A Manufacturing Company Calculates Cost Of Goods Sold As Follows

Ever wonder how companies figure out how much it really costs to make that widget you just bought? It's a wild ride, involving more than just the price of raw materials!

Let's dive into the fascinating world of Cost of Goods Sold (COGS), manufacturing style. Think of it as a detective story, but with spreadsheets instead of magnifying glasses. Get ready to be amazed.

The Great COGS Calculation Caper

Imagine a bustling factory, machines whirring, and workers assembling things. All those moving parts contribute to the final cost. That's what we're tracking.

Must Read

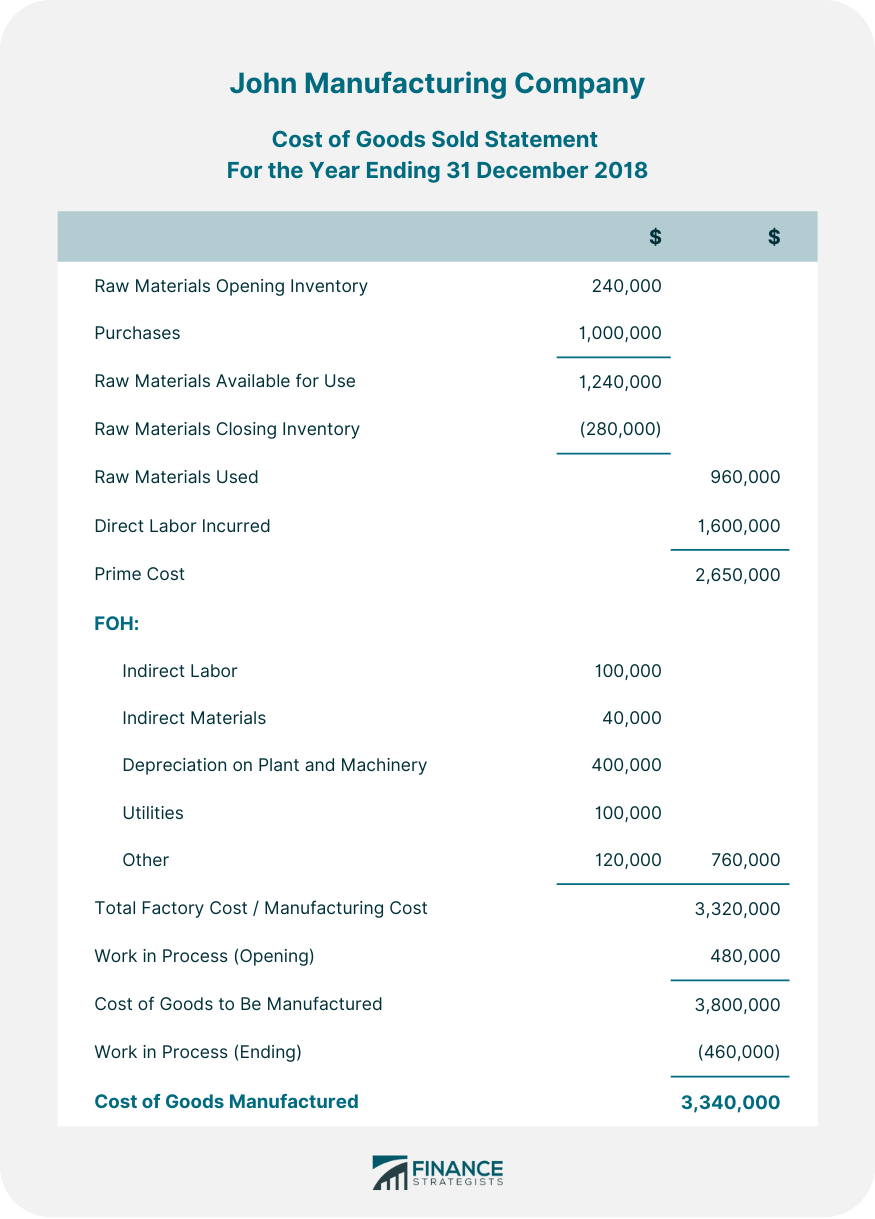

First, we need to understand the Basic Formula. It’s like a secret recipe, passed down through generations of accountants! Prepare for some number crunching.

