An Adjusting Entry For Accrued Expenses Involves

Alright, gather 'round, folks! Let's talk about adjusting entries. Yeah, yeah, I know what you’re thinking: "Accounting? Sounds about as exciting as watching paint dry... in slow motion." But trust me, even accounting has its moments of… well, let's call them mildly amusing. Today, we're diving into the murky waters of accrued expenses. Hold onto your hats, it's gonna be a wild ride! (Okay, maybe a slightly bumpy one).

What in the World Are Accrued Expenses?

Imagine this: You order a pizza. A really good pizza. The kind with extra cheese, pepperoni the size of your thumb, and maybe even pineapple (don't judge!). You devour the entire thing, feeling like a Roman Emperor after a successful conquest. But... you haven't paid for it yet. The pizza place is like, "No worries, pay us next week."

That, my friends, is the essence of an accrued expense. It's an expense you've incurred – you've gotten the benefit (that glorious pizza!) – but you haven't actually paid the bill yet. It's like the financial equivalent of a post-dated check, or promising your friend you'll totally pay them back for that concert ticket… someday.

Must Read

The Dreaded Adjusting Entry

Now, here's where the "adjusting entry" comes into play. See, in the world of accounting, we have this quirky little thing called the matching principle. It basically says: "Match your expenses to the period in which you incurred them, even if you haven't paid for them yet!" It's like the universe demanding that you acknowledge the pizza debt, even if your wallet is currently hiding under your bed.

So, an adjusting entry for accrued expenses is all about recognizing that expense now, even though the cash hasn't flown out of your account yet. It's like saying, "Okay, universe, I acknowledge the pizza! I promise to pay. Just don't send the debt collectors!"

How Does This Actually Work? (Don't Panic!)

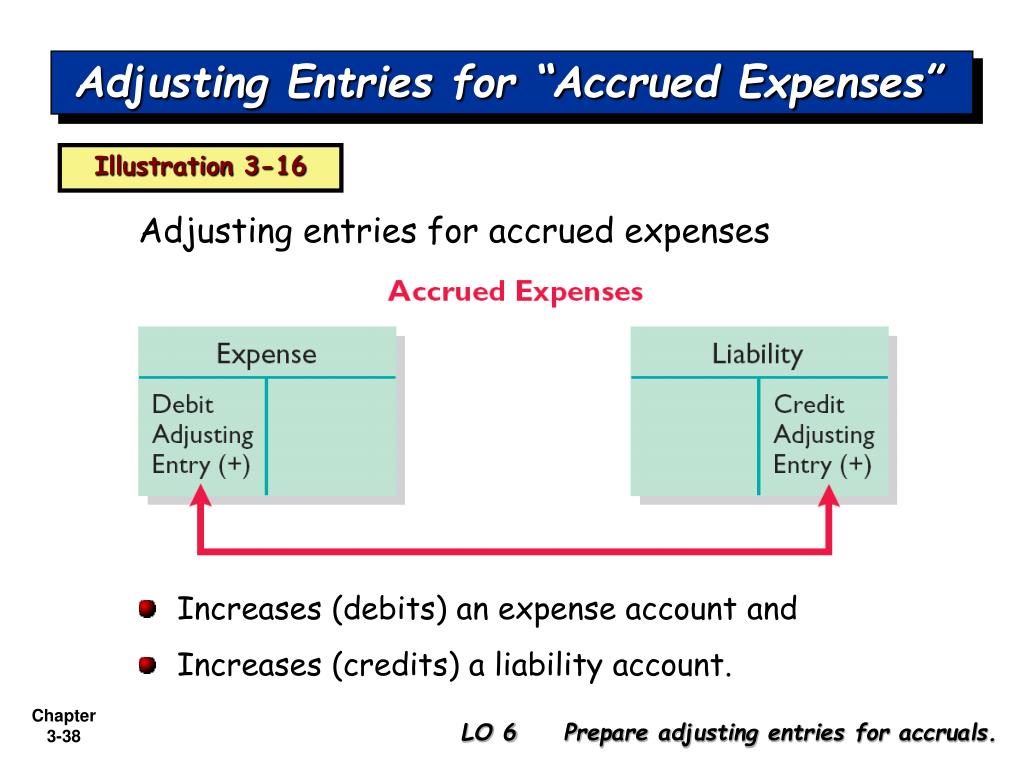

The adjusting entry involves two things: increasing an expense account and increasing a liability account. Think of it this way:

- The expense account is like yelling from the rooftops, "HEY EVERYONE, WE HAD A PIZZA PARTY! IT COST US MONEY!" So you're debiting that account to increase it.

