Can I Refinance My Car With A 650 Credit Score

So, you're thinking about refinancing your car, eh? Maybe you're picturing yourself cruising down the highway, windows down, saving a sweet chunk of change every month. But there's that nagging question in the back of your mind: "Can I even do that with my credit score?".

Let's talk about that 650 credit score! Is it a golden ticket? Maybe not. Is it a deal-breaker? Absolutely not! Think of it as a "maybe-ish" kind of situation.

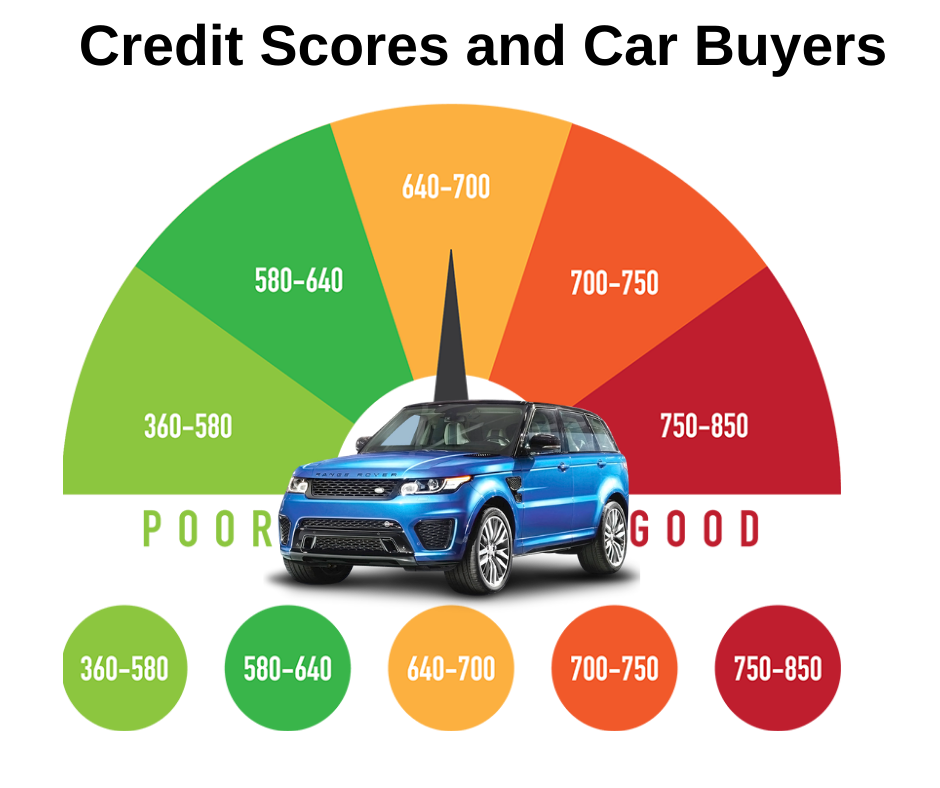

The 650 Credit Score Landscape

A 650 credit score generally lands you in the "fair" credit category. It's not terrible, it's not amazing, it's... perfectly average! Like a perfectly average cup of coffee. It'll get the job done.

Must Read

Lenders see it as a mixed bag. They're not going to slam the door in your face, but they're probably not going to roll out the red carpet either. You're in a negotiation zone, my friend!

But here’s the deal: refinancing with a 650 credit score is possible. It just means you might have to work a little harder to snag that dream interest rate. Think of it as a quest! A quest for financial awesomeness!

What Influences Your Refinance Approval?

Your credit score is definitely a big player in the refinance game. But it’s not the only player. It's more like the quarterback of a football team; important, but needs a good team around him.

Lenders are also going to peek at other aspects of your financial life. Things like your income, your debt-to-income ratio, and the age and mileage of your car.

Income is Key: Can you comfortably afford the monthly payments? Lenders want to know you're not going to default and leave them holding the bag. Show them the money! Show them you're responsible!

Debt-to-Income Ratio (DTI): This is basically how much of your income is already going towards debt payments. The lower the DTI, the better. Try to keep it under 40%. Imagine lenders are like judgmental relatives looking at your budget. Don’t let them frown!

The Car Itself: A lender will assess your car's value and loan-to-value (LTV) ratio. LTV compares the loan amount to the car's current market value. The closer your car value to your loan, the better your approval chances.

Basically, you're showing the lender the whole picture. You're not just a credit score; you're a responsible adult (probably!) who deserves a better deal on their car loan.

Boosting Your Chances of Refinancing Success

Okay, so you're armed with the knowledge. Now, let's get you ready for battle! Here are a few strategies to boost your chances of refinancing glory:

Check Your Credit Report: This is crucial! Snag a copy of your credit report from Experian, Equifax, and TransUnion. Look for any errors or inaccuracies. Dispute anything that's not right. Fixing even a small error can bump your score up a few points.

Pay Down Debt: Even a small dent in your existing debt can make a big difference. Focus on paying down credit card balances. It shows lenders you're serious about managing your finances.

