Backdoor Ira Conversion Vanguard

Okay, so you've heard whispers of a "Backdoor Roth IRA Conversion" and Vanguard is in the mix? Sounds kinda shady, right? Like you’re entering a spy movie. But trust me, it’s perfectly legal (and pretty darn clever!).

Think of it as a financial secret handshake. You know, for those of us who are too successful (that's you!) to contribute directly to a Roth IRA.

What's the Deal? Income Limits!

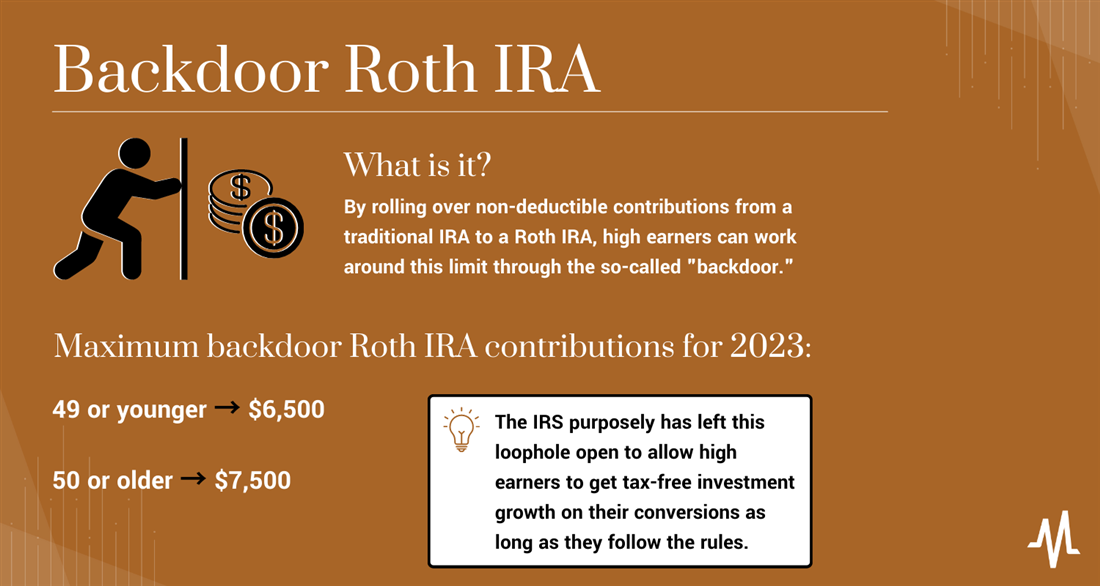

Roth IRAs are awesome. Tax-free growth? Yes, please! But there's a catch: income limits. If you earn too much, you can't directly contribute. Bummer, right?

Must Read

This is where the "backdoor" comes in. It's like sneaking through a side entrance to the party.

The Backdoor: Step-by-Step (Simplified!)

Here's the basic recipe for this financial sorcery, especially if you're considering Vanguard:

