assets), everything you owe (your liabilities), and how much your business is worth (your equity). It's like taking a photo of your entire financial life - the good, the bad, and the ugly.

So, What's the Big Difference?

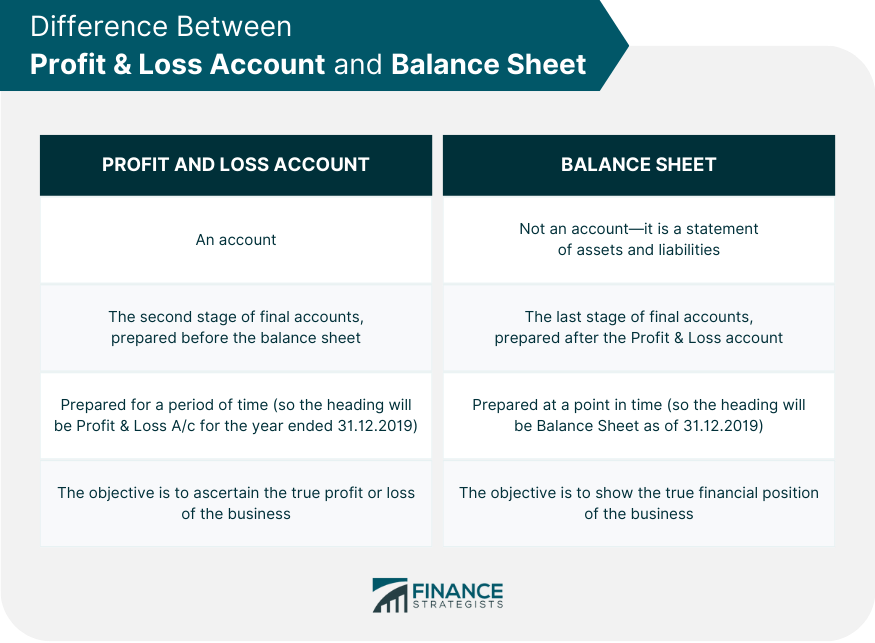

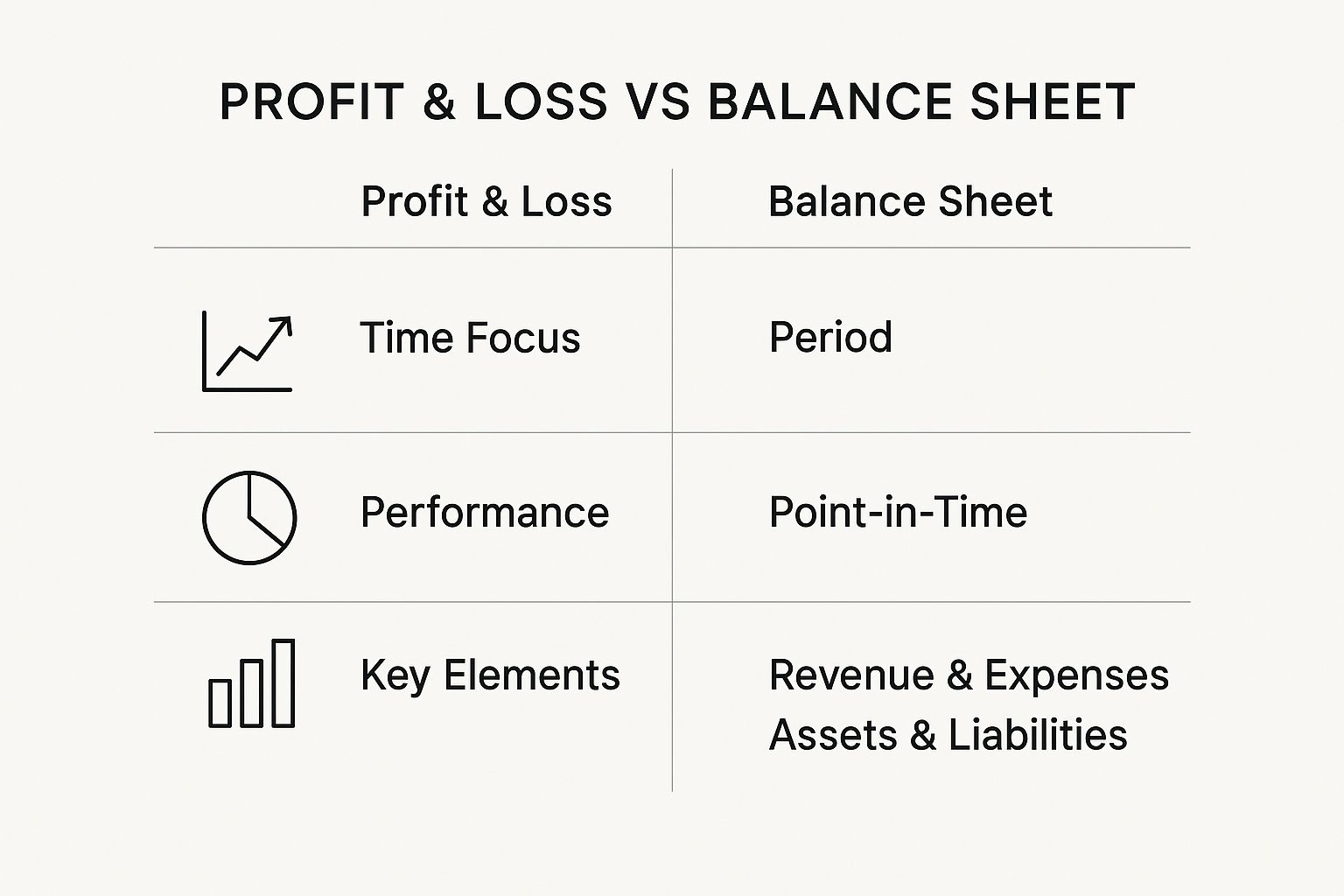

The main difference between a P&L account and a balance sheet is that a P&L account shows you how your business is performing over time, while a balance sheet shows you the financial position of your business at a specific point in time. Think of it like your favorite video game. The P&L account is like the leaderboard, showing you how you've done so far, while the balance sheet is like your character's inventory, showing you what you've got and what you're missing.

Must Read

A Real-Life Example

Let's say you're running a small bakery, and you want to know how you're doing financially. Your P&L account for the month might show that you made $10,000 in sales, but you spent $8,000 on ingredients and supplies, so your net profit is $2,000. Not bad, right? But, your balance sheet might show that you've got $5,000 in cash, $10,000 in assets (like your ovens and mixers), and $8,000 in liabilities (like the loan you took out to buy the bakery). This gives you a snapshot of your financial situation, and helps you decide what to do next.

Now, imagine you're trying to get a loan to expand your bakery. The bank is going to want to see your balance sheet, because they want to know if you've got enough assets to cover the loan, and if you're creditworthy. But, you'll also want to show them your P&L account, so they can see that your business is making money and has a positive cash flow. It's like showing them your report card - you want to prove that you're responsible and can handle the loan.