Get a Co-signer: If you have a friend or family member with excellent credit, consider asking them to co-sign your refinance loan. This can significantly improve your chances of approval and snag you a better interest rate. But remember, it's a big responsibility for them, so make sure you can definitely handle the payments!

Shop Around: Don't settle for the first offer you get! Compare rates from multiple lenders, including banks, credit unions, and online lenders. Each lender has different criteria, so you might find one that's more willing to work with your 650 credit score. Treat finding the right lender like finding the perfect avocado: you have to squeeze a few before you find the ripe one!

Highlight Your Strengths: Did you just get a raise? Have you been consistently employed for a long time? Make sure the lender knows about it! Show them you're a solid borrower. Sell yourself! (Ethically, of course!).

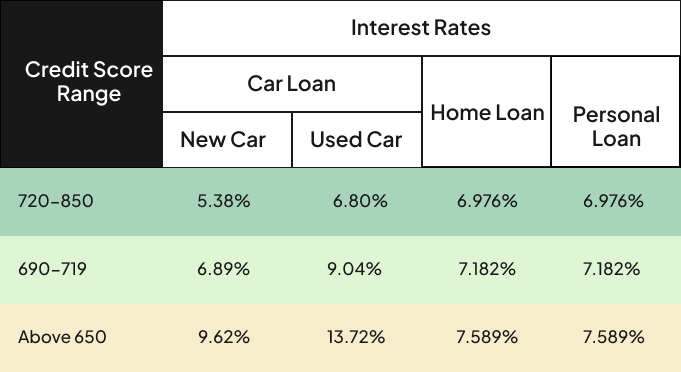

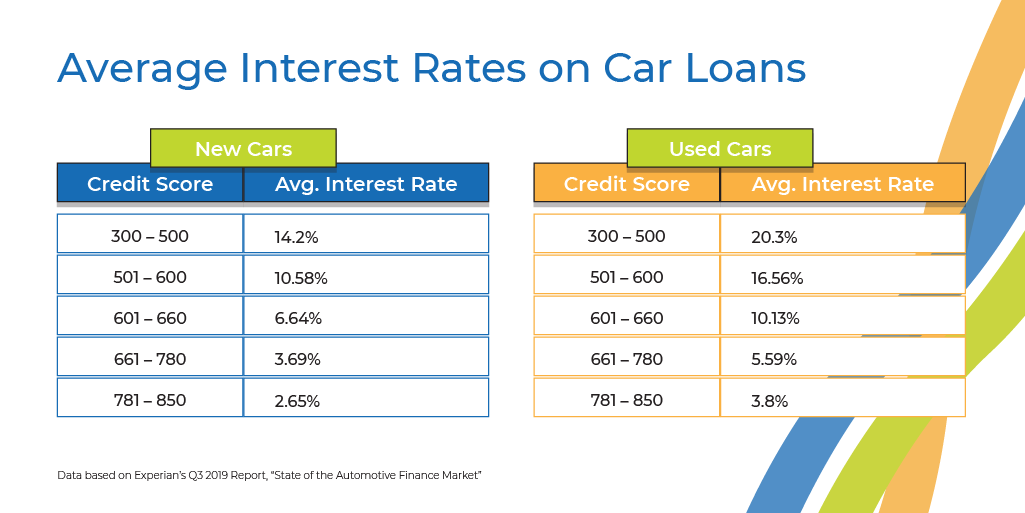

What Kind of Interest Rate Can You Expect?

Alright, let's talk numbers! With a 650 credit score, you're probably not going to get the rock-bottom, advertised interest rates. Those are usually reserved for borrowers with near-perfect credit. That’s reality!

But that doesn't mean you're doomed to pay through the nose. You can still find a reasonable interest rate, especially if you follow the tips above. Be prepared to shop around and negotiate! Negotiation is like haggling at a flea market, but with bigger numbers and slightly less awkward eye contact.

.png)

Expect interest rates to be higher compared to someone with a 750+ credit score. However, even a slightly lower interest rate than what you're currently paying can save you significant money over the life of the loan. Every little bit counts!

You can use online car refinance calculators to estimate potential savings. Play around with different interest rates and loan terms to see how they impact your monthly payments and total interest paid. Knowledge is power! And in this case, it's also potential savings!

