Credit Score Needed For Capital One

Okay, let's talk about Capital One. Not the Viking helmet commercials (though those are pretty great), but the credit cards. Specifically, the question everyone Googles late at night: "What credit score do I need to actually get one?" It's like trying to figure out the secret handshake to a cool club, only the bouncer is a robot powered by algorithms.

The Credit Score Mystery: More Than Just a Number

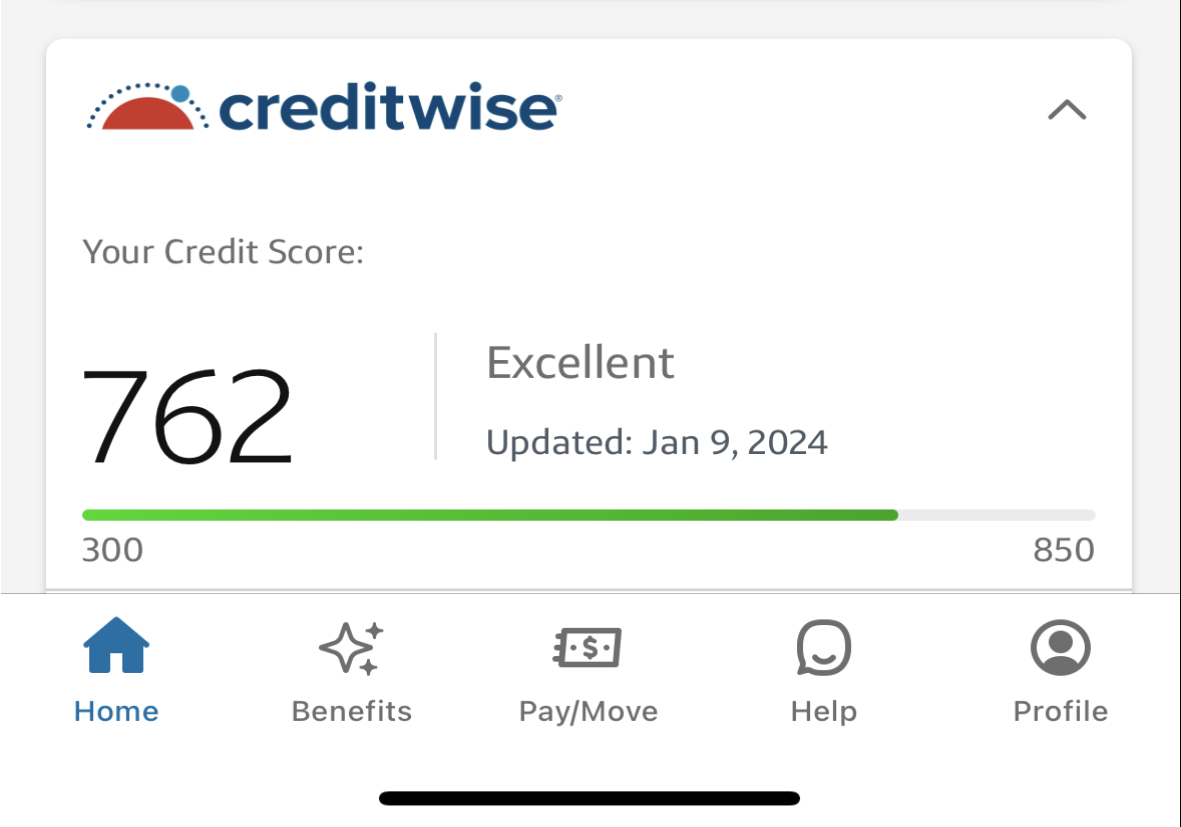

First, let's debunk a myth. There's no single, magic number. It's not like you hit 700 and suddenly confetti rains down and a Capital One card appears in your mailbox. Think of your credit score as more of a...vibe. A general feeling you're giving off about your ability to handle money responsibly. Are you a responsible adult who pays bills on time, or are you more of a "I'll pay it...eventually" type? Credit scores are trying to answer that question.

Capital One, bless their data-driven hearts, offers a range of cards, which means different cards have different standards. This is where it gets interesting. You might not qualify for the fancy travel rewards card with all the bells and whistles if your credit history is...let's say "developing." But, fear not! There are cards designed for people who are building (or rebuilding) their credit.

Must Read

Think of it like levels in a video game. You start at Level 1 (maybe even Level 0 if you're new to credit) and work your way up. Capital One has cards for each level. Some are designed for those with "fair" credit (generally scores in the 630-689 range), while others are for those with "excellent" credit (720+). The higher your score, the cooler the rewards (and the lower the interest rates!).

Beyond the Numbers: Real-Life Credit Card Adventures

Here's where the humor comes in. We've all heard stories about people denied credit cards for the silliest reasons. Maybe they typoed their address or forgot to include a middle initial. It's like failing a test because you forgot to write your name! The good news is that Capital One, like most lenders, will send you a letter explaining why you were denied. This is your chance to play detective and figure out what went wrong.

One heartwarming aspect of the credit card game is watching someone diligently rebuild their credit after a setback. Maybe they had some tough times, missed a few payments, and saw their score plummet. But, with perseverance, responsible spending habits, and maybe a secured credit card (which requires a security deposit), they can slowly but surely climb back up the credit score ladder. It's a financial comeback story worthy of a movie!

Tips for Cracking the Capital One Code

So, what's the takeaway? Here are a few tips for increasing your chances of getting that Capital One card you've been eyeing:

- Check your credit report: Know what's on it! You can get a free copy from annualcreditreport.com.

- Pay your bills on time: This is the golden rule of credit.

- Keep your credit utilization low: Don't max out your credit cards. Aim to use less than 30% of your available credit.

- Be patient: Building good credit takes time. It's not a sprint, it's a marathon.

And remember, don't be afraid to start small. A secured credit card or a card designed for those with fair credit can be a great stepping stone to bigger and better things. Think of it as your financial training wheels.

Ultimately, getting a Capital One card isn't about hitting some arbitrary number. It's about demonstrating that you're responsible with money. It's about building a credit history that shows you're a reliable borrower. And who knows, maybe one day you'll be the one giving out advice to friends and family, sharing your own credit card success story. Just don't forget to thank those Viking helmet guys for the inspiration!

"Capital One: What's in your wallet? Hopefully, a good credit score!"