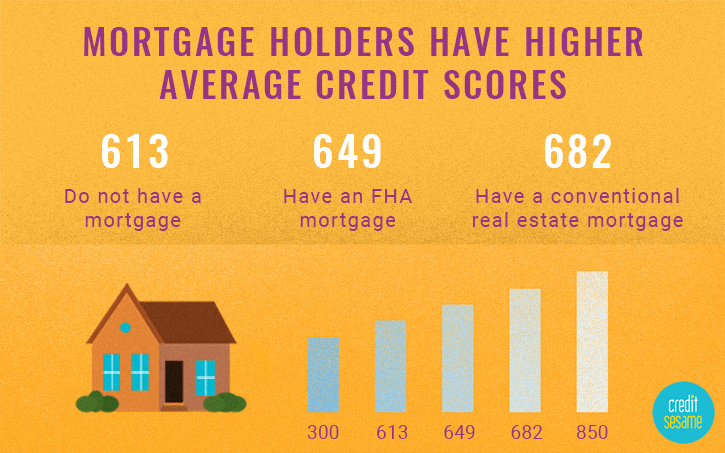

Can I Buy A House With A 524 Credit Score

Okay, let's talk about something that can feel a little…intimidating. Buying a house. The American Dream, right? But what happens when your credit score feels more like a nightmare than a dream come true? Specifically, let's tackle the big question: Can you actually buy a house with a 524 credit score? Spoiler alert: It's not necessarily a straight "no," but it does mean we need to get a little creative and strategic.

Think of your credit score as a report card for your financial habits. A 524? Well, it's saying you might have missed a few assignments, shall we say. It falls into the "poor" or "bad" credit range. Now, don't panic! This isn't a life sentence. It's just information, and information is power, my friend!

The Traditional Route: Probably Not (But Don't Give Up!)

Let's be real. Going the traditional mortgage route with a 524 credit score is going to be tough. Most conventional lenders (think big banks) prefer to see scores in the 620s or higher. Why? Because they see a lower score as a higher risk. They're worried you might not pay them back. And hey, from their perspective, it makes sense. But we aren't going to let that stop us, are we?

Must Read

So, before you throw in the towel and resign yourself to a lifetime of renting, let’s explore some options. Just because one door is closed doesn't mean there aren't others waiting to be opened!

Alternative Avenues: Where the Magic Happens

This is where things get interesting! There are several paths you can take that might make homeownership a reality, even with a less-than-stellar credit score.

FHA Loans: Your Friend in Need

FHA loans (backed by the Federal Housing Administration) are often a fantastic option for first-time homebuyers and those with lower credit scores. They're designed to make homeownership more accessible. The big perk? You can often qualify with a credit score as low as 500, especially if you can make a larger down payment (think 10%). Even with a score between 500 and 579, a 10% down payment can open doors. That said, even if you have a score above 580, you may be able to secure an FHA loan with as little as 3.5% down.

But remember, FHA loans come with mortgage insurance premiums (MIP). You'll pay an upfront MIP and then annual MIP for the life of the loan (in most cases). Factor those costs into your budget!

VA Loans: For Our Veterans

If you're a veteran, active-duty military member, or eligible surviving spouse, a VA loan might be your golden ticket. These loans, guaranteed by the Department of Veterans Affairs, often don't require a down payment and have more lenient credit score requirements than conventional loans. In fact, the VA doesn't set a minimum credit score, but lenders typically look for scores above 620, although it can be lower with compensating factors.

USDA Loans: Rural Dreams Come True

Dreaming of wide-open spaces? A USDA loan (backed by the U.S. Department of Agriculture) might be perfect. These loans are designed to help people buy homes in rural and suburban areas. And guess what? They often have lower credit score requirements! While guidelines vary by lender, some may approve borrowers with scores around 620. Eligibility is dependent upon income, and the location must meet USDA guidelines.

Private Money Lenders: A Risky but Possible Option

Private money lenders (also known as hard money lenders) are individuals or companies that lend money outside of traditional banks and credit unions. They often have more flexible approval criteria, but be warned: interest rates and fees can be significantly higher. This should really be a last resort, and you must understand the terms completely before signing anything.

Down Payment Assistance Programs: Every Little Bit Helps

Don't underestimate the power of down payment assistance programs (DAPs)! Many states, counties, and cities offer programs to help first-time homebuyers with down payments and closing costs. These programs can be a lifesaver, regardless of your credit score.

Boosting Your Score: The Ultimate Power-Up

While exploring these alternative options is important, let's not forget about the power of improving your credit score. Even a small increase can make a big difference in the interest rates you qualify for. So how do you do it?

- Pay your bills on time, every time! This is the biggest factor.

- Keep your credit card balances low. Aim for below 30% of your credit limit.

- Dispute any errors on your credit report.

- Become an authorized user on someone else's credit card (with their permission, of course!).

- Consider a secured credit card.

Improving your credit score isn't an overnight fix. It takes time and effort. But it's worth it! Think of it as leveling up in a video game. Each point you gain gets you closer to your goal.

The Bottom Line: Homeownership Is Possible!

So, can you buy a house with a 524 credit score? It's not impossible! It will likely require some creativity, a bit of patience, and maybe a few extra steps. But with the right strategy, determination, and maybe a little help along the way, you can achieve your dream of owning a home.

Don't let a number define your future. Take control of your finances, explore your options, and remember, you've got this! Start researching, connect with a reputable mortgage lender who specializes in working with borrowers who have lower credit scores, and get ready to turn that dream into a reality. The world of homeownership awaits!

Ready to learn more and take the next step? Reach out to local housing counseling agencies or non-profit organizations for guidance. Their resources are free or low cost and can help you create a plan for success. Go get 'em!