Credit Score To Get A Citi Credit Card

Okay, so picture this: I'm at a fancy restaurant, trying to impress a date (it didn't work, but that's a story for another time). I confidently pull out my credit card to pay, and the waiter gives me that look. You know the one. The "is-this-going-to-decline?" look. Thankfully, it went through! But the experience got me thinking… what exactly does it take to get approved for a decent credit card these days? Specifically, a Citi card, since they seem to be everywhere.

And that, my friends, is what we're diving into today: your credit score and its mystical power in determining your Citi credit card destiny.

The Credit Score Lowdown: Why It Matters

Let's be honest, credit scores can feel like some arbitrary number assigned by a shadowy organization. But in reality, it’s a pretty good indicator of how responsible you are with borrowed money. Banks, like Citi, use it to gauge the risk of lending you money. The higher your score, the lower the risk, and the better your chances of getting approved (and with a decent interest rate, thank you very much).

Must Read

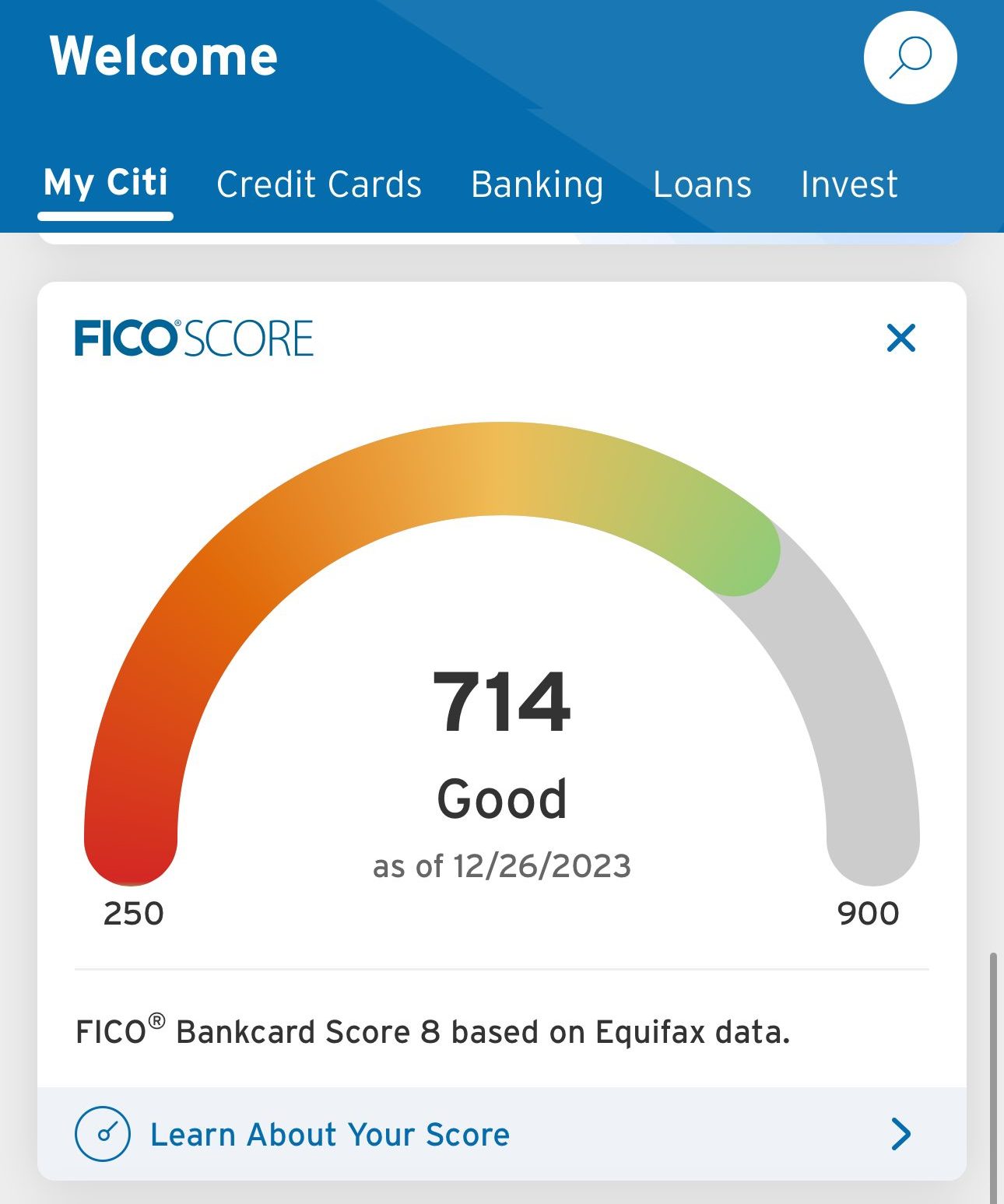

Generally, credit scores range from 300 to 850. Here’s a quick breakdown:

- Poor (300-579): Uh oh. Probably best to work on building up your score before applying.

- Fair (580-669): You're getting there, but options might be limited. Think secured cards or cards with higher interest rates.

- Good (670-739): Now we're talking! You'll likely qualify for some decent cards.

- Very Good (740-799): Excellent! Many options are available, including some rewards cards.

- Exceptional (800-850): Congrats! You're basically a credit card god/goddess. Go forth and reap the rewards (responsibly, of course!).

(Psst… If you don't know your credit score, there are tons of free websites to check it. Just Google it – but make sure it’s a reputable site! Don’t give your info to just anyone.)

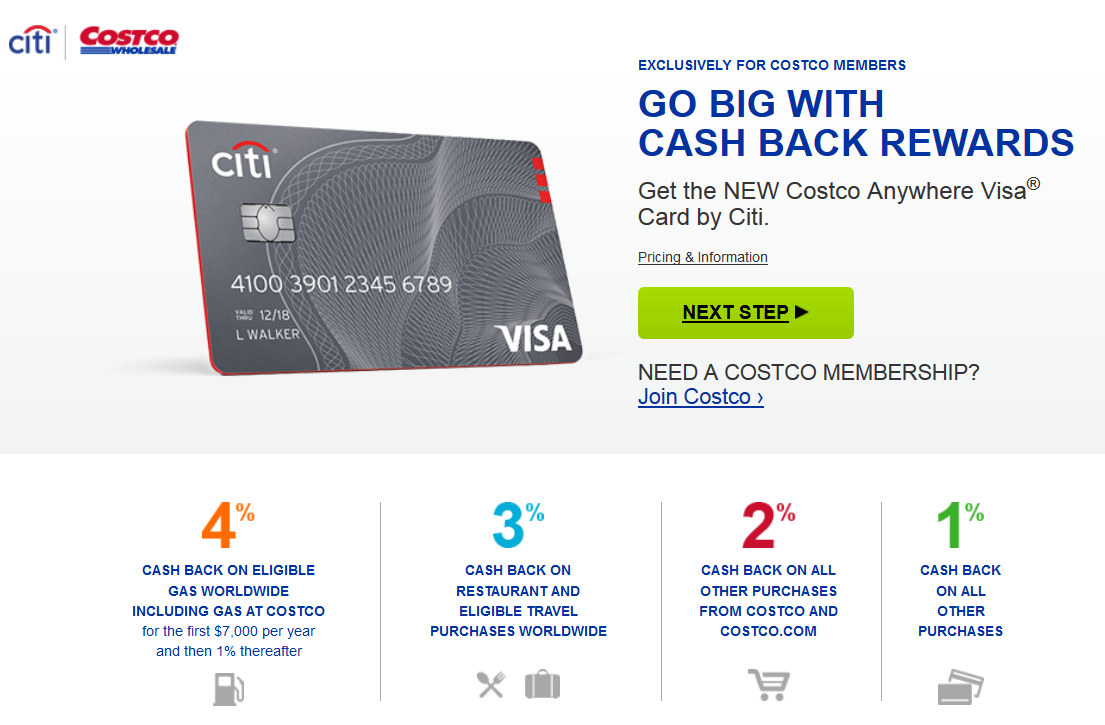

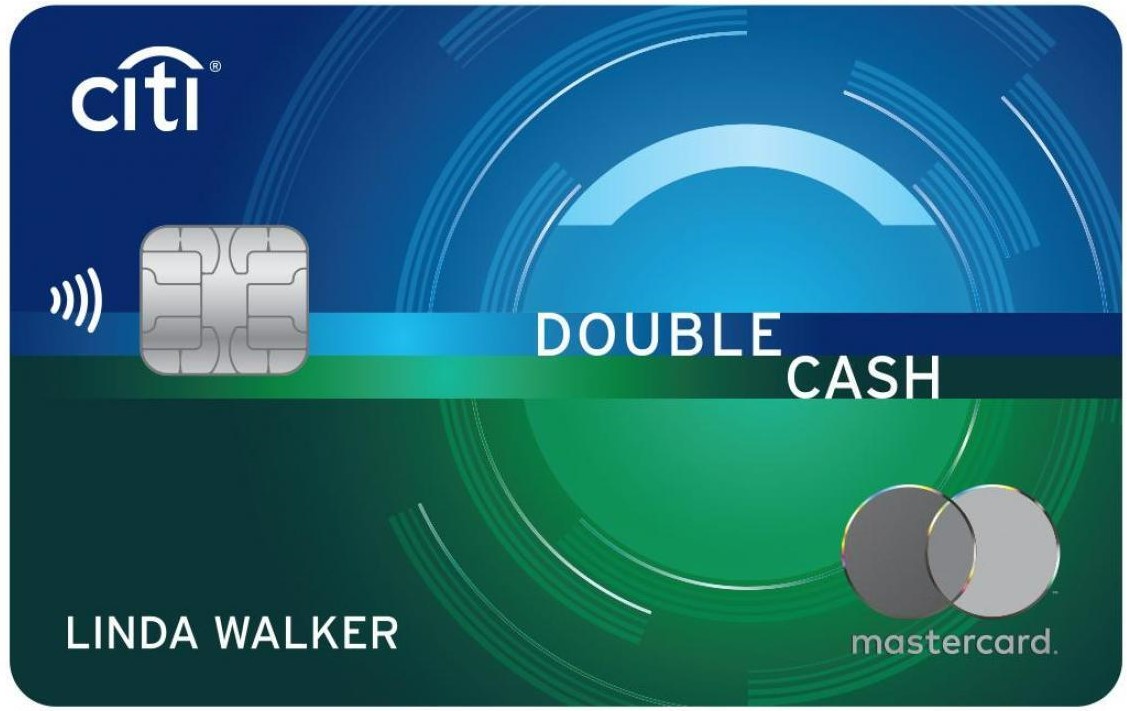

Citi Credit Cards: A Score for Every Style

Citi offers a range of credit cards, from basic cash-back options to premium travel rewards cards. And, surprise surprise, the credit score you need varies depending on the card. It's not a one-size-fits-all situation, sadly. I wish it were that simple!

Here's a very general guideline (because, disclaimer, Citi doesn't publish exact score requirements. Sneaky, I know!):

- For entry-level or secured Citi cards: A fair credit score (580-669) might get you approved, but you'll likely need to prove income stability and have a clean credit report (no recent bankruptcies or major delinquencies).

- For mid-tier Citi cards (like some cash-back cards): Aim for a good credit score (670-739). This will significantly increase your chances of approval and get you better terms.

