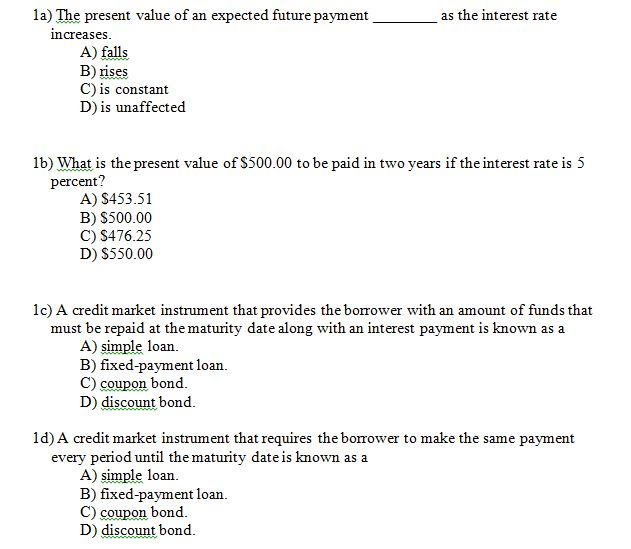

As The Interest Rate Increases The Present Value

:max_bytes(150000):strip_icc()/Pvif_4-3-v2_final-aea739afcbca439998b6fd4032af48bf.png)

Imagine you've just won a lottery! Congratulations! The grand prize is $10,000, but here's the catch: you don't get it all at once.

Instead, they'll pay you $1,000 every year for the next ten years. Sounds good, right? Well, let's talk about interest rates and how they play tricks with the value of that prize.

The Time-Traveling Money

Think of money as a time traveler. A dollar today isn't quite the same as a dollar a year from now.

Must Read

Why? Because you could invest that dollar today and earn interest! So, $1,000 arriving next year is worth slightly less than $1,000 in your hand right now.

This concept is called present value. It's like asking, "What's the real, today-in-my-pocket worth of all those future payments?"

The Interest Rate Monster

Here's where the interest rate comes in. It's like a tiny monster nibbling away at the future value of your money.

The higher the interest rate, the bigger the nibbles! It demands a larger discount for waiting to receive your money.

Consider this scenario: interest rates are super low, like everyone’s asleep. Receiving $1,000 next year isn't so bad, because you wouldn't earn much interest by having the money today.

Low Rates, Happy Days

Let's say the interest rate is 1%. That $1,000 you'll get next year is almost as good as having $1,000 today.

The present value of your entire lottery winning is pretty close to $10,000!

You're practically rolling in dough, even though you have to wait a bit. It's like a slow, steady stream of happiness flowing into your bank account.

High Rates, Uh Oh!

Now, imagine the interest rate shoots up to 10%! Suddenly, that little interest rate monster is starving!

It demands a much bigger discount for making you wait. Ten percent is a substantial amount that you could earn by investing the money immediately.

That $1,000 you're getting next year? Its present value just plummeted.

The Shrinking Lottery Prize

Suddenly, the present value of your lottery winnings is significantly less than $10,000. Ouch!

All those future payments, when added together in today’s money, aren't worth as much. It’s like watching your prize money slowly deflate.

You're still getting $10,000 eventually, but the true value, in today's terms, is much lower. The monster ate a significant chunk of your win!

A Real-Life Example: Bonds

Think of government bonds. You're essentially lending money to the government, and they promise to pay you back with interest over time.

When interest rates rise, the present value of those future bond payments decreases. Existing bonds become less attractive because new bonds will offer higher interest rates.

Thus, the market value of older bonds goes down, reflecting that lower present value.

The Unexpected Consequence

Here’s a slightly more heartwarming example. Imagine you are saving up for your child's college education.

You've diligently put money aside, expecting tuition to remain relatively constant. But what if interest rates rise dramatically?

On one hand, your existing savings might not be worth quite as much in terms of present value for future tuition costs. But, on the other hand, the returns on your savings will increase dramatically!

A Silver Lining

The higher interest rates mean your savings will grow faster! So, while the present value of your future tuition payments might technically be less due to the discount rate, the actual growth of your savings could outpace that decrease.

This could potentially offset the rising costs of education or even provide a larger sum than initially anticipated!

It's like a financial seesaw – one side goes down (present value), but the other goes up (investment growth)!

The Mortgage Maze

Let’s say you’re looking at buying a house and taking out a mortgage. Higher interest rates have a profound impact.

Firstly, the monthly payments go up. This is because you’re paying more interest on the loan.

Secondly, and perhaps less intuitively, the present value of the house itself can decrease.

House Value?

Wait, what? How does the house value change because of interest rates?

Well, consider this: many people buy houses based on what they can afford monthly. Higher interest rates mean people can afford less house.

This decreased demand can lead to lower house prices overall, impacting the present value of your potential new home.

The Grand Finale

So, the next time you hear about interest rates going up, remember the present value monster!

It's always lurking, nibbling (or sometimes devouring) the value of your future income streams.

Understanding this relationship can help you make smarter financial decisions, whether you're investing, saving, or just dreaming of lottery winnings.

A Thought to Ponder

The present value concept is a reminder that time is indeed money. The longer you have to wait for something, the less it's worth today.

It’s a fundamental principle that shapes everything from investment strategies to understanding the true cost of borrowing.

So, embrace the monster, understand its appetite, and navigate the world of finance with a little more wisdom (and perhaps a bit of humor).