An Allowance For Doubtful Accounts Is Established.

Hey there, future accounting whiz! Ever sold something on credit, like offering to let your friend pay you back for that awesome concert ticket later? Hope they actually do, right? That's where the "Allowance for Doubtful Accounts" comes in! Think of it as your financial "just in case" fund. It’s like having a spare donut hidden in your desk drawer… for emergencies only, of course!

So, What IS This "Allowance" Thingy?

Okay, so in the business world, companies often sell stuff on credit. They're basically saying, "Pay us later!" This creates something called accounts receivable – money owed to them. Sweet! But here’s the rub: sometimes, customers don't pay. Gasp! That’s where the Allowance for Doubtful Accounts, or ADA (catchy, right?), steps in. It’s an estimate of how much of that accounts receivable the company doesn't expect to collect. It's like betting against yourself... but in a responsible, accounting kind of way!

Think of it this way: you're baking a cake. You hope everyone will eat it, but you know Uncle Jerry only ever takes a tiny nibble. The ADA is like setting aside a smaller slice for him. You expect less from him, and that's okay!

Must Read

Why Do We Bother Setting One Up?

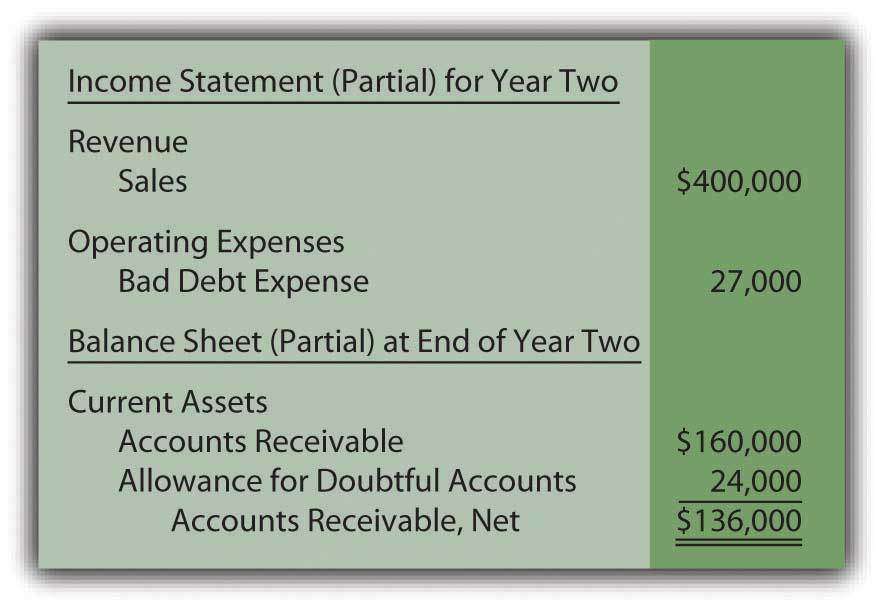

Great question! It’s all about being realistic and following something called the matching principle. This principle basically says that expenses should be recognized in the same period as the revenue they helped generate. So, if you sold something in January but expect to write off some of the receivable in February, you need to account for that potential loss now, in January. It prevents you from painting too rosy a picture of your financial health.

Imagine you sell 100 gizmos for $10 each, so you book $1000 in revenue. Yay! But if you suspect you won’t collect $100 from a certain customer, you don't want to pretend you’re going to collect the whole $1000! The ADA helps you reflect the actual economic reality.

