Another Name For The Lifo Reserve Account Is

Alright, accounting newbies and seasoned pros alike, let's dive into a topic that might sound drier than a desert, but trust me, it's got a sneaky bit of intrigue: the LIFO Reserve! Now, accounting terms can often feel like a secret language, but understanding them unlocks a powerful ability to decipher the financial health of a company. And today, we're demystifying a particularly interesting one. So, why is this fun? Because knowing this little detail can impress your boss, help you ace that accounting exam, or just make you feel incredibly smart at your next cocktail party. Plus, it involves a hidden identity! What's not to love?

So, what’s the big secret? Another name for the LIFO Reserve Account is the LIFO Adjustment Account. Bam! Mystery solved. But wait, there's more! Just knowing the alias isn't enough. Let's understand what this account actually does and why it matters.

In the world of inventory accounting, there are different ways to value the goods a company has on hand. One method, called LIFO (Last-In, First-Out), assumes that the most recently purchased items are the first ones sold. Think of it like a stack of pancakes – the top pancake (the last one cooked) is the first one you eat. While seemingly simple, LIFO can create a bit of a wrinkle in financial reporting, especially when compared to companies using FIFO (First-In, First-Out), which assumes the oldest items are sold first.

Must Read

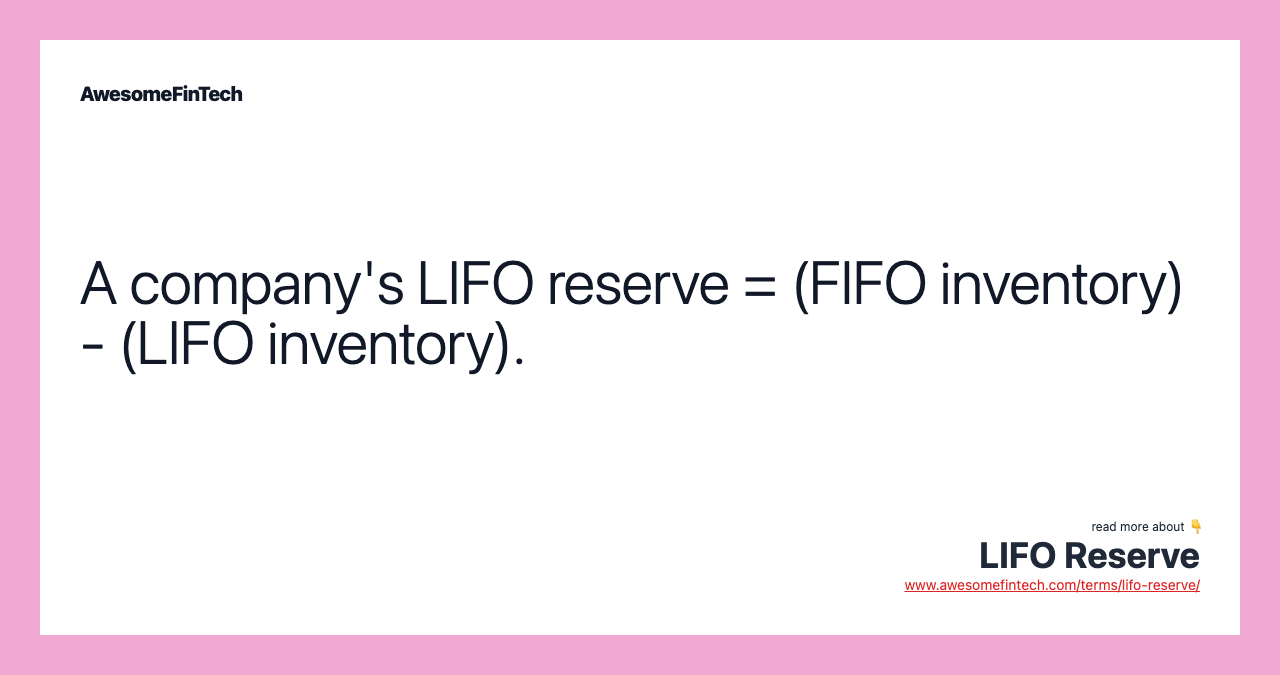

Here's where the LIFO Reserve/Adjustment Account comes to the rescue! It's a contra-asset account. That means it reduces the value of inventory reported on a company's balance sheet when LIFO is used. It essentially represents the difference between the value of inventory if it were calculated using FIFO versus using LIFO. Think of it as a correction factor, ensuring financial statements present a clearer picture.

But why even use LIFO in the first place if it requires this adjustment? Well, in times of rising prices, LIFO can lead to a higher cost of goods sold (COGS) and therefore a lower taxable income. This can mean lower taxes for the company! However, the IRS rules dictate when LIFO can be used, and it's not allowed under International Financial Reporting Standards (IFRS). So, it's primarily a U.S.-centric accounting quirk.

The benefit of the LIFO Reserve/Adjustment Account is that it allows analysts and investors to compare companies that use LIFO with those that use other inventory valuation methods, primarily FIFO. By adding the LIFO Reserve back to the reported LIFO inventory value, you get a more comparable figure, allowing for apples-to-apples comparisons. This is crucial for making informed investment decisions.

In summary, the LIFO Reserve (or LIFO Adjustment Account) is a vital tool for understanding and comparing companies using LIFO. It ensures that financial statements are transparent and allows for accurate analysis, despite the complexities of inventory valuation methods. So next time you hear someone mention the LIFO Reserve, you can confidently say, "Ah yes, the LIFO Adjustment Account! I know all about that!" You'll be the star accountant of the party, guaranteed.