Can You Use No Claims Discount On 2 Cars

As we navigate the complexities of our modern lives, it's not uncommon to find ourselves pondering the intricacies of insurance policies, particularly when it comes to our vehicles. One aspect that often sparks curiosity and, sometimes, anxiety is the concept of No Claims Discount (NCD) and its application across multiple cars. But why does this topic resonate so deeply with us? To understand this, we must delve into the psychological underpinnings that drive our perceptions and reactions towards insurance and financial planning. Our brains are wired to respond to the prospect of saving money and mitigating risk, which is fundamentally what NCD is about. This innate desire for security and the fear of financial loss can evoke strong emotional responses, making the consideration of using NCD on two cars a deeply personal and somewhat daunting decision.

Furthermore, the relevance of this topic in today's fast-paced, financially cautious world cannot be overstated. With the rising costs of living and the ever-present uncertainty of the future, individuals are increasingly seeking ways to optimize their financial strategies. The ability to apply NCD to multiple vehicles not only represents a potential for significant savings but also symbolizes a sense of control and foresight in one's financial planning. This sense of control is empathetically reassuring, as it speaks to our basic human need for security and stability. However, the process of understanding and navigating the rules surrounding NCD can be overwhelming, leading to a mix of emotions ranging from anxiety to relief, depending on one's circumstances and understanding of the policy.

The modern relevance of this topic is also underscored by the shift in lifestyles and the increasing number of households with multiple vehicles. As families grow and expand, so do their needs for transportation, leading to a scenario where managing insurance for multiple cars becomes a significant aspect of household financial planning. The possibility of leveraging NCD across these vehicles can thus be seen as a catalyst for personal growth, as individuals are prompted to engage more deeply with their financial planning, embracing a more proactive and informed approach to managing risk and securing their financial futures.

Must Read

Understanding the Psychological and Emotional Aspects

Diving deeper into the psychological and emotional aspects of using NCD on two cars, it becomes apparent that this decision is often influenced by cognitive biases and emotional triggers. For instance, the endowment effect might lead individuals to overvalue the potential savings from NCD, making the decision seem more critical than it actually is. Conversely, the fear of loss can cause people to be more cautious, sometimes to the point of inaction, when considering changes to their insurance policies.

In real-life scenarios, these biases and triggers can play out in vivid and relatable ways. Consider a family with two cars, both essential for daily commuting and family activities. The prospect of applying NCD to both vehicles might evoke a sense of excitement and anticipation regarding the potential savings, but it could also be met with apprehension due to concerns about policy complexities and the risk of losing the discount. This emotional rollercoaster underscores the complex psychological dynamics at play when making decisions about NCD and multiple vehicle insurance.

Moreover, the process of researching and understanding NCD policies can itself be a source of stress and anxiety, as individuals must navigate a myriad of terms, conditions, and potential pitfalls. This stress can be further compounded by the pressure to make the right decision, as the financial implications of choosing incorrectly can be significant. Therefore, it's crucial for individuals to approach this decision with a clear understanding of their financial situation, insurance needs, and the specific rules governing NCD in their region.

The emotional and psychological aspects of this decision are also closely tied to an individual's overall financial literacy and confidence. Those with a solid grasp of insurance principles and a history of successfully managing their finances might approach the decision with a sense of calm and competence, while others might feel overwhelmed and uncertain. This disparity highlights the importance of education and self-reflection in navigating the complexities of NCD and multiple vehicle insurance.

Coping Mechanisms and Mindset Shifts

To effectively navigate the complexities and emotions surrounding the use of NCD on two cars, it's essential to develop actionable coping mechanisms and undergo mindset shifts. One of the first steps is to seek professional advice, consulting with insurance experts who can provide personalized guidance based on one's specific situation and needs. This professional insight can help alleviate uncertainty and doubt, replacing them with a sense of clarity and direction.