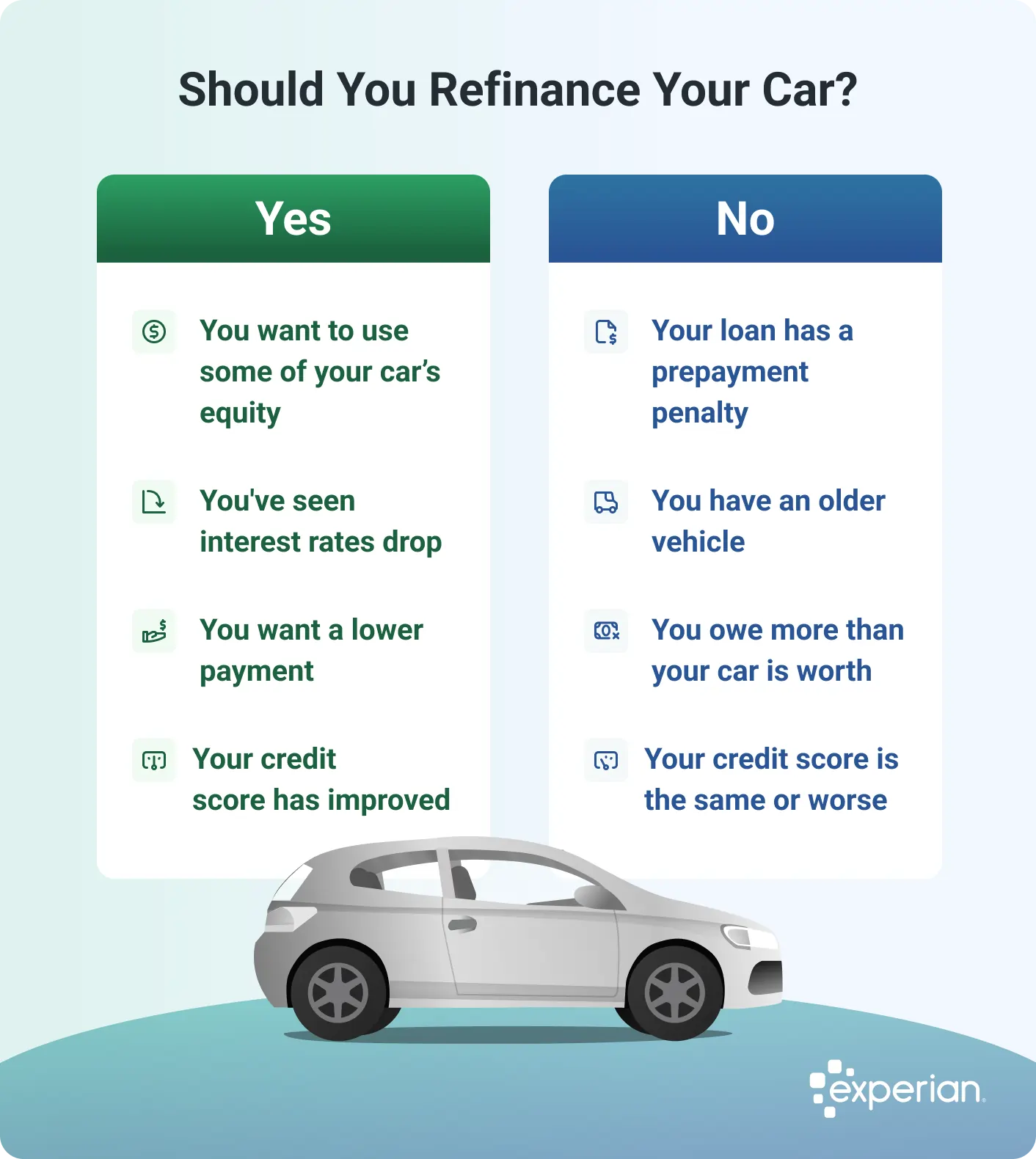

When Refinancing Might Not Be the Best Idea

Before you jump headfirst into refinancing, let's pump the brakes for a second. Sometimes, refinancing might not be the smartest move. Gasp! I know, shocking, right?

Short Remaining Loan Term: If you only have a few months left on your current car loan, the savings from refinancing might not be worth the hassle and potential fees. Do the math! Sometimes the juice ain't worth the squeeze.

High Prepayment Penalties: Check your current loan agreement for any prepayment penalties. These are fees you have to pay for paying off your loan early. If the penalty is high, it could negate any savings from refinancing.

.png)

Underwater Car Loan: This is when you owe more on your car than it's actually worth. This can make it difficult to get approved for refinancing, as lenders are hesitant to finance a loan that's worth more than the asset.

Minimal Interest Rate Savings: If you can only shave off a tiny percentage point from your current interest rate, the savings might not be worth the time and effort. Factor in any fees associated with refinancing. Make sure the benefits outweigh the costs.

Basically, it's all about weighing the pros and cons. Is refinancing going to save you money in the long run? Or are you just spinning your wheels? (Pun intended!).

The Bottom Line: Refinancing with a 650 Credit Score

So, can you refinance your car with a 650 credit score? The answer is a resounding... maybe! It's not a guaranteed "yes," but it's definitely not an automatic "no."

You'll need to do your homework, shop around, and potentially improve your financial profile. But with a little effort, you can absolutely find a better interest rate and save some serious cash. Think of it as a financial glow-up for your car loan!

Remember, knowledge is power! The more you know about your credit score, your financial situation, and the refinancing process, the better equipped you'll be to make informed decisions. Now go forth and conquer the world of car refinancing!