Beginning Inventory: The Starting Line

Picture a warehouse, stacked high with stuff. This is the beginning inventory. It's the stuff we had left over from last year.

Think of it as ingredients waiting to be turned into delicious products. Important detail, right?

Purchases: Adding Fuel to the Fire

Now, imagine trucks rolling up to the loading dock, delivering more raw materials. That's where purchases come in.

Things like metal, plastic, and sprinkles. These new goodies are going to contribute to what we sell!

Direct Labor: The Human Touch

Don't forget the amazing people who actually build these things! This is direct labor.

Every hour they spend assembling, shaping, or quality-checking adds to the cost. They’re the magic ingredient, you see.

Manufacturing Overhead: The Hidden Costs

This is where it gets interesting. Manufacturing overhead are all the indirect costs needed to run the factory.

Think rent for the factory, electricity to power the machines, and even the salary of the factory supervisor! It’s a BIG category.

Don't forget about depreciation on the machines. Those babies aren't free!

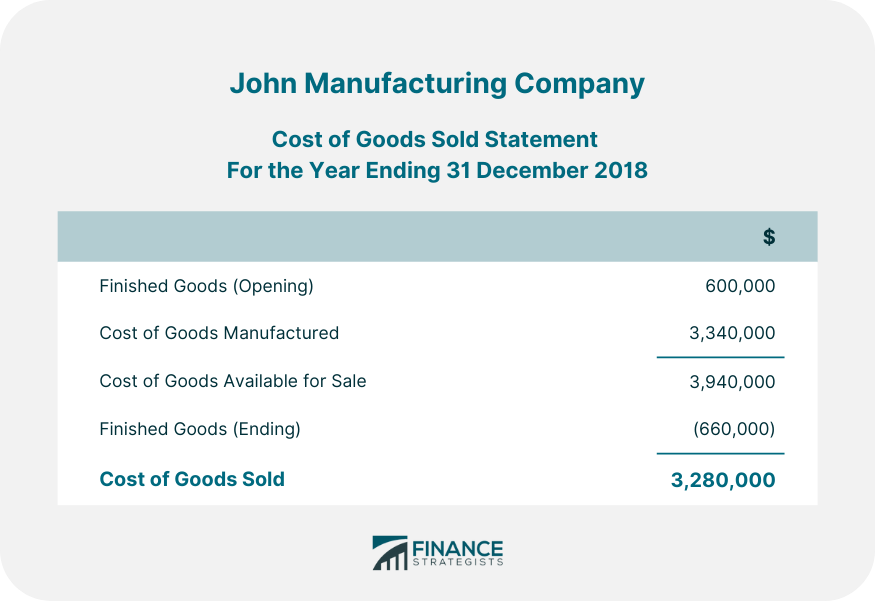

Cost of Goods Available for Sale: The Full Arsenal

Add beginning inventory, purchases, direct labor, and manufacturing overhead together. BOOM! We got something.

This tells us the total cost of all the products that could be sold. It's almost time to unleash this product to the world!

Ending Inventory: What's Left Over?

At the end of the period, we're left with stuff. This is the ending inventory.

These are the unsold goodies still sitting on the shelves. They’re waiting for their moment to shine!

The Grand Finale: Calculating COGS

Here's the moment we've been waiting for! Are you ready? Are you on the edge of your seat?

Subtract the ending inventory from the cost of goods available for sale. The result? Our COGS!

This tells us how much it cost us to make the stuff we actually sold. It's a key figure for understanding profitability.

So, the formula is something like this:

Beginning Inventory + Purchases + Direct Labor + Manufacturing Overhead - Ending Inventory = Cost of Goods Sold (COGS)

Pretty cool, right? It’s a lot more involved than just adding up the price of materials.

Why It Matters (and Why It’s Kinda Fun)

Understanding COGS helps companies make smarter decisions. It gives them insight to improve their bottom line.

Pricing strategies, production efficiency, and even supplier negotiations can all be improved. Now, that's power.

And let’s be honest, there’s something oddly satisfying about tracking all these numbers and seeing the big picture. It's like solving a puzzle!

Maybe you will become an accountant someday. The world needs more people who love to calculate things.

So, the next time you see a product on the shelf, remember the complex calculation behind its price. There's more than meets the eye!

Maybe you can try calculate the cost of the next product you are selling.

Now, go forth and COGS! You're basically a manufacturing accounting expert now.