- The liability account (often called "Accrued Expenses" or "Payable") is like writing yourself a little IOU note. It's saying, "We owe someone money! Don't forget!" You're crediting that account to increase it.

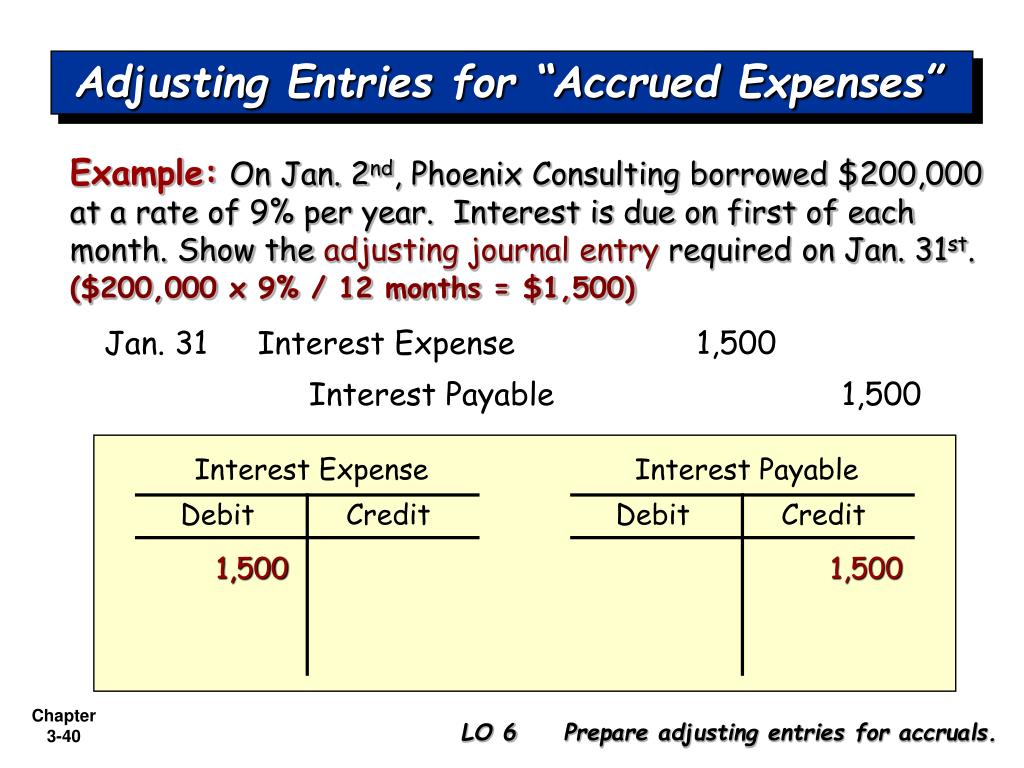

Let’s say that pizza cost you $25. Your adjusting entry would look something like this:

Debit: Pizza Expense - $25

Credit: Accrued Pizza Payable - $25

Easy peasy, right? Okay, maybe not easy, but hopefully less terrifying than you initially thought.

Why Bother With This Nonsense?

You might be thinking, "Why can't I just wait until I actually pay the bill to record the expense? What's the big deal?" Well, the big deal is accurate financial statements! If you only recorded expenses when you paid them, your income statement might be a total lie. It would be like saying you're super healthy just because you haven't been to the doctor recently, ignoring all those late-night pizza binges (hypothetically speaking, of course!).

Accrued expenses paint a more accurate picture of your company's financial health. They show that you've incurred obligations, even if you haven't settled them yet. This is super important for making informed decisions about your business.

Examples in the Wild!

Accrued expenses aren't just about pizza, although that's clearly the most relatable example. Here are a few other common examples:

- Accrued Salaries: You have employees who worked hard all month, but payday isn't until next week. You owe them money!

- Accrued Interest: You're borrowing money, and interest is accruing on the loan. Even if you don't pay the interest yet, it's still an expense!

- Accrued Utilities: You used electricity, water, and internet throughout the month. The bill hasn't arrived yet, but you still owe the money!

Basically, any expense you've incurred but haven't paid yet is a potential candidate for an adjusting entry.

The Takeaway (And a Final Joke!)

So, there you have it: accrued expenses and their trusty sidekick, the adjusting entry. It's all about recognizing expenses when you incur them, not just when you pay them. It might seem like a small detail, but it makes a big difference in the accuracy of your financial statements. Ignoring these entries is like pretending you don't owe anyone money... which, let's be honest, never ends well.

Now, before I leave you to ponder the mysteries of accounting, here's a final thought: What do you call an accountant who's also a stand-up comedian? A debit-ant!

Thanks for listening, folks! Tip your waitresses, and try the pizza – it's accrued, but worth it!