Additionally, adopting a proactive mindset towards financial planning can be incredibly empowering. This involves regularly reviewing insurance policies, staying informed about changes in the insurance market, and being open to adjusting one's strategy as circumstances change. Such a mindset not only helps in making informed decisions about NCD but also contributes to a broader sense of financial well-being and security.

A crucial mindset shift involves recognizing that the decision to use NCD on two cars is not a one-time event, but rather part of an ongoing process of financial management. By embracing this perspective, individuals can move away from short-term anxiety and towards a long-term vision that prioritizes sustained financial health and stability. This shift in perspective can lead to a more balanced approach to insurance and financial planning, one that emphasizes flexibility and adaptability in the face of changing circumstances.

Furthermore, leveraging technology and digital tools can significantly simplify the process of managing multiple vehicle insurance policies and tracking NCD. From online platforms that compare insurance quotes to apps that help monitor and manage policies, there are numerous resources available that can reduce the administrative burden and provide peace of mind. By harnessing these tools, individuals can streamline their financial management, reducing stress and freeing up time and energy for other aspects of their lives.

Frequently Asked Questions

Can I Use My No Claims Discount on Two Cars Simultaneously?

This question is at the heart of many discussions about NCD and multiple vehicle insurance. The answer depends on the specific insurance provider and the terms of the policy. Some insurers may allow the use of NCD on a second vehicle, either by mirroring the NCD from the first vehicle or by offering a reduced rate for the second vehicle based on the NCD earned. However, it's crucial to understand that rules and offerings can vary widely, and not all insurers may provide this flexibility. Therefore, it's essential to consult directly with the insurance company to determine the exact possibilities and limitations.

In navigating this aspect, it's also important to consider the psychological impact of uncertainty. When individuals are unclear about their options regarding NCD on multiple vehicles, they may experience increased anxiety and stress. By seeking clear and direct communication with their insurer, individuals can mitigate these negative emotions, replacing them with a sense of confidence and certainty about their financial decisions.

How Does No Claims Discount Affect My Premiums When I Have Two Cars?

The impact of NCD on premiums for two cars can be significant, but it depends on how the NCD is applied and the specific terms of the insurance policies. Generally, if NCD can be used on the second vehicle, it could lead to substantial savings on the premiums for that vehicle. However, the extent of these savings will depend on the NCD percentage that can be applied and the base premium of the second vehicle. It's also worth noting that some insurers might offer additional discounts for insuring multiple vehicles with them, further reducing the overall cost.

From a psychological standpoint, the potential for savings through NCD can evoke feelings of excitement and motivation, as individuals see a direct and tangible benefit from their responsible driving and financial planning. This positive reinforcement can encourage a long-term commitment to safe driving practices and diligent financial management, contributing to a more stable and secure financial future.

Can I Transfer My No Claims Discount to a New Car?

Transferring NCD to a new car is generally possible, but the process and any associated restrictions can vary between insurers. Typically, if you're replacing your current vehicle with a new one, you can transfer your NCD to the new vehicle's insurance policy. However, if you're adding a new vehicle to your household (in addition to the one you already insure), the ability to use your existing NCD on this new vehicle will depend on the insurer's policies regarding multiple vehicle discounts and NCD application.

This aspect of NCD highlights the importance of flexibility and adaptability in financial planning. As life circumstances change, whether through the purchase of a new vehicle or other significant events, being able to adjust one's insurance strategy while retaining the benefits of NCD can provide a sense of security and continuity. This ability to adapt and make the most of available financial tools and discounts can significantly reduce stress and contribute to a sense of financial well-being.

Does No Claims Discount Apply to Named Drivers on My Policy?

The application of NCD to named drivers on a policy can vary, and it's an area where the rules can be particularly complex. Generally, NCD is associated with the policyholder rather than the vehicle or other drivers. However, some insurers may offer discounts or special considerations for named drivers who have their own NCD or meet certain criteria. It's essential to review the policy terms or consult with the insurer to understand how NCD applies in scenarios involving named drivers.

