Closing Costs On 185 000 House

Okay, so you're eyeing that cozy little abode, right? The one with the questionable landscaping and the slightly-too-close-to-the-neighbor's-garage placement? Let's say it's going for a cool $185,000. Awesome! But hold your horses (or unicorns, if that’s more your style), because that sticker price isn't the whole enchilada. We gotta talk closing costs. Think of them as the surprise party that your bank throws for you, only instead of cake and balloons, it's fees and paperwork. Joy!

What are closing costs, you ask? Well, imagine you’re throwing a really, really complicated party. You need to pay the caterer (the appraiser), the DJ (the title company), and the bouncer (your lender). All those folks need to get paid, and that, my friend, is essentially what closing costs are. They're the various fees and expenses associated with finalizing your mortgage and transferring ownership of the property.

The Closing Cost Culprits: A Rogues' Gallery

So, who are the usual suspects in this closing cost caper? Let's take a peek at the lineup:

Must Read

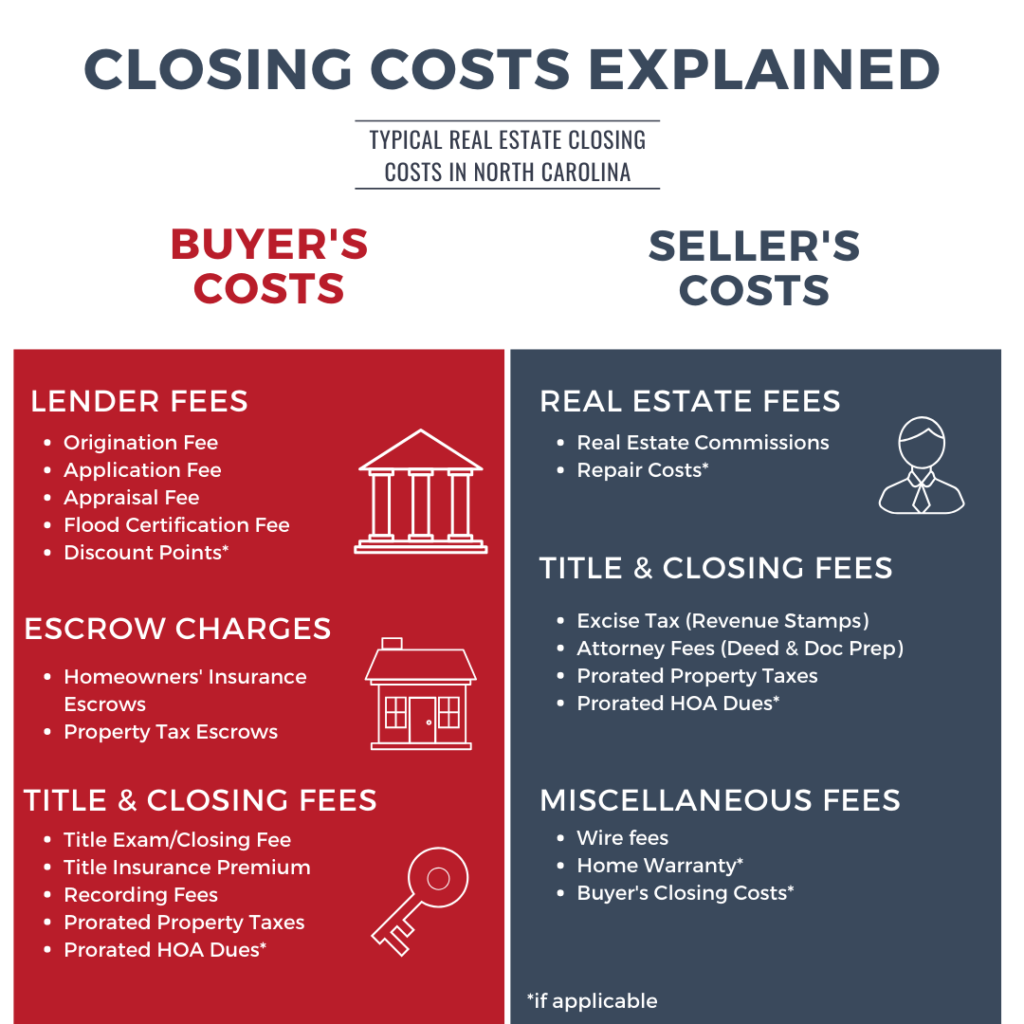

- Appraisal Fee: Remember that caterer I mentioned? This pays for someone to come out and tell the bank if your potential new home is actually worth $185,000. If they come back and say it's only worth $2 and a bag of chips, you might have a problem. Expect to shell out somewhere between $300 and $500 for this.

- Title Insurance: This is like getting insurance for your insurance. Seriously. It protects you (and the lender) if someone later pops up claiming they actually own the property. Think of it as a shield against surprise zombie heirs. Could run you anywhere from $500 to over $1,000.

- Loan Origination Fee: This is what the lender charges you for the sheer audacity of letting them loan you money. It's usually expressed as a percentage of the loan amount, often around 0.5% to 1%. So, for our $185,000 house, we're talking somewhere between $925 and $1850. Ouch.

- Recording Fees: Basically, the government charges you to officially record the deed, making it official that you are now the proud owner of that slightly-too-close-to-the-neighbor’s-garage house. These are usually relatively small, maybe $100 to $200.

- Property Taxes and Homeowner's Insurance: You might have to prepay some of these upfront to get things moving. The amounts vary wildly depending on where you live, of course. Think of them as welcoming gifts to your local municipality and insurance company!

Now, I know what you're thinking: "This sounds like a lot of money!" And you're right, it is. The good news? Closing costs are negotiable. Sometimes.

Decoding the Cost: How Much Can You Expect on a $185,000 House?

Alright, let’s get down to brass tacks. Generally speaking, closing costs typically range from 2% to 5% of the loan amount. So, on our $185,000 house, you're looking at somewhere between $3,700 and $9,250. Yes, that’s a pretty wide range. It depends on your location, the type of loan you’re getting, and how good you are at haggling.

Important note: This is just a rough estimate. Don’t take this as gospel. Your best bet is to get a Loan Estimate from your lender. This document will break down all the estimated costs associated with your specific loan. It’s like a crystal ball, but instead of seeing your future love life, you see your future expenses. Less romantic, but arguably more useful.

Haggling for Heroes (and Homebuyers)

Okay, so how do you avoid feeling like you've been robbed blind? Time for some negotiation ninjutsu!

- Shop around for lenders: Different lenders charge different fees. Get quotes from multiple lenders and compare them carefully. Don't be afraid to play them against each other. “Lender A is offering me a lower origination fee… can you beat that?”

- Negotiate with the seller: In some cases, you can negotiate with the seller to cover some of the closing costs. This is more common in a buyer's market, where there's more competition among sellers. It never hurts to ask. The worst they can say is no (and then you dramatically faint from disappointment).

- Look for assistance programs: Many states and local governments offer programs to help first-time homebuyers with closing costs. Do your research and see what's available in your area. Free money is good money!

Don't be afraid to ask questions! Your lender should be able to explain all the fees in detail. If they can't, or if they seem shady, find a different lender. You want someone who's transparent and trustworthy, not someone who's going to disappear with your money and move to a remote island.

The Bottom Line (and Your Bank Account)

Buying a house is a big deal, and closing costs are a significant part of the process. Don't let them catch you off guard. Do your research, shop around, and negotiate like your financial future depends on it (because it kind of does). And remember, a little bit of preparation can save you a whole lot of money (and stress) in the long run. Now go forth and conquer that real estate market! You got this!