- For premium Citi cards (think travel rewards cards with sweet perks): You’ll almost certainly need a very good to exceptional credit score (740+). These cards are highly competitive, and Citi wants to be sure you’re a reliable borrower.

Remember these are estimates. Other factors like your income, employment history, debt-to-income ratio, and overall credit history all play a role. They want to see you can actually afford to use the card responsibly, not just rack up debt.

Beyond the Score: Other Things to Consider

Okay, so you know your credit score. But don't rest on your laurels! Citi (and other lenders) also look at:

- Your credit report: This is a detailed history of your credit activity. Any late payments, defaults, or bankruptcies will raise red flags.

- Your income: Can you actually afford to pay off your balance each month? They need to know you're not living beyond your means.

- Your debt-to-income ratio (DTI): This is the percentage of your monthly income that goes towards debt payments. A lower DTI is always better.

- Length of credit history: The longer you've been using credit responsibly, the better. A longer track record gives them more confidence.

So, yeah, it’s a whole package deal. Think of it like applying for a job. Your credit score is like your GPA, but your credit report and financial history are like your resume and references.

The Takeaway

Getting a Citi credit card (or any credit card, really) is all about showing lenders you're a responsible borrower. Building and maintaining a good credit score is essential, but it's not the only factor. Keep your credit report clean, manage your debt wisely, and demonstrate a stable income. And hey, if you get rejected the first time, don't give up! Work on improving your credit profile and try again in a few months. You got this!