At What Credit Score Can You Buy A House

So, you're dreaming of owning a house, huh? Visions of freshly baked cookies wafting from your own kitchen, movie nights in a living room that’s actually yours, and finally having a garden gnome collection without your landlord giving you the side-eye? Awesome! But before you start picking out paint colors and arguing over which of you gets the walk-in closet, there's a little something called a credit score to consider.

Don't panic! It’s not as scary as it sounds. Think of your credit score as your financial report card. It tells lenders how likely you are to pay back the money they lend you. And spoiler alert: a good score makes buying a house a lot easier.

The Magical Number: What Credit Score Do You Need?

Alright, let's cut to the chase. There isn't one single, universally accepted “magic number” that unlocks the door to homeownership. It’s more like a sliding scale of awesome. But generally, aiming for a score of 620 or higher is a solid starting point.

Must Read

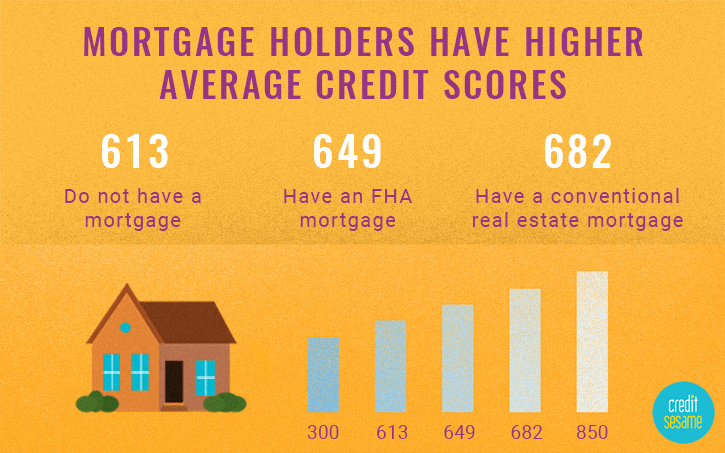

Why 620? Because that’s often the minimum score required for a conventional loan. These loans are like the gold standard of mortgages – often offering better interest rates and terms than other options. Think of it as getting the VIP pass to the house-buying party!

Now, what if your score is, shall we say, a tad below 620? Don’t despair! It’s not the end of the world. There are still options!

Other Avenues to Homeownership

Think of these as the “secret passages” to your dream home:

- FHA Loans: The Federal Housing Administration (FHA) is like that super understanding aunt who's willing to help even if you’ve made a few questionable financial choices in the past. They often accept scores as low as 500 (though you’ll likely need a bigger down payment).

- VA Loans: If you're a veteran, active-duty service member, or eligible surviving spouse, the Department of Veterans Affairs (VA) might be your knight in shining armor. They offer loans with no minimum credit score requirement in many cases! (Subject to lender requirements). It's a fantastic benefit for those who've served our country.

- USDA Loans: Yearning for a farmhouse in the countryside? The U.S. Department of Agriculture (USDA) offers loans to help people buy homes in rural areas. Credit score requirements vary but can be more lenient than conventional loans.

Important Note: Just because you can get approved with a lower score doesn't always mean you should. Lower scores often mean higher interest rates, which can cost you a lot more in the long run.

Boosting Your Score: Operation "House Hunter Hero"

So, what if your credit score needs a little TLC before you’re ready to buy? No problem! Think of it as a fun challenge, a chance to level up your financial fitness!

Here are a few quick tips to boost your score:

- Pay your bills on time, every time! This is like showing up to work on time – it demonstrates reliability.

- Keep your credit card balances low. Think of your credit cards as emergency funds, not free money. Aim to use less than 30% of your available credit.

- Don’t open a bunch of new credit accounts at once. Lenders might think you’re desperate for cash, which can lower your score.

- Check your credit report for errors. Mistakes happen! Dispute any inaccuracies you find. You're entitled to a free credit report from each of the three major credit bureaus annually.

Think of improving your credit score like training for a marathon. It takes time, effort, and consistency, but the reward – a brand new house – is totally worth it!

Remember, buying a house is a big decision, but it's also an exciting one! With a little planning and a healthy dose of financial responsibility, you'll be hanging those curtains and planting those garden gnomes in no time!

Disclaimer: This article provides general information only and does not constitute financial advice. Consult with a qualified financial advisor for personalized guidance.