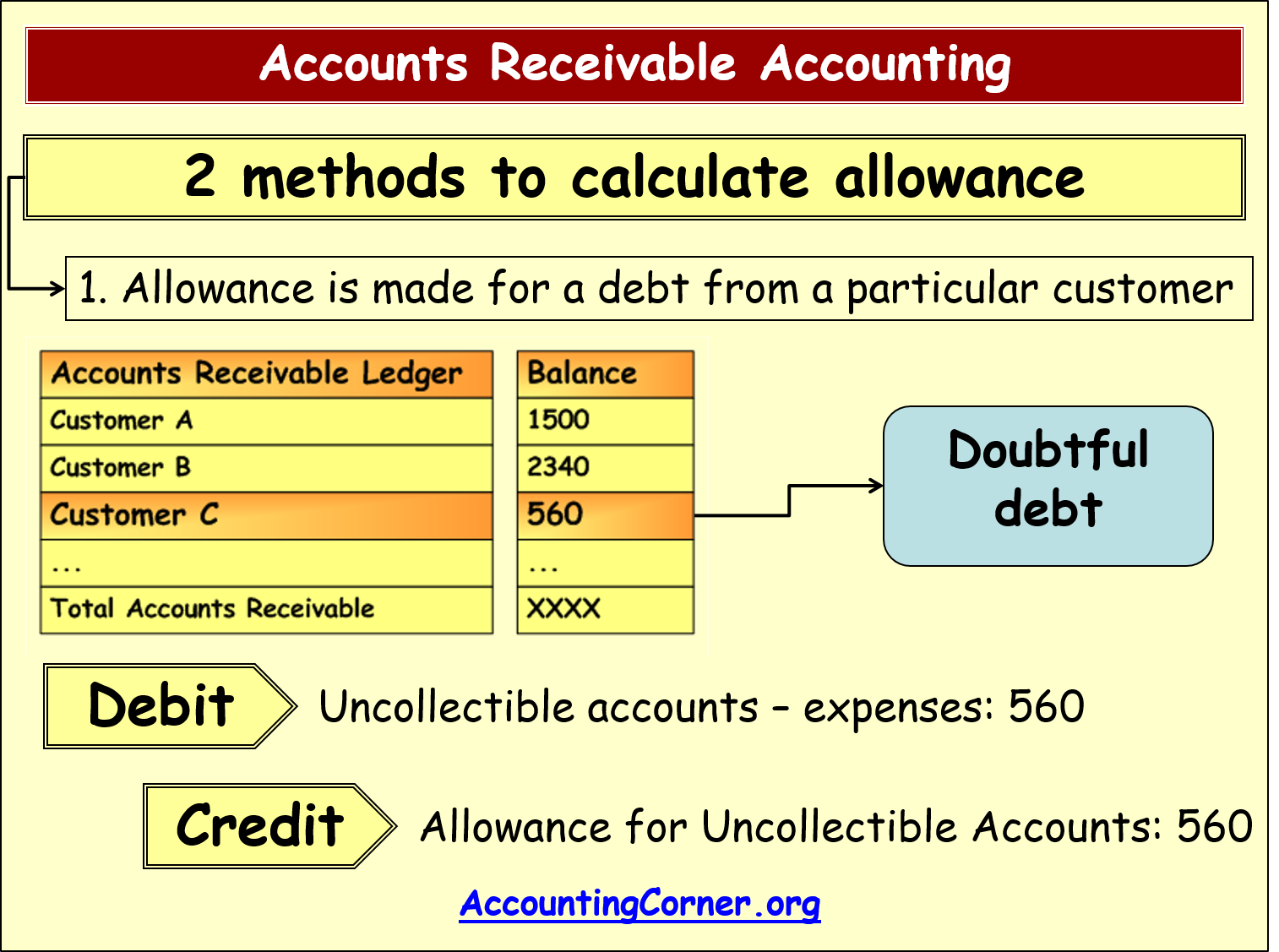

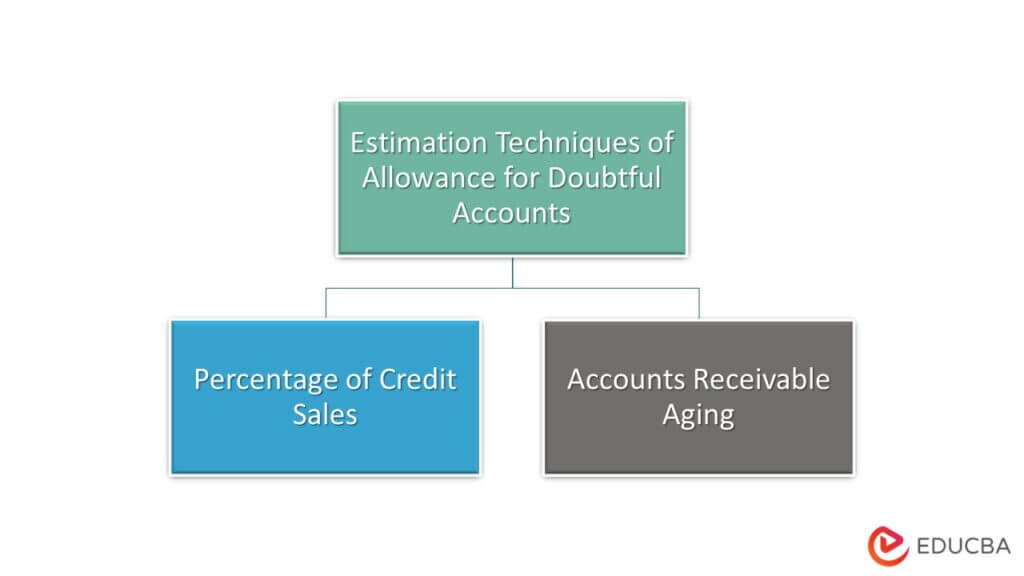

How Do We Actually Create This Allowance?

There are a few ways! Here are two common ones:

- Percentage of Sales Method: You estimate a percentage of your total sales that you think will be uncollectible. Easy peasy! For example, you might say, "We think 2% of our sales will go bad."

- Aging of Accounts Receivable Method: You break down your receivables by how old they are. Older receivables are considered riskier. Someone who owes you money for 