From an emotional and psychological perspective, understanding how NCD applies to named drivers can alleviate concerns about fairness and equity. When all parties involved in the insurance policy understand their roles and how NCD impacts their premiums and driving records, it can foster a sense of trust and cooperation, which is particularly important in household or family settings where multiple individuals may be involved in the policy.

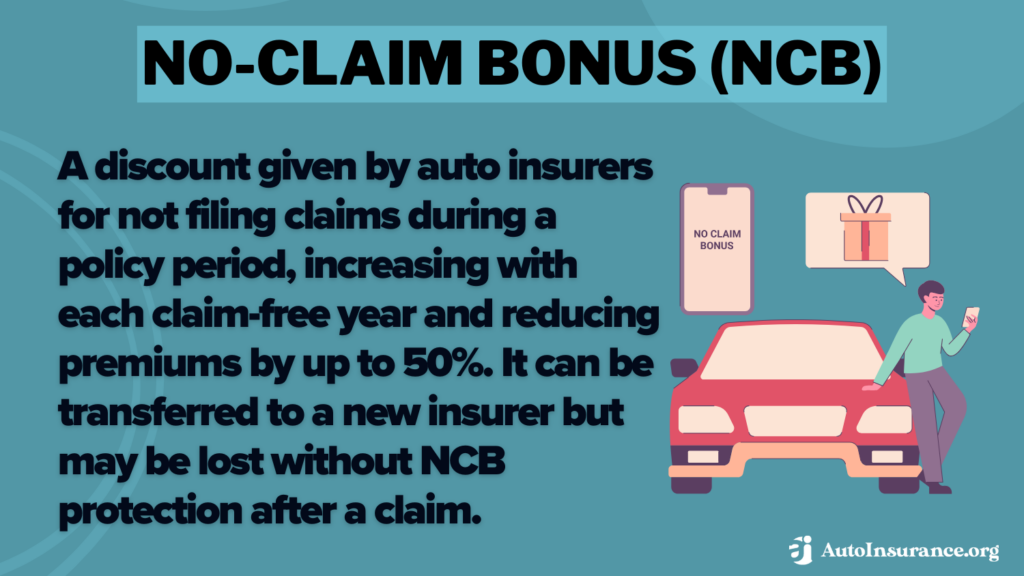

How Long Does No Claims Discount Last?

The duration for which NCD lasts can depend on several factors, including the insurer's policies and any claims made on the insurance. Typically, NCD accumulates over years of claim-free driving and can be maintained as long as the policyholder continues to drive safely and doesn't make any claims that would affect their NCD. However, if a claim is made, the NCD may be reduced or lost, depending on the insurer's rules and the nature of the claim.

The concept of NCD lasting over time underscores the value of long-term thinking and responsibility in financial planning. By prioritizing safe driving practices and maintaining a good driving record, individuals can secure long-term benefits through NCD, reflecting a commitment to prudence and foresight in their financial decisions. This commitment not only leads to financial savings but also contributes to a sense of personal satisfaction and fulfillment, knowing that one's efforts are yielding tangible rewards over time.

As individuals master the intricacies of using NCD on two cars, they embark on a journey of personal growth and financial maturity. This process involves not just understanding insurance policies but also developing a deeper awareness of one's financial needs, risks, and long-term goals. By navigating the complexities of NCD with empathy, introspection, and a willingness to learn, individuals can cultivate a more balanced and assured approach to financial planning, one that is grounded in a thorough understanding of the psychological, emotional, and practical aspects of insurance and risk management.

In conclusion, the ability to use NCD on two cars represents more than just a financial strategy; it symbolizes a proactive and informed approach to managing one's financial future. By embracing this aspect of insurance with a mindset that is both resilient and adaptable, individuals can transform their relationship with financial planning, turning what might seem like a daunting task into an empowering journey of discovery and growth. This journey, marked by a deeper understanding of NCD and its applications, can lead to a more secure, stable, and fulfilling life, where the challenges of navigating complex insurance policies are met with confidence, clarity, and a profound sense of personal and financial well-being.