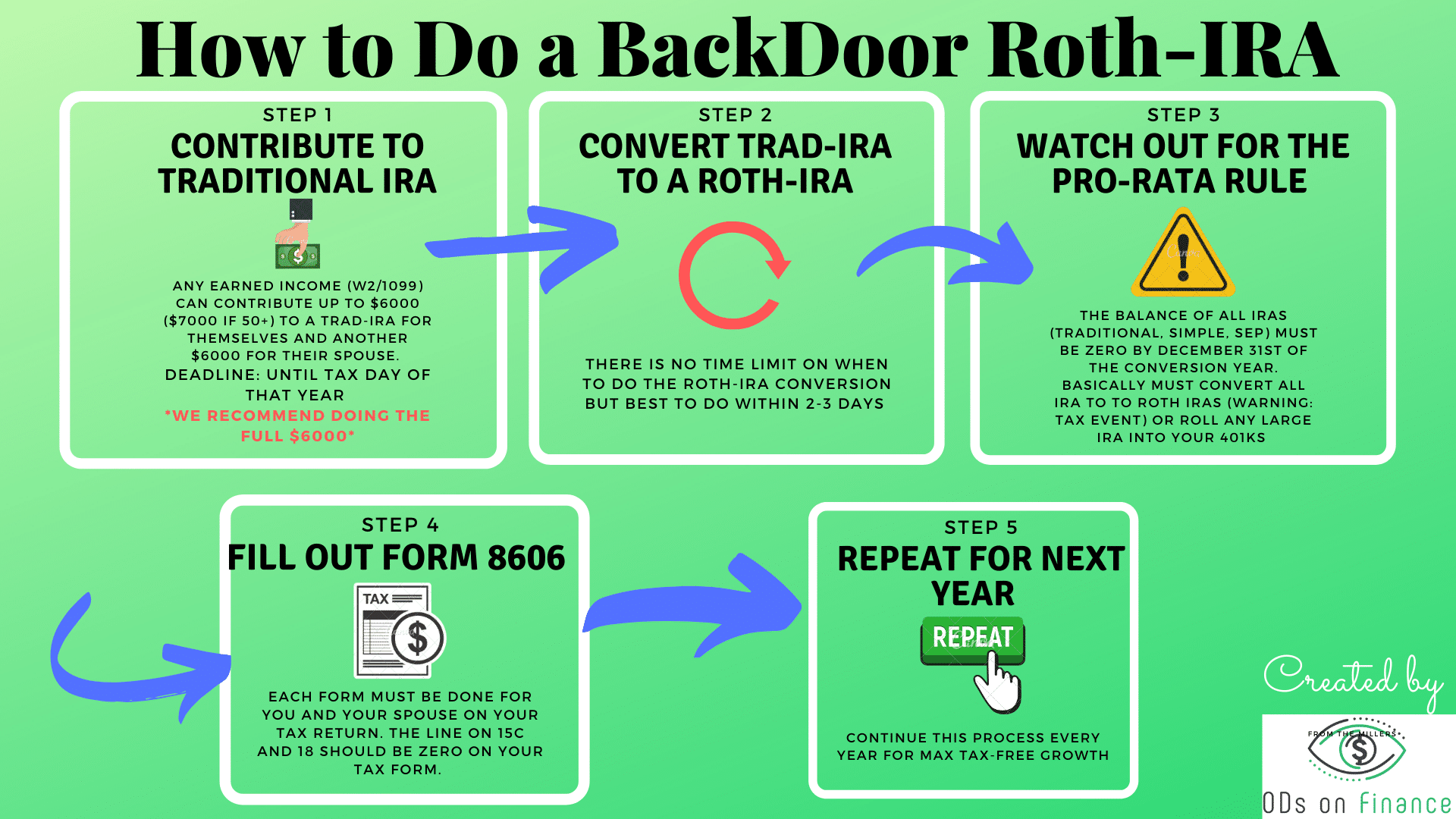

- Contribute to a Traditional IRA: Even if you think you make too much, you can usually contribute to a traditional IRA. It's like saying, "Hey IRS, I'm investing!"

- Don't Deduct It (Maybe): This is key. If you're already covered by a retirement plan at work (like a 401(k)), deducting your traditional IRA contributions might not be worth it. The whole point is to minimize taxes at this stage. Keep it simple!

