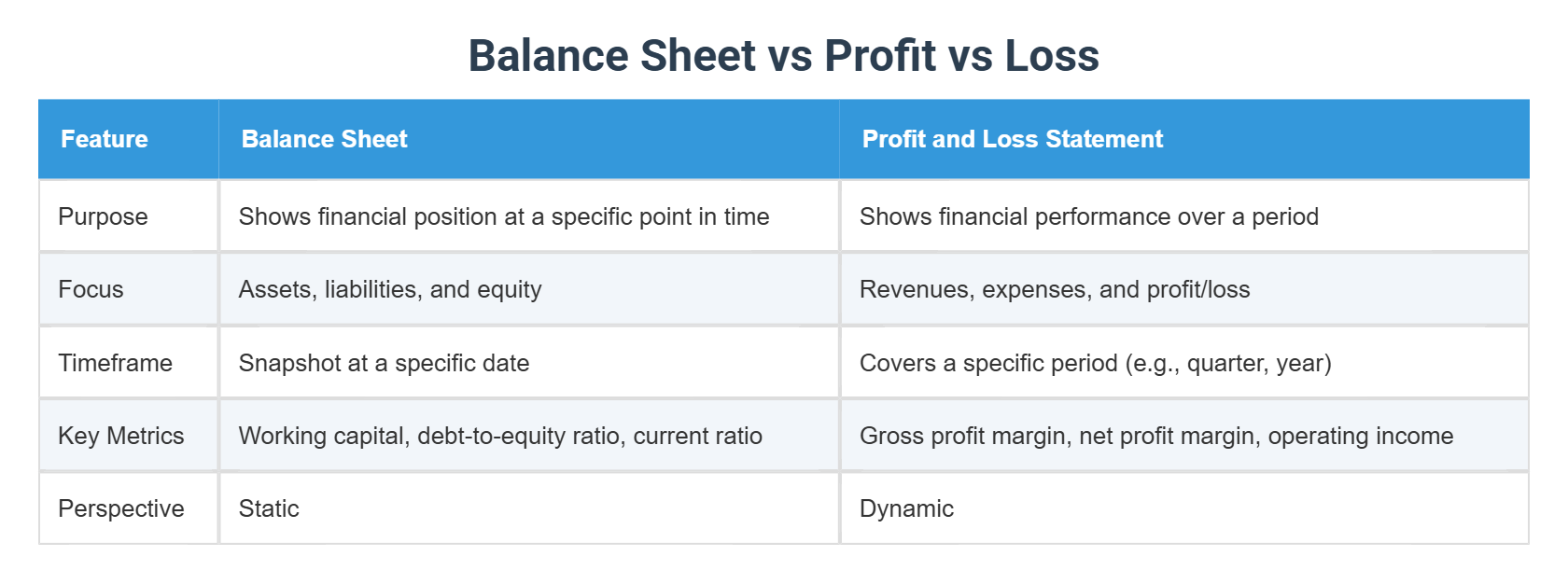

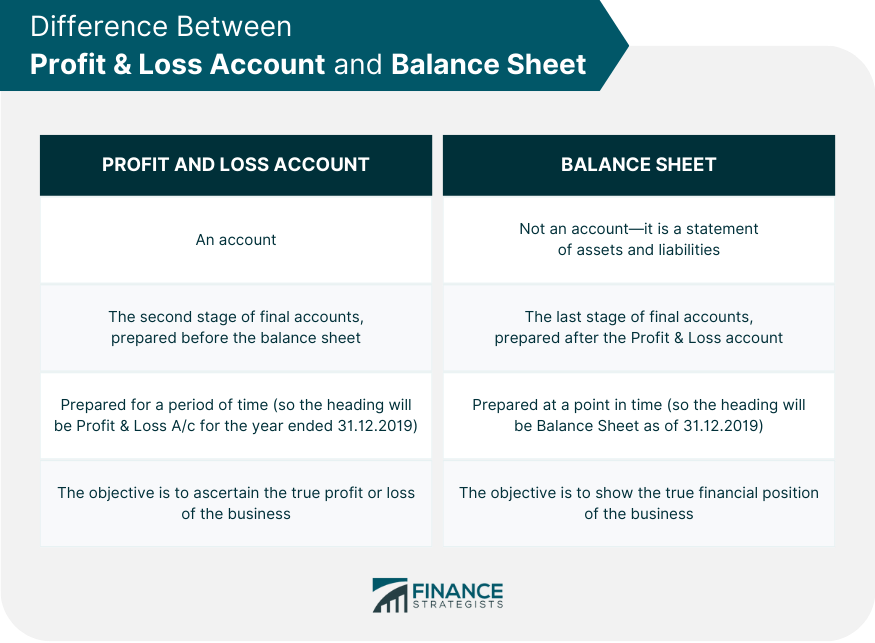

Difference Between A Profit And Loss And A Balance Sheet

When it comes to managing finances, whether personal or business, two essential tools come to mind: Profit and Loss statements and Balance Sheets. Many people enjoy using these financial statements because they provide a clear picture of their financial situation, helping them make informed decisions. The purpose of these statements is to serve as a guide for individuals and businesses to track their income and expenses, identify areas for improvement, and make smart investment choices.

The benefits of using Profit and Loss statements and Balance Sheets are numerous. For one, they help individuals and businesses stay organized and keep track of their finances. By regularly reviewing these statements, people can identify trends, detect potential problems, and make adjustments to achieve their financial goals. For example, a Profit and Loss statement can help a business owner determine whether their company is generating enough revenue to cover its expenses, while a Balance Sheet can provide a snapshot of the company's overall financial health at a given point in time.

Common examples of how these statements are applied can be seen in everyday life. For instance, when applying for a loan or credit card, lenders often require individuals to provide a Balance Sheet to assess their creditworthiness. Similarly, businesses use Profit and Loss statements to evaluate their performance and make informed decisions about investments, expansions, or cutbacks. Even individuals can benefit from creating a personal Balance Sheet to track their assets and liabilities and make smart financial decisions.

Must Read

To enjoy the benefits of these financial statements more effectively, here are some practical tips. First, it's essential to understand the basics of how to read and interpret these statements. This can be achieved by taking a financial literacy course or consulting with a financial advisor. Second, individuals and businesses should regularly review and update their Profit and Loss statements and Balance Sheets to ensure accuracy and stay on top of their finances. Finally, by using accounting software or spreadsheet tools, people can streamline the process of creating and managing these statements, making it easier to analyze their finances and make data-driven decisions.

In conclusion, Profit and Loss statements and Balance Sheets are indispensable tools for anyone looking to manage their finances effectively. By understanding the difference between these two statements and applying the tips outlined above, individuals and businesses can gain a deeper insight into their financial situation, make informed decisions, and achieve their long-term financial goals. Whether you're a seasoned business owner or just starting to manage your personal finances, these statements are essential resources that can help you stay on track and reach financial success.