Why Do I Need Both?

The thing is, you can't just have one or the other - you need both a P&L account and a balance sheet to get a complete picture of your business's financial health. It's like trying to navigate a road trip with only a map or only a compass. You need both to know where you are, where you're going, and how to get there. A P&L account shows you the direction your business is heading, while a balance sheet shows you the current state of your business.

So, there you have it - the difference between a P&L account and a balance sheet. It's not exactly rocket science, but it's not exactly common sense either. Just remember, a P&L account is like a snapshot of your financial performance, while a balance sheet is like a photo of your entire financial life. And, if you're ever stuck, just think of the burger and fries - it's all about the timing, baby!

The Takeaway

In the end, understanding the difference between a P&L account and a balance sheet is crucial for any business owner. It's like having a superpower - you can see into the future (well, at least, you can see your financial future). So, go ahead, grab a snack, and dive into your financial statements. Your business (and your accountant) will thank you. And, who knows, you might just find yourself smiling at the thought of accounting - but don't worry, we won't tell anyone.

As we wrap up this article, I hope you've had a few laughs and learned something new. Accounting might not be the most exciting topic, but it's definitely an important one. So, next time you're looking at your financial statements, just remember - a P&L account is like a leaderboard, and a balance sheet is like your character's inventory. And, if you ever get stuck, just think of the burger and fries. Happy accounting (yes, I said that)!