90+ days is probably less likely to pay than someone who owes you for 30. It’s like comparing a fresh banana to one that's been hiding in your backpack for a week… which one are you more likely to eat? (Hopefully, the fresh one!).

Whichever method you choose, the key is to make a reasonable estimate. Don't just pull a number out of thin air! Look at your past experience, industry trends, and any specific information about your customers. Do your homework!

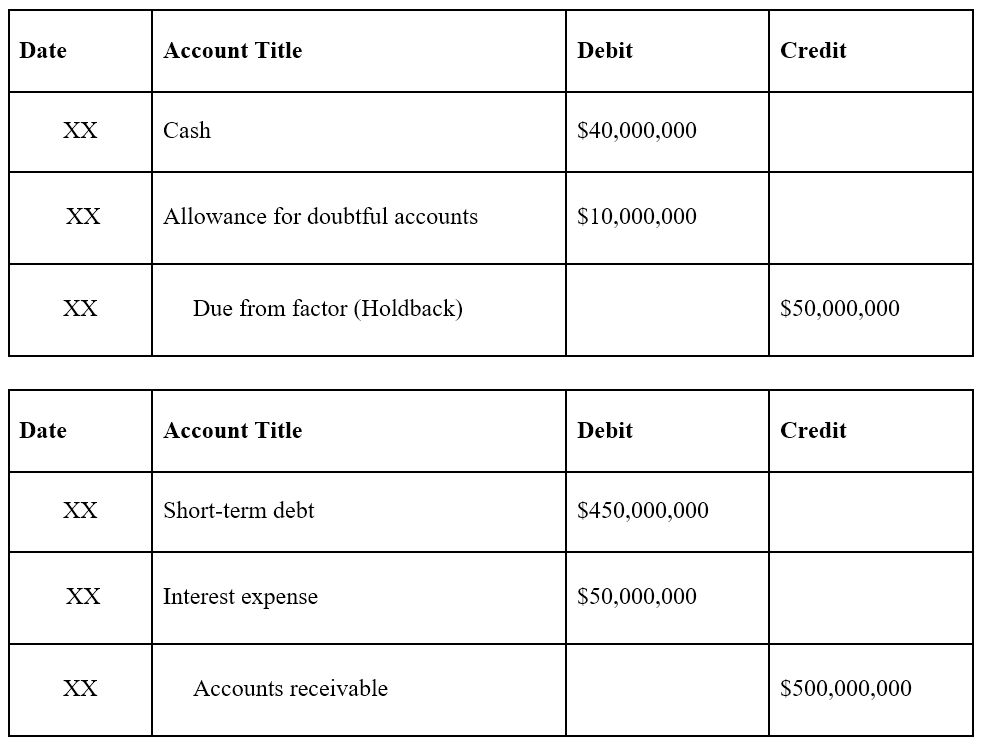

The Journal Entry (Don't Panic!)