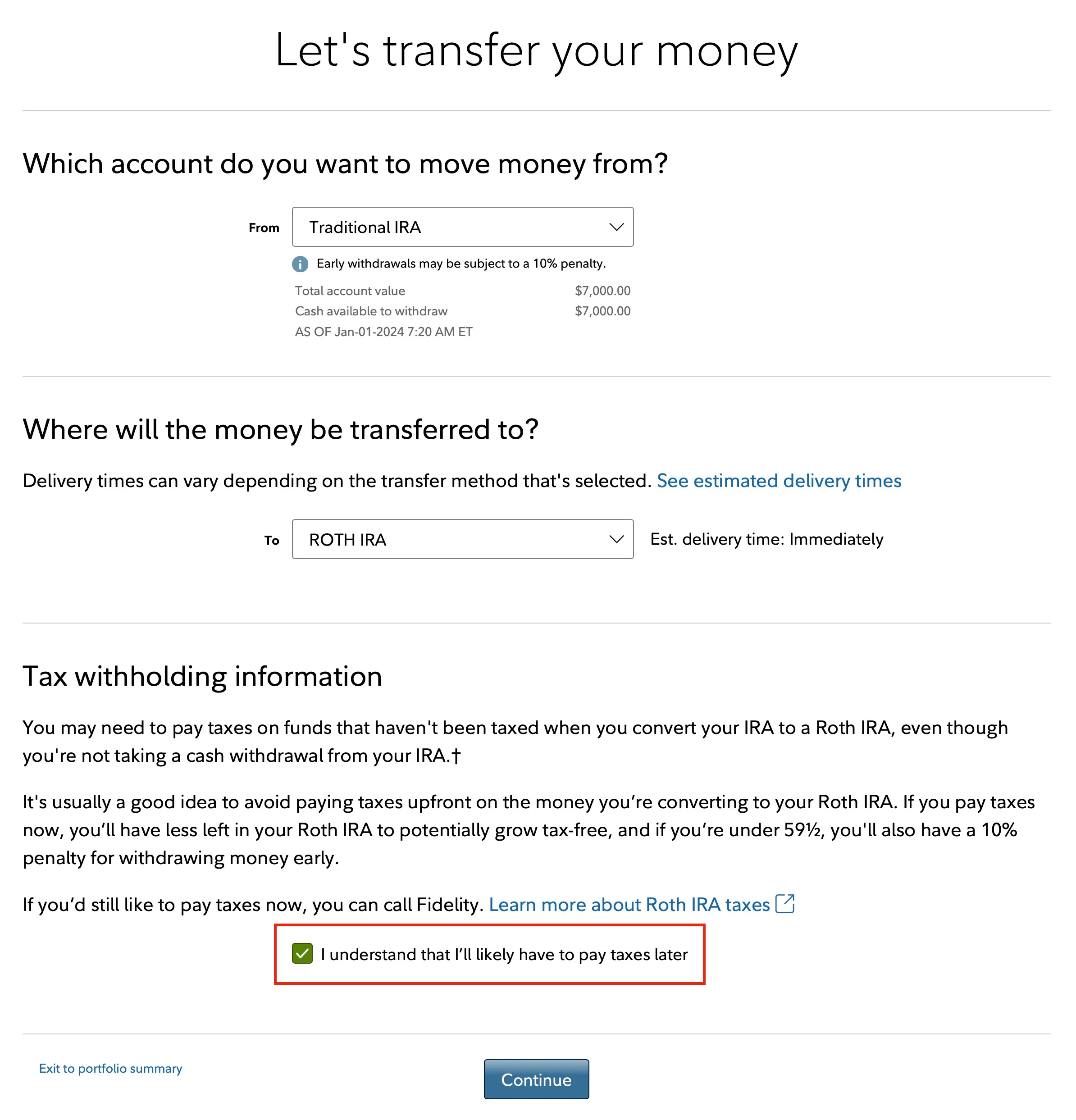

- The Conversion: Now, the magic happens. Convert that traditional IRA to a Roth IRA. Boom! You've bypassed the income limits.

Think of it like this: You're transforming boring, taxable money into shiny, tax-free unicorn money. Who wouldn't want that?

Why Vanguard?

Vanguard is a popular choice for a few reasons:

- Low Fees: Vanguard is known for its ridiculously low fees. This is super important because every dollar you save on fees is a dollar that can grow in your Roth IRA.

- Easy to Use: Their website is pretty straightforward. No confusing jargon (mostly!).

- Reputation: They're a well-respected company. You're trusting them with your hard-earned cash, after all!

It's like choosing a reliable car. You want something that gets you from point A to point B without breaking down every five minutes. Vanguard is that reliable car.

The Catch (There's Always a Catch, Right?)

Okay, so it's not completely free money. Here are a couple of things to keep in mind:

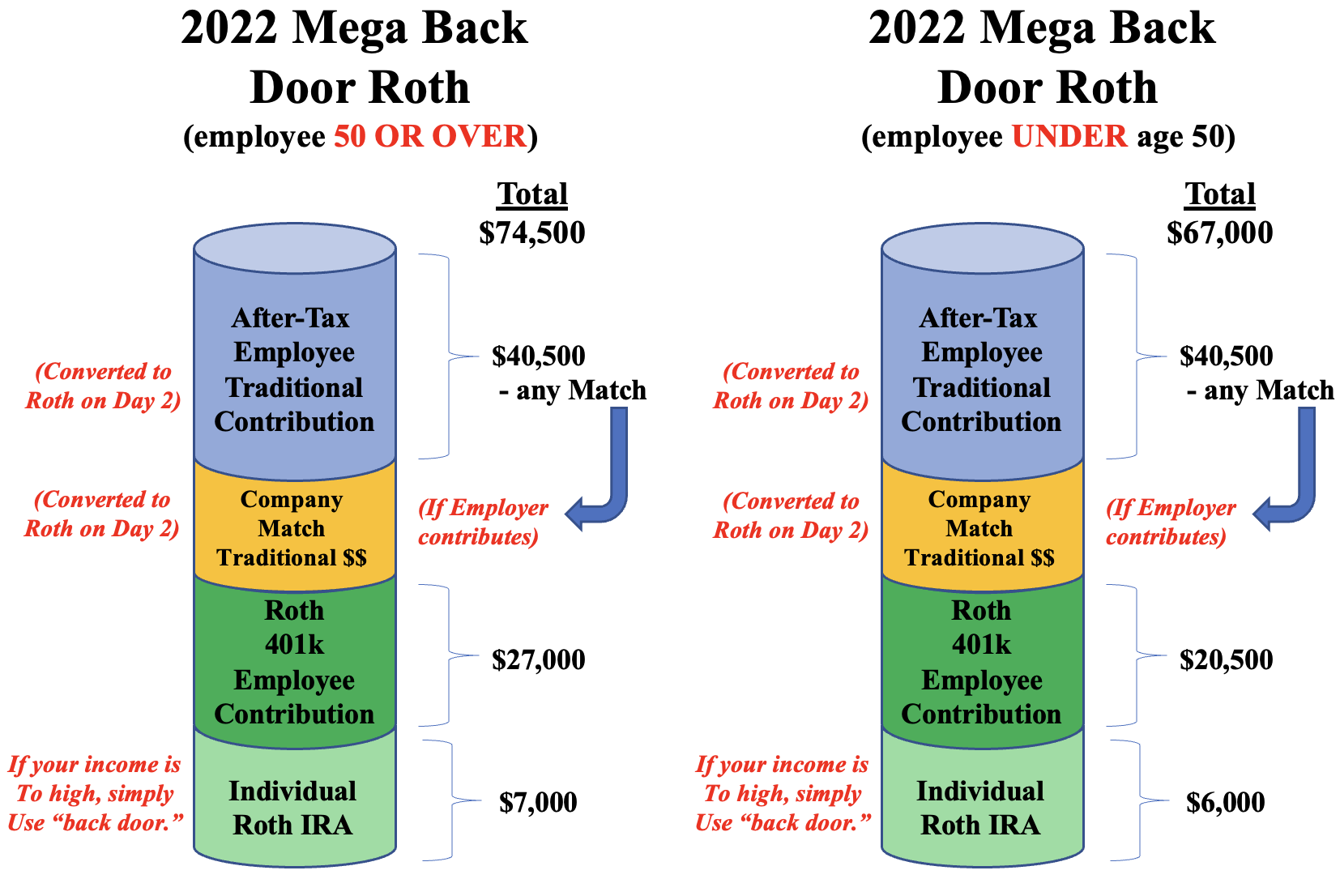

- The Pro-Rata Rule: This is the biggest gotcha. If you have other traditional IRAs (SEP, SIMPLE, Rollover), the IRS sees all your IRAs as one big pot. This can make the conversion more complicated and potentially taxable. Imagine trying to separate glitter from sand. Not fun!

- Taxes: If you did deduct your traditional IRA contributions and then convert, you'll owe taxes on the amount you converted. That's why keeping it non-deductible is often the way to go.

Basically, you want to make sure your "backdoor" is clean and doesn't have any hidden fees or unexpected tax implications.

Is It Right for You?

This is the million-dollar question (literally, maybe!). Consider this if:

- You're over the Roth IRA income limits.

- You want tax-free growth.

- You're comfortable with a little bit of financial planning.

If you're not sure, talk to a financial advisor! They can help you navigate the complexities and make sure you're not accidentally stepping on a financial landmine.

Fun Fact!

Did you know that the term "Backdoor Roth IRA" isn't an official term? The IRS doesn't have a specific form for it. It's just a clever nickname the financial community came up with. It's like a secret code!

Don't Be Scared, Be Savvy!

The Backdoor Roth IRA conversion can seem intimidating, but it's a powerful tool for those who are locked out of direct Roth IRA contributions. And with Vanguard, you've got a solid platform to make it happen (with a little research and maybe some professional guidance, of course!). So, go forth and conquer your financial goals!

Just remember to double-check those pro-rata rules. Nobody wants a glitter-sand situation!