Okay, time for the scary part: the journal entry! It's not as bad as it sounds, I promise. Here's the basic idea:

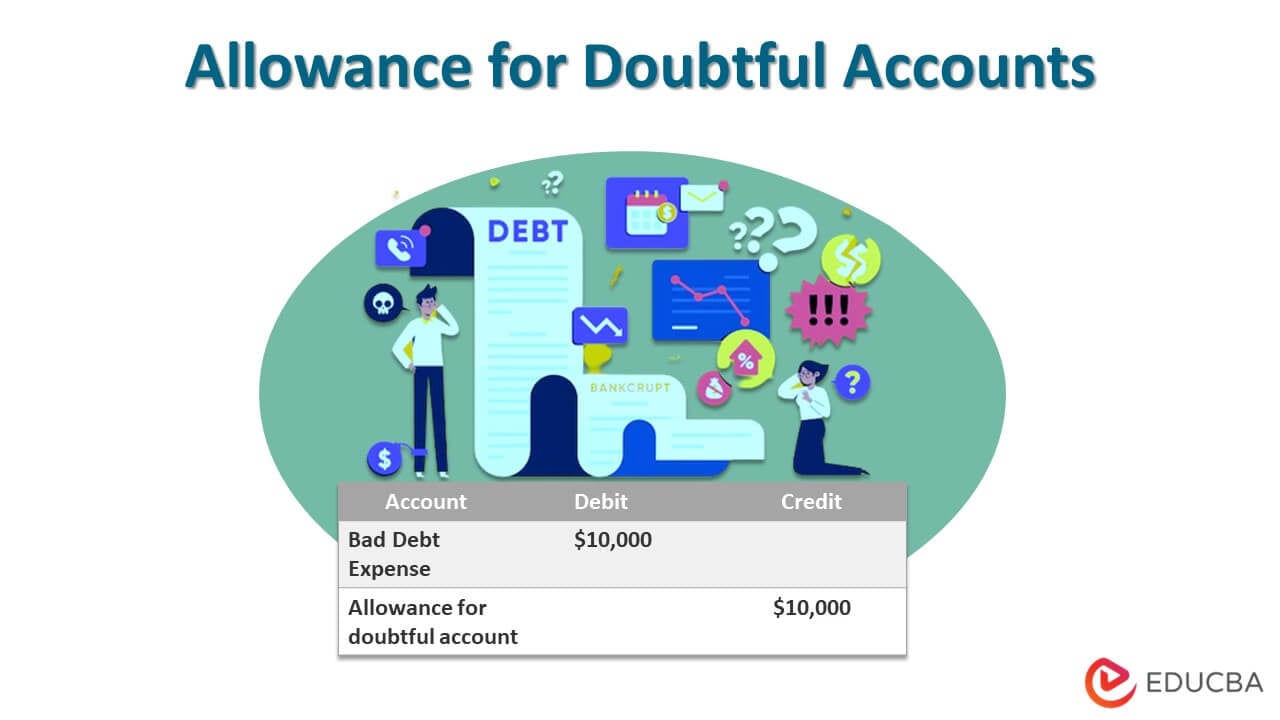

You'll debit (increase) something called Bad Debt Expense. This is an expense account that shows up on your income statement. It reflects the estimated cost of those uncollectible accounts.

You'll credit (increase) the Allowance for Doubtful Accounts. This is a contra-asset account, meaning it reduces the value of your accounts receivable on the balance sheet. It's like a cushion, protecting you from the impact of those potential losses.

So, it looks something like this:

Debit: Bad Debt Expense $X Credit: Allowance for Doubtful Accounts $X

Where $X is your estimated amount of uncollectible accounts. Boom! You just created an ADA!

What Happens When a Customer Actually Doesn't Pay?

Ah, the moment of truth! When you've officially given up on collecting from a customer, you write off the account. This involves:

Debiting the Allowance for Doubtful Accounts (reducing the cushion).

Crediting Accounts Receivable (removing the uncollectible amount from your books).

Notice that this write-off doesn't affect your income statement! The expense was already recognized when you established the allowance. It's just cleaning up your balance sheet.

In Conclusion: Be Prepared, Stay Positive!

Establishing an Allowance for Doubtful Accounts might seem a bit pessimistic, but it’s actually a sign of good financial management. It shows you're being realistic about your business and preparing for potential challenges. It's like packing an umbrella even if the forecast is sunny – you're ready for anything!

So, go forth and create your own ADAs with confidence! Remember, accounting isn't about being perfect; it's about being honest and transparent. And who knows, maybe you'll even get to write off a few accounts and celebrate with that hidden donut! You deserve it!